Healthcare Chatbots Market Summary

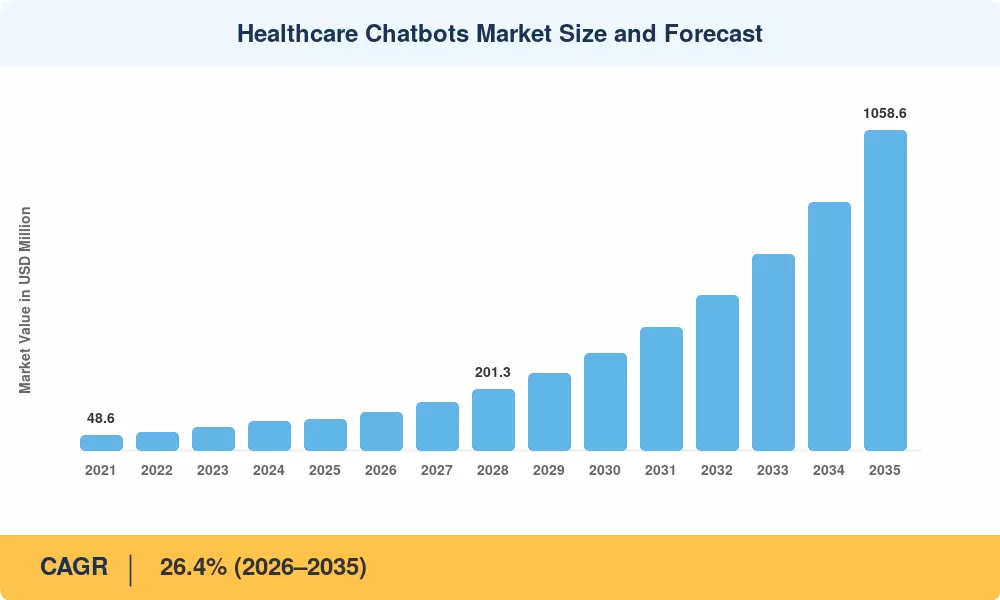

The Healthcare Chatbots Market closed 2025 at roughly USD 101.8 Million and is projected to begin its 2026 forecast year near USD 126.5 Million, climbing to approximately USD 1,058.6 Million by 2035 at a 26.4% CAGR across the 2026–2035 window. Two catalysts anchor this trajectory: chronic clinician shortages flagged by the World Health Organization, and reimbursement clarity emerging from CMS digital-health coding updates that finally make conversational tools billable rather than experimental. Buyers in the Healthcare Chatbots Market now treat these systems as front-door infrastructure, not pilots.

Legacy interactive voice response systems and static patient portals are giving way to AI patient triage bots that interpret free-text symptoms and route patients intelligently. Hospitals once relied on call-center scripts; they now deploy a virtual health assistant layer that integrates directly with electronic health records. Venture funding exceeding USD 1.4 billion across conversational health startups since 2023 has accelerated this shift, pushing symptom checker chatbot capabilities from novelty toward clinical workflow.

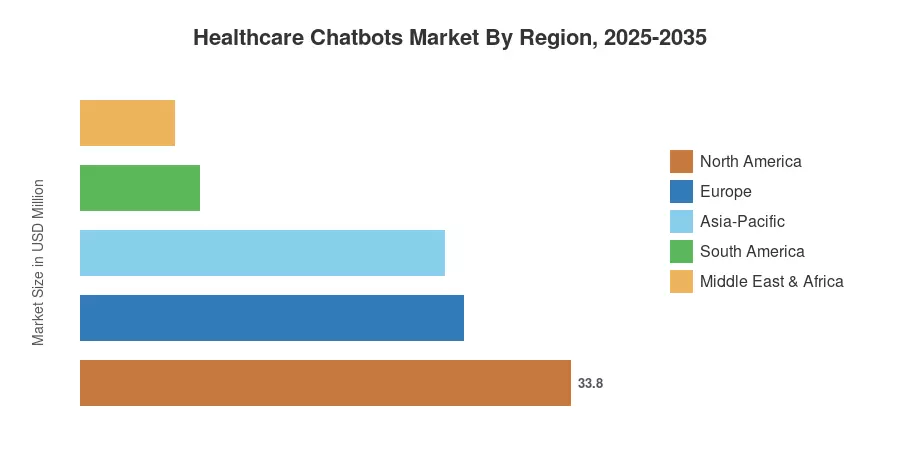

North America holds the dominant position with a 33.8% revenue share, supported by mature EHR connectivity and payer adoption. Asia-Pacific ranks as the fastest-growing region at a 27.6% CAGR as smartphone penetration closes care-access gaps. Europe stands as the second-largest contributor, propelled by GDPR-aligned conversational AI for clinic deployments. The decade ahead favors vendors that pair clinical safety with measurable patient engagement automation.

Key Report Takeaways

• By Component

- Software dominated the Healthcare Chatbots Market with a 67.9% revenue share in 2025, remaining the principal revenue engine

• By Deployment

- Cloud deployments grew at a 26.0% CAGR, the fastest architecture tier as health systems prioritize elasticity

- Hybrid deployment models represent an emerging USD 14.2 Million opportunity tied to data-sovereignty demands

• By Application

- Symptom checking and triage applications held 44.1% of the Healthcare Chatbots Market in 2025, the largest application slice

- Mental-health coaching applications are advancing at a 28.1% CAGR through 2035

• By End-User

- Healthcare providers contributed USD 47.4 million in 2025 revenue as the leading end-user group

- Patients and caregivers form the fastest-growing group as self-service expectations and patient engagement automation reshape how individuals interact with the health system.

• By Region

- North America retained a 33.8% share of the Healthcare Chatbots Market in 2025

- Asia-Pacific is expanding at a 27.6% CAGR, the fastest regional pace

- Europe generated USD 26.9 Million in 2025, ranking as the second-largest regional contributor

Market Size and Forecast (2021–2035)

Market sizing draws on MRFR's bottom-up methodology, triangulating vendor revenue disclosures, hospital IT procurement data, and payer adoption surveys, then cross-checked against comparable third-party estimates and calibrated within accepted variance bands.