Flexible Hybrid Electronics Market Summary

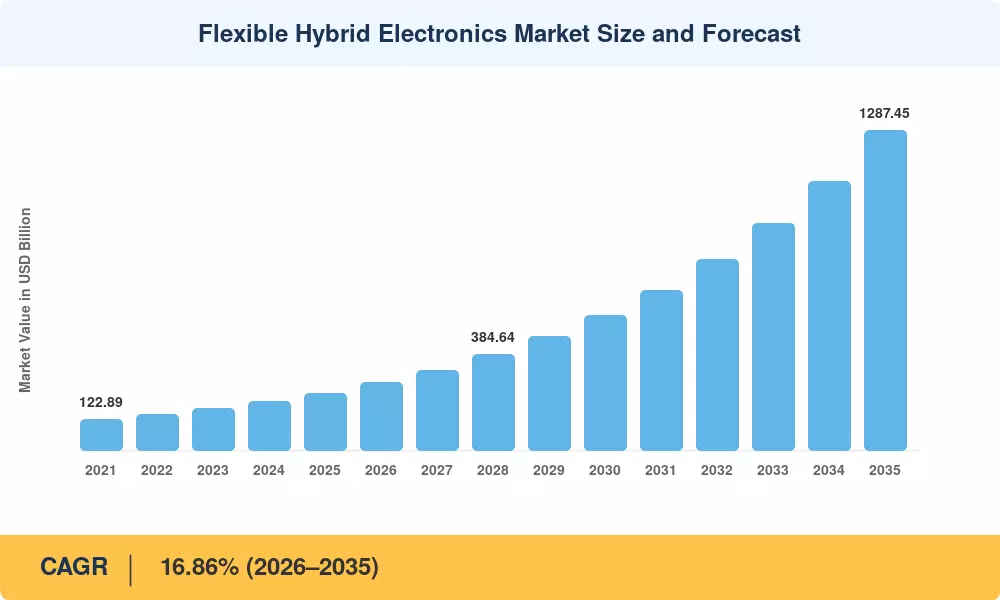

The flexible hybrid electronics market reached an estimated USD 229.19 million in 2025 and is projected to expand from USD 271.68 million in 2026 to USD 1,287.45 million by 2035, registering a CAGR of 16.86% during the forecast period. This acceleration is anchored in the U.S. Department of Defense's sustained commitment through the NextFlex Manufacturing Innovation Institute, which has channeled over USD 350 million in public-private investment toward conformal flexible circuits and hybrid rigid-flex electronics since its inception [2]. Parallel funding from the European Commission's Horizon Europe programme is directing approximately EUR 120 million toward stretchable electronics devices for medical diagnostics and smart packaging through 2027 [3].

A decisive technology shift is underway as rigid printed circuit boards give way to lightweight architectures that integrate thin-film silicon die onto polyimide and PET substrates. Roll-to-roll manufacturing lines — once limited to passive components — now handle flexible circuit integration of active sensors, microcontrollers, and antenna arrays in continuous web processes, cutting per-unit costs by an estimated 30–40% versus legacy sheet-based methods [4]. The flexible hybrid electronics market benefits directly from this transition as OEMs in consumer devices, automotive interiors, and healthcare seek conformable form factors that rigid boards cannot deliver.

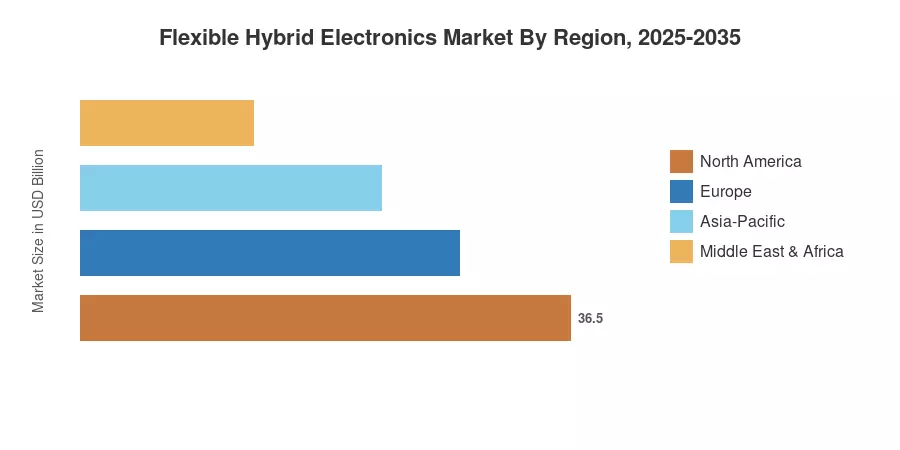

North America commands roughly 35.42% of the flexible hybrid electronics market, driven by defense procurement and Silicon Valley's wearable flexible hybrid systems ecosystem. Asia-Pacific is the fastest-growing region at a projected 17.32% CAGR through 2035, propelled by China's aggressive expansion of flexible display fabrication capacity and India's nascent but fast-scaling sensor manufacturing base. Europe holds the second-largest share at approximately 27%, with Germany and the Nordic countries leading adoption in automotive and industrial IoT applications. As substrate innovation continues to reduce materials costs, the flexible hybrid electronics market is positioned for broad-based global expansion over the coming decade

Key Report Takeaways

• By Component

- Flexible displays accounted for approximately 38.17% of the flexible hybrid electronics market in 2025, underpinned by OLED panel demand in smartphones and foldable devices

- Flexible sensors are projected to grow at a 17.45% CAGR through 2035 as conformal flexible circuits gain traction in continuous health monitoring and structural diagnostics

• By Substrate Material

- Polyimide substrates commanded the largest share of the flexible hybrid electronics market in 2025, valued at an estimated USD 100.26 million

- Paper and cellulose substrates are advancing at a 17.38% CAGR, driven by sustainable smart packaging and single-use wearable flexible hybrid systems

• By End-Use Industry

- Consumer electronics held 28.12% revenue share in 2025, reflecting strong demand for stretchable electronics devices in wearables and foldable phones

- Healthcare applications are projected to expand at a 17.24% CAGR through 2035 in the flexible hybrid electronics market

• By Region

- North America accounted for 35.42% share in 2025, led by defense and aerospace procurement of hybrid rigid-flex electronics

- Asia-Pacific is progressing at a 17.32% CAGR through 2035, the fastest among all regions in the flexible hybrid electronics market

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework combines bottom-up revenue modeling from manufacturer shipments, substrate consumption data, and end-use industry spending patterns. Historical figures draw on company filings, trade association data, and customs statistics, while forecast projections incorporate technology adoption curves, R2R capacity expansion schedules, and policy pipeline analysis.

.webp?v=1783416214)