Flat Glass Market Summary

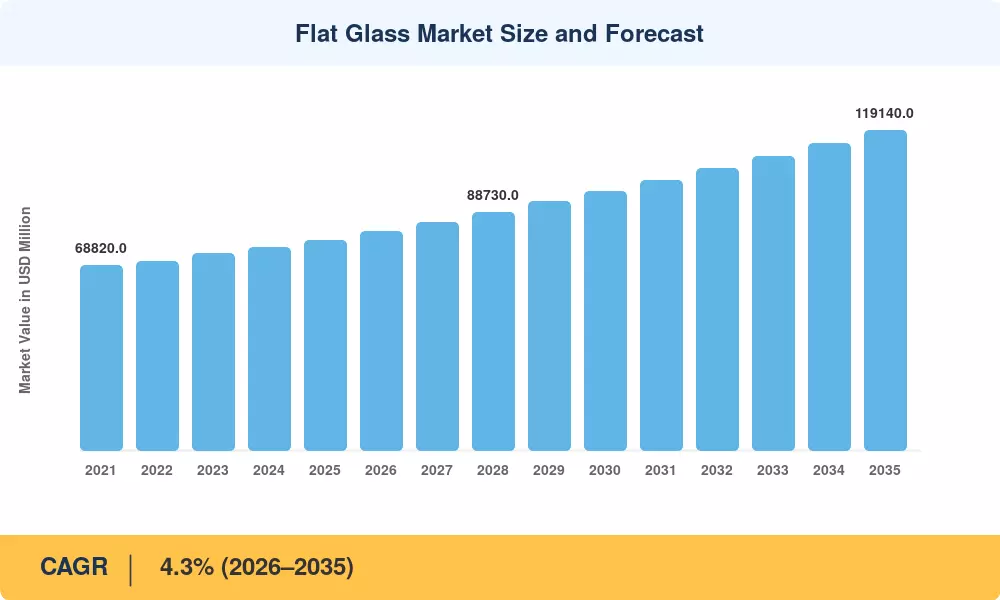

The Flat Glass Market reached an estimated USD 78,200 Million in 2025 and is projected to climb from USD 81,560 Million in 2026 to USD 119,140 Million by 2035, registering a compound annual growth rate of 4.3% across the forecast window. Tightening building energy performance directives — led by the European Union's revised Energy Performance of Buildings Directive and the U.S. Department of Energy's updated commercial building envelope standards — are channeling capital into high-performance glazing at an unprecedented pace [1][7]. Simultaneously, national photovoltaic deployment targets exceeding 350 GW of annual solar additions by 2030 are pulling glass producers deeper into the renewable energy value chain [12].

A structural change is redefining manufacturing floors in the flat glass market. Oxy-electric hybrid melting lines and green-hydrogen-fired units, which can reduce scope-one emissions by up to 40%, are replacing legacy regenerative furnaces, which have long been the foundation of mass manufacturing [19]. The necessity of this shift was demonstrated by Saint-Gobain alone, which set aside EUR 1.3 billion for capital expenditures related to decarbonization until 2028 [5]. In developed economies, single-pane retrofit stock is being replaced with ultra-thin triple-glazed assemblies and vacuum-insulated panels, strengthening the connection between product innovation and regulatory compliance.

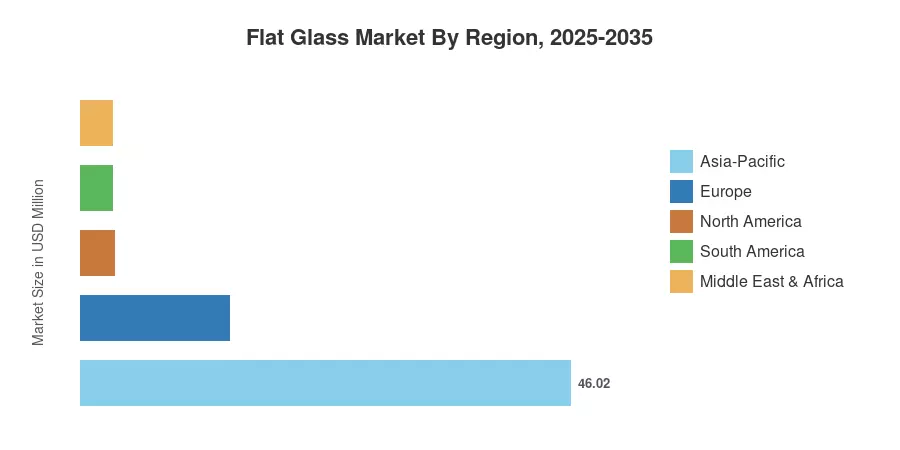

Due to China's dominance in both capacity and consumption, the Asia-Pacific accounts for around 59% of the world's flat glass market revenue [3]. With a CAGR of about 5.0% until 2035, the area also leads the growth chart, propelled by Southeast Asian infrastructure corridors and India's ambitious housing initiatives [9]. Due to strict near-zero-energy construction regulations and renovation-wave funding, Europe maintains the second-largest share at roughly 19% [7]. In contrast, North America's future depends on commercial refit cycles and the growing supply chain for solar modules, setting up the flat glass market for long-term, steady growth.

Key Report Takeaways

• By Product Type

- Annealed glass accounted for roughly 74% of the total Flat Glass Market volume in 2025, reflecting its foundational role in standard architectural and automotive glazing.

- Processed glass is forecast to post a 5.0% CAGR through 2035, as demand for safety-rated and performance-enhanced products accelerates in commercial construction.

- Coated glass products captured around USD 7,820 million in 2025, underpinned by low-emissivity and solar-control specifications in green building codes.

• By End-User Industry

- Building and construction represented 75% of the Flat Glass Market in 2025, driven by new residential starts in Asia and deep-renovation mandates in Europe.

- Solar glass is advancing at a 7.0% CAGR to 2035, the fastest sub-segment, tracking global photovoltaic capacity expansion.

• By Region

- Asia-Pacific held roughly 59% of the Flat Glass Market revenue in 2025, with China alone contributing over half of the regional demand.

- North America is poised for a 4.1% CAGR, catalyzed by IRA-linked clean-energy manufacturing incentives and commercial building modernization.

Flat Glass Market Size and Forecast (2021–2035)

Market Research Future's estimation framework triangulates production data from national statistics bureaus, company-level financial filings, and downstream demand models across construction, automotive, and solar sectors. Historical figures reflect audited shipment volumes and trade databases; forecast projections incorporate policy scenario modeling and input-cost trend analysis [3][15].