Head Mounted Display Market Summary

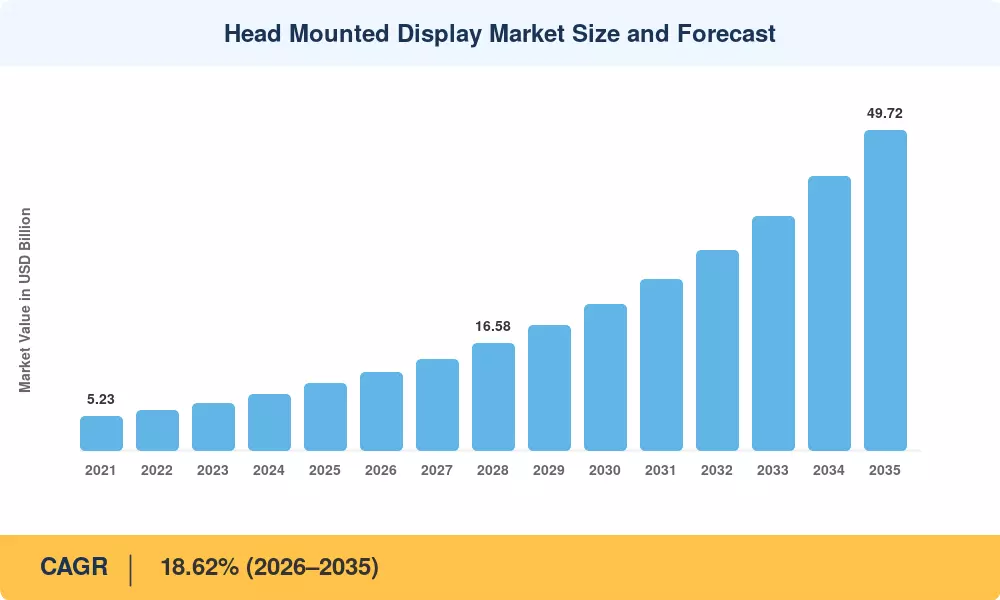

The Head Mounted Display Market reached USD 10.36 billion in 2025, with the forecast period beginning at USD 12.14 billion in 2026 and climbing to USD 49.72 billion by 2035 at an 18.62% CAGR. Defense modernization spending across NATO and Indo-Pacific alliances — exceeding USD 14 billion in combined mixed-reality helmet procurement budgets through 2030 — anchors this trajectory alongside expanding industrial metaverse programs that create diversified demand for immersive HMD devices[2]. The Head Mounted Display Market benefits from simultaneous pull across military, healthcare, and consumer entertainment verticals, a rare convergence that insulates the growth path from single-sector cyclicality.

A generational shift in near-eye display systems is replacing legacy binocular night-vision goggles and basic safety visors with sensor-fused, AI-enhanced headsets. The U.S. Army's Integrated Visual Augmentation System alone carries a USD 21.9 billion ceiling contract, while the European Commission's Horizon Europe program has earmarked over EUR 1.2 billion for XR research through 2027 [3][4]. Micro-OLED panels, foveated rendering engines, and pancake lens stacks are collapsing device weight below 300 grams, making wearable display technology practical for eight-hour surgical and field-service shifts.

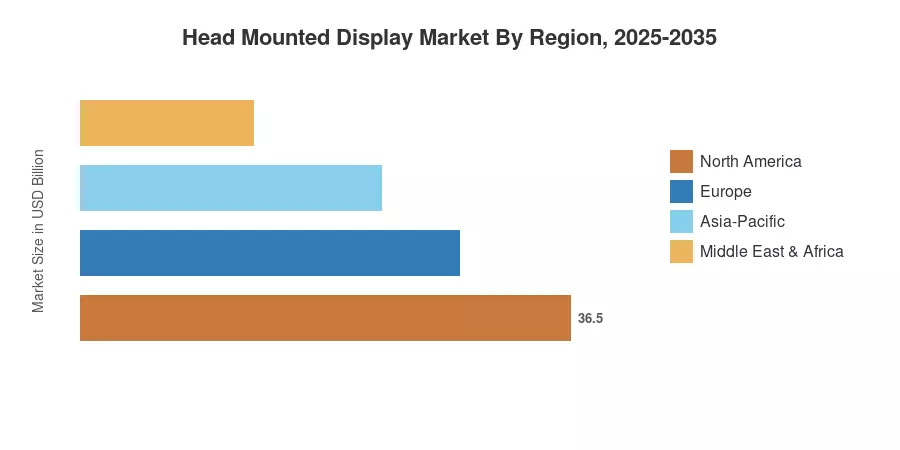

Asia-Pacific dominates with roughly 35.4% of global revenue, driven by Chinese OEM scale and Japan's precision optics supply chain. North America is the fastest-growing region at a 19.08% CAGR, powered by Pentagon procurement and Silicon Valley R&D. Europe holds the second-largest share, near 27.8%, buoyed by Airbus and BAE Systems partnerships embedding AR VR headset displays into aerospace maintenance workflows The Head Mounted Display Market is positioned for sustained double-digit expansion as 5G-native smart glasses display platforms unlock untethered enterprise use cases through the decade.

Key Report Takeaways

• By Technology

- Virtual Reality commanded 65.2% of the Head Mounted Display Market in 2025, supported by gaming ecosystem maturity and esports subscription revenue

- Augmented Reality is forecast to expand at a 20.48% CAGR through 2035, fueled by enterprise field-service adoption of smart glasses display form factors

• By Connectivity

- Wired/ Tethered systems held USD 5.94 billion in revenue during 2025, though Wireless/ Standalone units are growing at a 22.85% CAGR as 5G and Wi-Fi 7 enable untethered immersive HMD devices

• By Product Type

- Wired/tethered systems held USD 5.94 billion in revenue during 2025, though wireless/standalone units are growing at a 22.85% CAGR as 5G and Wi-Fi 7 enable untethered immersive HMD devices

- Helmet-mounted displays represented 82.1% of the Head Mounted Display Market size in 2025, while Wearable Glasses are advancing at a 23.45% CAGR

• By End User

- Consumer applications accounted for 73.8% of demand in 2025

• By Application

- Consumer applications accounted for 73.8% of demand in 2025

- Healthcare is progressing at a 22.07% CAGR, driven by surgical navigation and medical training simulators that rely on near-eye display systems

• By Region

- Asia-Pacific captured 35.4% of global revenue in 2025

- North America shows the strongest growth at a 19.08% CAGR to 2035, reflecting defense budget allocations for AR VR headset displays

- The Head Mounted Display Market in Europe held 27.8% share, with Germany and the UK leading adoption

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework triangulates vendor revenue disclosures, component shipment data from panel and sensor suppliers, and demand-side surveys across defense, healthcare, and consumer electronics channels. Historical figures draw on audited financials and customs trade data, while the forecast applies a bottom-up build validated against top-down macro benchmarks for the Head Mounted Display Market.

.webp?v=1783425169)