Fetal Bovine Serum market Summary

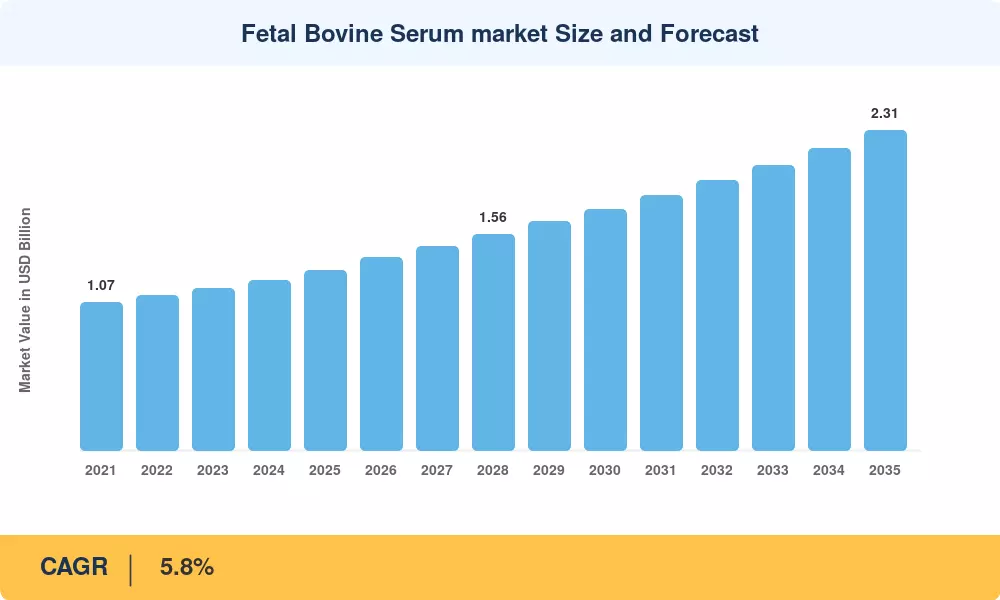

The Fetal Bovine Serum Market size was valued at USD 1.30 Billion in 2025, and the market is projected to grow from USD 1.39 Billion in 2026 to USD 2.31 Billion by 2035, registering a CAGR of 5.8% during the forecast period 2026–2035. Two structural forces anchor this trajectory: the cell and gene therapy pipeline now exceeds 3,200 active clinical assets globally [1], creating non-discretionary demand for qualified serum lots, and the U.S. cattle herd dropped to roughly 87.2 million head in January 2025 — its lowest level since 1951 — tightening raw-material supply and reinforcing pricing power [2].

The industry is experiencing a pronounced quality stratification. Legacy standard-grade FBS is giving way to specialty grades — charcoal/dextran-stripped, dialyzed, and stem-cell-qualified — as researchers demand tighter lot-to-lot consistency. Meanwhile, regulatory agencies in the EU and U.S. have intensified traceability requirements for animal-derived biologicals, pushing suppliers to invest in origin-certification platforms and ISIA-certified collection networks [3]. Global biopharmaceutical R&D spending crossed USD 265 billion in 2024 [4], underwriting steady serum consumption even as synthetic alternatives gain early traction.

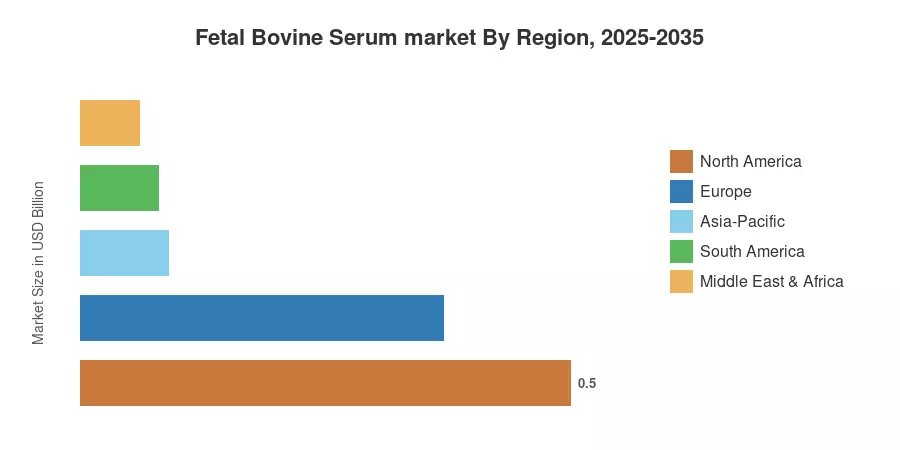

North America controlled approximately 38.2% of the Fetal Bovine Serum Market in 2025, anchored by concentrated biopharma clusters and NIH-funded academic research infrastructure. Asia-Pacific is the fastest-growing region, projected at a 6.7% CAGR through 2035, driven by expanding CRO/CMO capacity in China and India. Europe held the second-largest share at roughly 28.5%, supported by EMA-harmonized quality frameworks and a dense network of academic research institutes. The Fetal Bovine Serum Market is poised for sustained but supply-constrained growth as therapeutic complexity scales faster than herd recovery.

Key Report Takeaways

• By Product Type

- Charcoal/dextran-stripped serum captured 34.1% of the Fetal Bovine Serum Market share in 2025, driven by demand from hormone-sensitive assay workflows.

- Stem-cell-qualified FBS is advancing at the fastest pace among product types, reflecting expansion in regenerative medicine trial enrollment.

• By Application

- Biopharmaceutical production accounted for 29.5% of total revenue in 2025, supported by monoclonal antibody and recombinant protein pipelines.

- Cell-culture maintenance and expansion is the fastest-growing application segment through 2035.

• By End User

- Biotechnology and pharmaceutical companies controlled 57.4% of the Fetal Bovine Serum Market in 2025.

- Academic and research institutes are posting the fastest end-user growth rate through 2035, fueled by government grant allocations.

• By Region

- North America led with a 38.2% revenue share in 2025, while Asia-Pacific is projected to grow at a 6.7% CAGR through 2035.

Fetal Bovine Serum Market Size and Forecast (2021–2035)

Market Research Future's estimation framework combines primary supplier interviews, customs trade-flow data, and downstream consumption audits across biopharmaceutical, academic, and contract research end users. Historical figures reflect confirmed shipment values; forecast projections apply a compounded growth model calibrated against pipeline expansion rates and herd-supply indicators.