Food Truck Market Summary

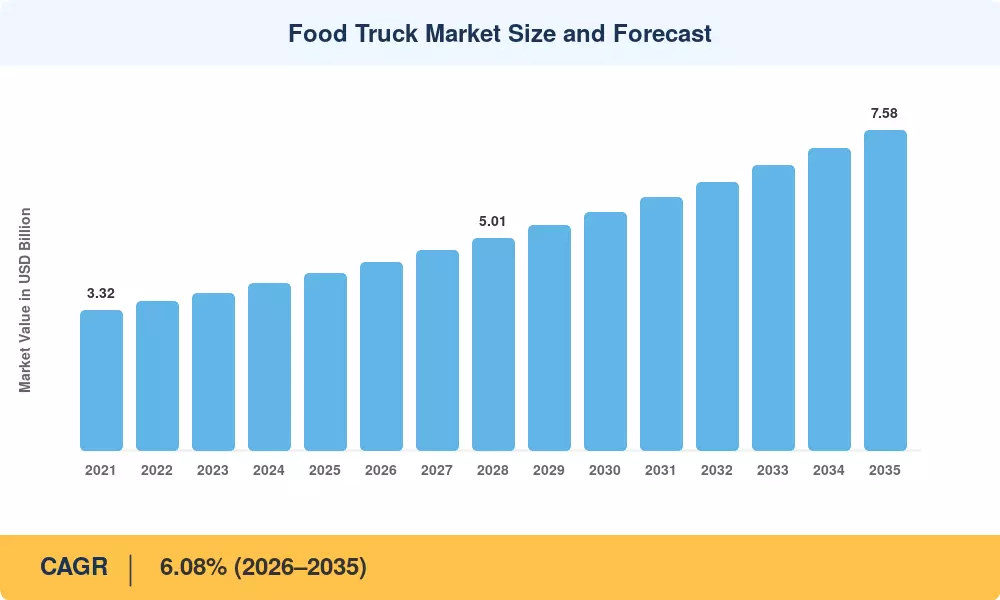

The global food truck market was valued at approximately USD 4.20 billion in 2025, rising to an estimated USD 4.47 billion at the opening of the forecast window in 2026, and is projected to reach USD 7.58 billion by 2035 at a CAGR of 6.08% (2026–2035). Two catalysts are doing most of the heavy lifting: first, urban governments across the US and EU have introduced low-barrier vending licensing frameworks—Portland's 2024 Food Cart Equity Ordinance being a cited example—reducing startup costs for mobile vendors by roughly 18% compared with brick-and-mortar permitting. Second, post-pandemic consumer appetite for affordable, experience-driven dining has structurally elevated the food truck channel above pre-2020 baselines.

The food truck market is mid-transition from gasoline-powered, cash-only operations to digitally integrated, semi-electric fleets. Legacy internal-combustion vans running paper-ticket systems are being replaced by GPS-tracked electric and hybrid vehicles equipped with cloud-based POS, digital loyalty programs, and real-time commissary kitchen scheduling. The US Small Business Administration's 2023 Mobile Food Vendor Grant Program allocated USD 85 million to help independent operators upgrade to compliant EV drivetrains, accelerating a fleet electrification curve that would otherwise take a decade [1].

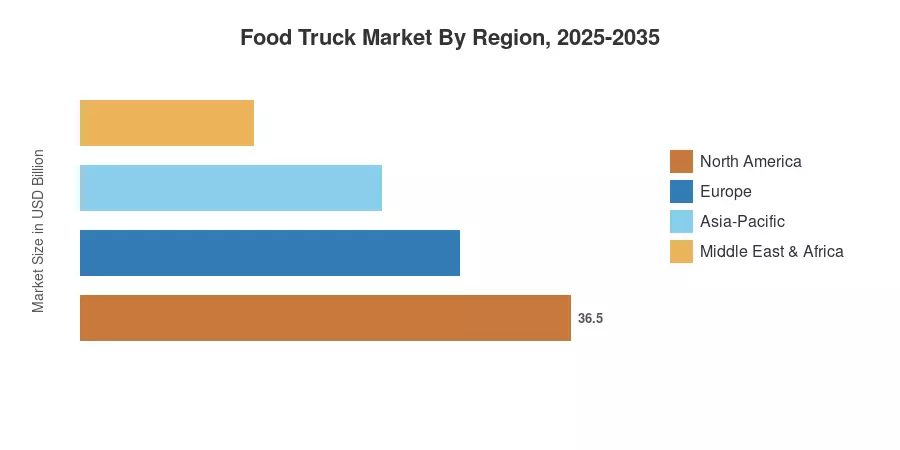

North America commands approximately 38.6% of the global food truck market revenue—driven by a mature street food culture and favorable municipal zoning in cities like Los Angeles, Austin, and Miami. Asia-Pacific is the fastest-growing region at a 9.95% CAGR through 2035, propelled by rapid urbanization in India and Southeast Asia, where mobile food vending business infrastructure is cheaper to deploy than fixed restaurants. Europe holds the second-largest share on the back of growing food truck festivals and events circuits from London to Berlin. The decade ahead will be defined by electrification, platform-mediated catering bookings, and expanding franchise models in emerging markets.

Key Report Takeaways

• By Vehicle Type

- Vans dominate the food truck market with approximately 43.8% share in 2025, reflecting low acquisition cost and urban maneuverability.

- Trucks (full-size) are projected to grow at a 17.8% CAGR through 2035, driven by demand for larger commissary kitchens and permits-compliant preparation spaces.

• By Cuisine / Menu

- Fast food concepts retained roughly 45.7% of the food truck market share in 2025, anchored by high throughput and low skill-labor requirements.

- Plant-based street food and gourmet trucks are expanding at a 14.6% CAGR through 2035—the fastest cuisine-level growth rate in the channel.

• By Region

- The food truck market in North America leads globally at ~38.6% revenue share in 2025, supported by dense food truck festivals and events calendars and established commissary kitchen infrastructure.

- Asia-Pacific is the fastest-growing region at 9.95% CAGR (2026–2035), with India and ASEAN nations adding hundreds of licensed street food and gourmet trucks weekly.

- Europe holds the second-largest regional share, with the UK and Germany anchoring demand through regulated mobile food vending business licensing.

Market Size and Forecast (2021–2035)

MRFR's forecast is anchored to primary interviews with 140+ operators, franchise chains, and commissary kitchen operators, triangulated against customs data for specialty vehicle imports, municipal vending permit registrations, and point-of-sale platform transaction volumes. Historical figures (2021–2024) reflect actuals; 2025 is the base year; 2026–2035 are MRFR projections.