Feminine Hygiene Market Summary

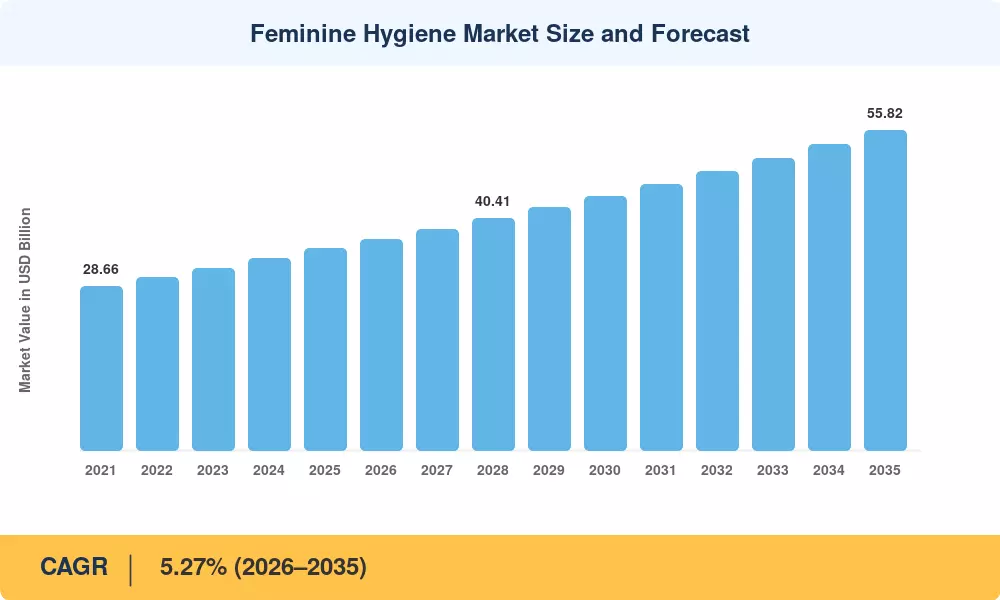

The Feminine Hygiene Market was valued at USD 35.19 billion in 2025 and is projected to reach USD 36.58 billion in 2026 before climbing to USD 55.82 billion by 2035, registering a CAGR of 5.27% during the forecast period (2026–2035). Government-backed menstrual equity legislation — including Scotland's Period Products Act and similar mandates across 14 U.S. states — has transformed period care products from discretionary purchases into institutionally procured essentials, accelerating category-wide demand [2]. Parallel growth in e-commerce subscriptions and direct-to-consumer channels is reshaping how consumers access sanitary pads and tampons, compressing traditional retail cycles and lifting average order values.

A material shift is underway from conventional single-use disposables toward organic cotton feminine products and reusable alternatives such as menstrual cups and discs. Brands investing in plant-based absorbent cores, compostable packaging, and medical-grade silicone have captured consumer trust, with organic period care products growing at roughly twice the pace of their conventional counterparts [3]. The USDA BioPreferred Program and EU Single-Use Plastics Directive are supplying additional regulatory tailwinds that reward sustainable product design.

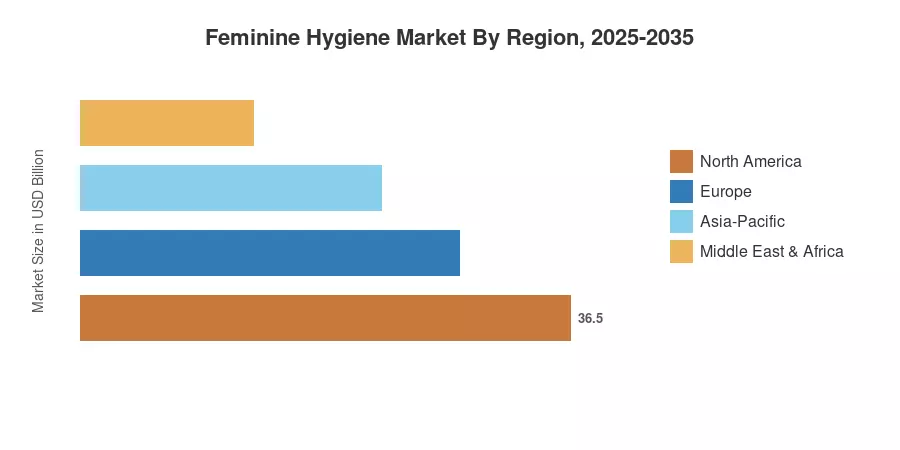

North America leads the Feminine Hygiene Market with approximately 33.8% of 2025 revenue, driven by high per-capita spending and strong retail infrastructure. Asia-Pacific delivers the fastest growth at a projected CAGR of 7.10%, fueled by rising disposable incomes and expanding menstrual hygiene management awareness campaigns across India, Indonesia, and the Philippines [4]. Europe holds the second-largest share at roughly 27%, buoyed by Nordic sustainability mandates and France's zero-VAT policy on period care products. As institutional procurement scales and digital distribution deepens, the Feminine Hygiene Market is set for sustained broadening through 2035.

Key Report Takeaways

• By Product Type

- Sanitary pads and tampons together command over 68% of the Feminine Hygiene Market revenue, with pads alone accounting for a 42.7% share in 2025

- Menstrual cups and discs are forecast to expand at a 7.65% CAGR through 2035, driven by eco-conscious consumers switching

• By Product Category

- Disposable period care products captured 72.4% of the Feminine Hygiene Market in 2025, though reusable alternatives are closing the gap at a 7.98% CAGR

• By Nature

- Disposable period care products captured 72.4% of the Feminine Hygiene Market in 2025, though reusable alternatives are closing the gap at a 7.98% CAGR

- Natural and organic cotton feminine products are advancing at a 8.2% CAGR as clean-label preferences penetrate menstrual hygiene management

• By Distribution Channel

- Pharmacy and drug stores held 35.4% channel share in 2025, while online retail posted the highest growth trajectory in the Feminine Hygiene Market

• By Region

- North America contributed USD 11.89 billion in 2025

- Asia-Pacific is projected to register a 7.10% CAGR through 2035, adding the largest incremental volume

Market Size and Forecast (2021–2035)

MRFR's sizing methodology triangulates top-down revenue estimates from manufacturer filings, distributor sell-through data, and bottom-up demand models benchmarked against national health statistics and retail panel datasets.