Green Cement Market Summary

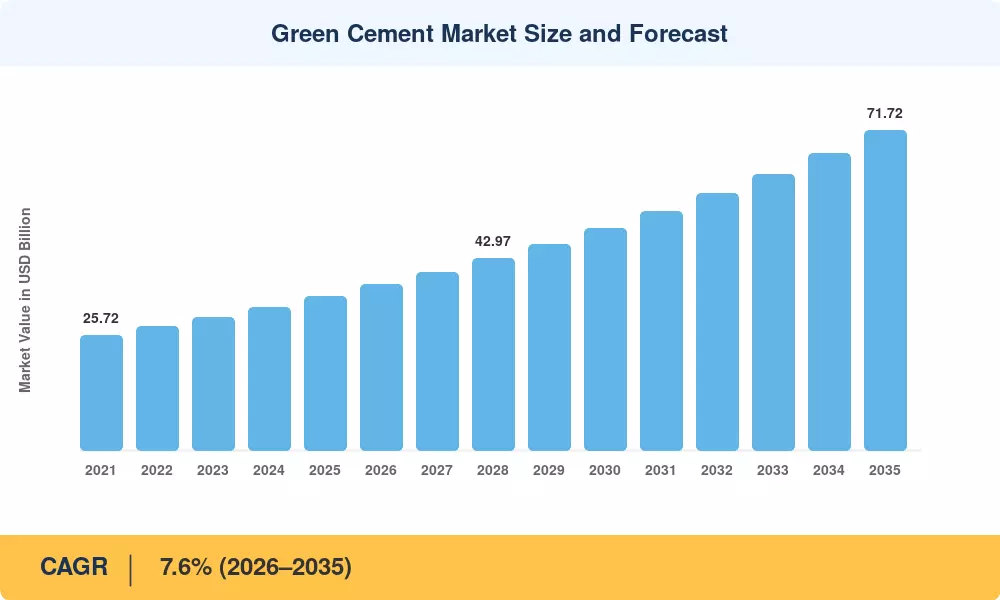

The Green Cement Market reached an estimated USD 34.50 Billion in 2025, is projected to touch USD 37.09 Billion in 2026, and is on course to climb to USD 71.72 Billion by 2035 at a 7.6% CAGR across the 2026–2035 forecast window. This trajectory reflects a structural shift: the EU Carbon Border Adjustment Mechanism (CBAM), now covering cement imports, and the U.S. Inflation Reduction Act's Buy Clean provisions have turned procurement specifications into the single largest growth catalyst for the Green Cement Market [1][2]. Carbon pricing mechanisms active in over 40 national jurisdictions push producers to reformulate or face margin erosion.

Traditional ordinary Portland cement — responsible for roughly 8% of global CO₂ emissions — is steadily losing specification share to blended and geopolymer alternatives. The International Energy Agency's Net Zero Roadmap calls for a 40% cut in direct cement-sector emissions by 2030, a target that has unlocked more than USD 12 billion in cumulative capital commitments toward kiln electrification, carbon-capture retrofit, and clinker-substitution capacity since 2022 [3][4]. Low-carbon cement formulations now account for a growing slice of tender-stage material lists in both public infrastructure and commercial real estate.

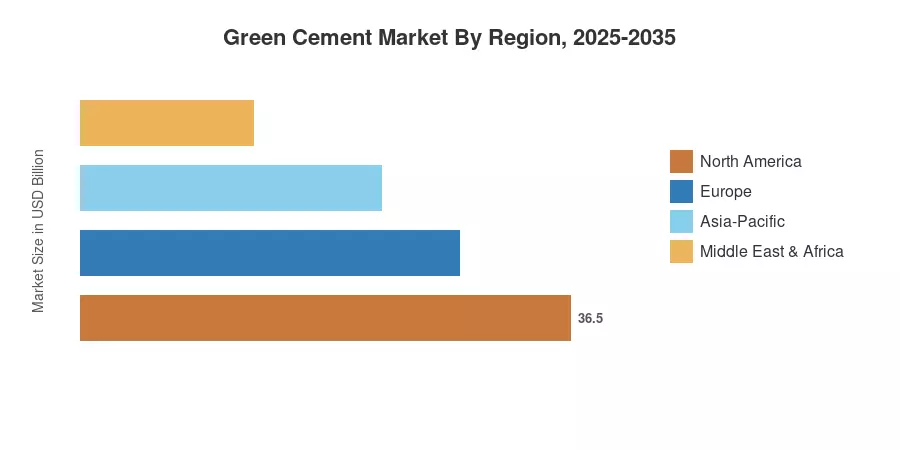

North America held approximately 34.0% of the Green Cement Market revenue in 2025, anchored by federal and state-level Buy Clean mandates. Asia-Pacific posted the fastest regional expansion, registering an 8.6% CAGR, driven by China's dual-carbon policy and India's green-building code revisions. Europe maintained the second-largest revenue position at USD 9.14 billion, underpinned by the EU Emissions Trading System and national green-public-procurement frameworks. The decade ahead will reward companies that lock in supplementary cementitious material supply chains early.

Key Report Takeaways

• By Product Type

- Fly-ash-based cement commanded a 46.8% share of the Green Cement Market in 2025, reflecting thermal-power-plant by-product availability and established blending standards.

- Slag-based cement is forecast to expand at an 8.3% CAGR through 2035, supported by rising blast-furnace-slag recovery in steelmaking regions.

- Limestone-based formulations accounted for approximately USD 5.18 billion in 2025, gaining traction where fly ash supply is constrained.

• By Construction Sector

- Non-residential works represented 62.3% of the Green Cement Market in 2025, led by commercial, institutional, and infrastructure projects subject to green-procurement mandates.

- Residential construction is projected to achieve a 7.1% CAGR through 2035 as green-building certification programs expand into single-family housing.

• By Region

- North America retained a 34.0% revenue share of the Green Cement Market, supported by early policy adoption and robust supply-chain maturity.

- Asia-Pacific registered the fastest CAGR at 8.6%, with China and India together accounting for over 60% of regional demand growth.

Green Cement Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining top-down demand modeling from construction output databases, bottom-up production data from cement-industry associations, and cross-validation against publicly reported revenues of leading producers. All values are expressed in USD Billion at constant exchange rates.