Fresh Cherries Market Summary

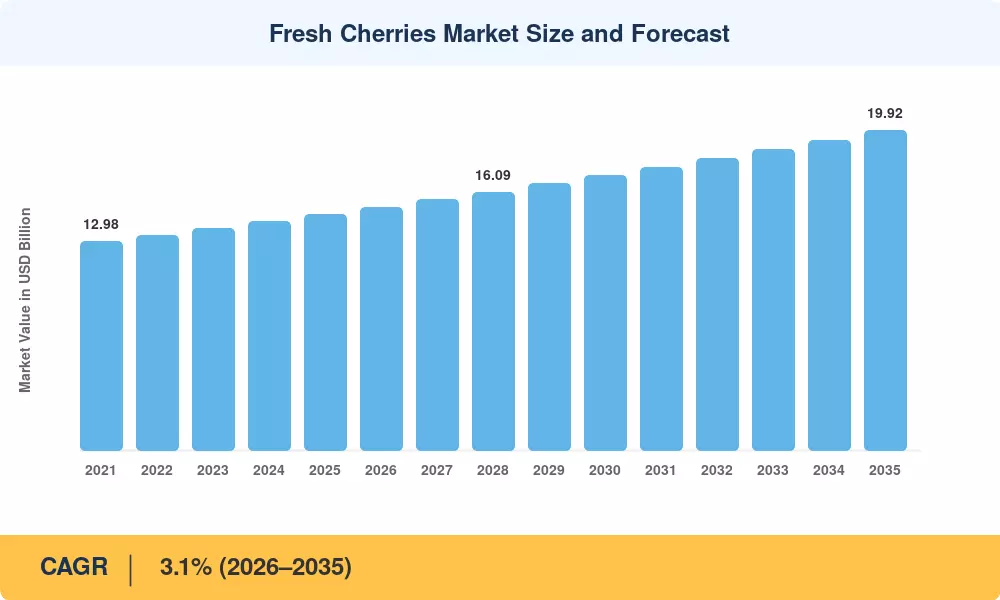

The fresh cherries market reached a valuation of USD 14.68 billion in 2025 and is projected to grow from USD 15.14 billion in 2026 to USD 19.92 billion by 2035, registering a CAGR of 3.1% during the forecast period. Rising consumer preference for nutrient-rich stone fruits, combined with government-backed cold-chain infrastructure programs across major producing nations, continues to fuel this upward trajectory. Fresh cherry export and import volumes expanded by over 8% between 2022 and 2024 alone, driven largely by bilateral trade agreements between Chile, China, and the United States [2].

A technology-led transformation is reshaping how cherry stone fruit harvesting takes place across commercial orchards. Traditional hand-picking operations—still dominant in parts of Europe and Turkey—are giving way to high-density trellised orchard systems paired with mechanical harvesters and AI-enabled optical sorters. The USDA's Specialty Crop Block Grant Program allocated USD 72.9 million in 2024 toward post-harvest innovation, a significant portion of which targeted controlled-atmosphere storage and modified-atmosphere packaging for sweet and sour cherry varieties [3].

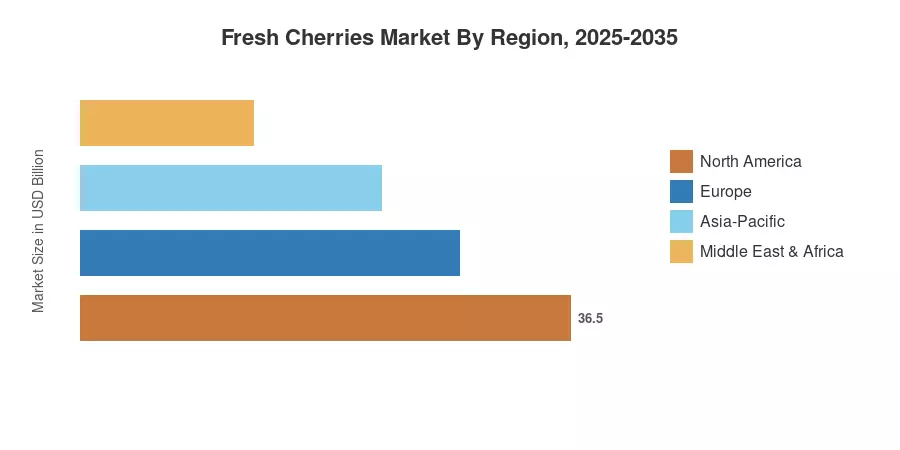

Asia-Pacific commands the largest share of the fresh cherries market at approximately 30.5% of global value, led by China's massive domestic consumption base. South America is the fastest-growing region, expanding at a 2.7% CAGR through 2035 as Chilean and Argentine exporters invest in counter-seasonal supply chains. Europe holds roughly 26% of the global fresh cherries market, anchored by Turkey, Spain, and Italy—three nations where Bing and Rainier cherry types are cultivated at scale for both domestic and export channels [4]. The decade ahead will be shaped by precision agriculture adoption and evolving consumer expectations around traceability and cherry antioxidant properties.

Key Report Takeaways

• By Type

- Sweet cherries accounted for approximately 68% of the fresh cherries market in 2025, reflecting consumer demand for premium dessert-grade fruit across North America and Asia-Pacific

- Sour/tart cherry varieties are expanding at a 3.6% CAGR, fueled by growing use in functional beverages, dietary supplements, and baked goods

• By Distribution Channel

- Supermarkets and hypermarkets generated an estimated USD 6.45 billion in fresh cherry sales in 2025, reinforcing their dominance as the primary retail touchpoint for the fresh cherries market

- Online retail channels are registering the fastest growth at 4.8% CAGR, supported by direct-to-consumer farm box subscriptions and cold-chain last-mile logistics

• By Region

- Asia-Pacific held 30.5% of the fresh cherries market share in 2025, driven by China's domestic production exceeding 4.5 million metric tons annually

- South America is projected to record a 2.7% CAGR through 2035, with Chilean exporters capitalizing on counter-seasonal demand windows

- North America contributed approximately USD 3.52 billion to the fresh cherries market in 2025

Fresh Cherries Market Size and Forecast (2021–2035)

MRFR's market sizing methodology combines top-down revenue estimation with bottom-up production volume analysis across 42 cherry-producing countries. Historical data draws on FAO production statistics, UN Comtrade bilateral trade records, and proprietary grower surveys. Forecast projections apply econometric modeling adjusted for climate variability, orchard expansion rates, and per-capita consumption trends in key import markets[5].