Healthcare Staffing Market Summary

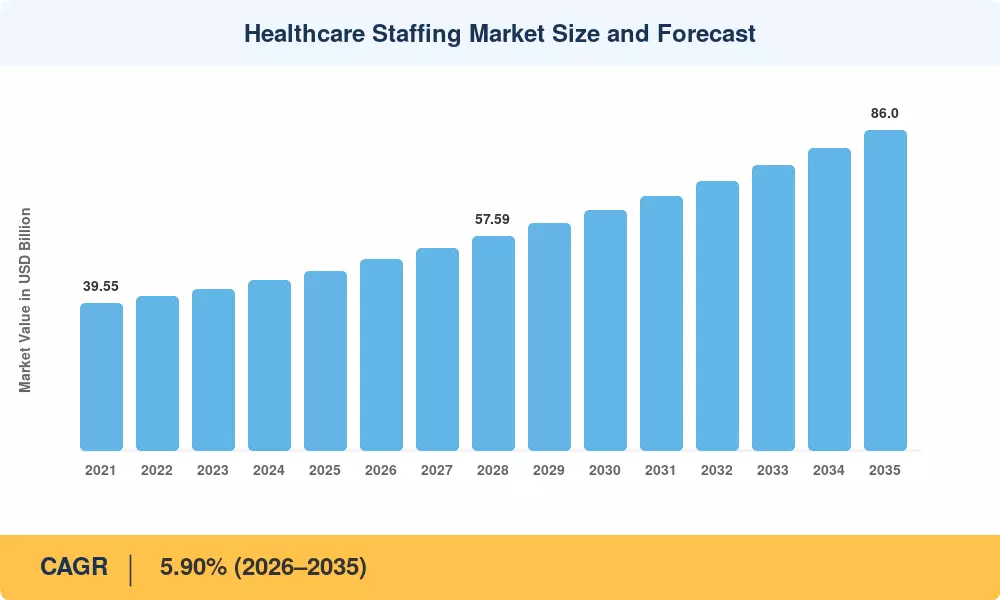

The Global Healthcare Staffing Market size was valued at USD 48.10 Billion in 2025, and the market is projected to grow from USD 51.35 Billion in 2026 to USD 86.00 Billion by 2035, registering a CAGR of 5.90% during the forecast period 2026–2035. Chronic clinician shortages remain the single largest catalyst behind this expansion. The U.S. Bureau of Labor Statistics projects a deficit of over 200,000 registered nurses by 2030 [1], while the Association of American Medical Colleges estimates a physician shortfall of up to 124,000 by 2034 [2]. Federal staffing mandates — including CMS minimum nurse-to-patient ratio proposals — are converting contingent labor from a cost-management tactic into a regulatory imperative, lending structural resilience to the Healthcare Staffing Market.

Technology is reshaping how health systems source and deploy temporary clinicians. Legacy phone-and-fax credentialing workflows are giving way to AI-enabled scheduling platforms and predictive workforce analytics that reduce time-to-fill by 30–40% [3]. Managed service provider frameworks now manage upward of USD 12 billion in annual contingent healthcare spend in North America alone, replacing fragmented vendor relationships with centralized program oversight [4]. These digital investments deepen vendor differentiation and compress premium labor costs even as travel-nurse bill rates normalize from their pandemic peaks.

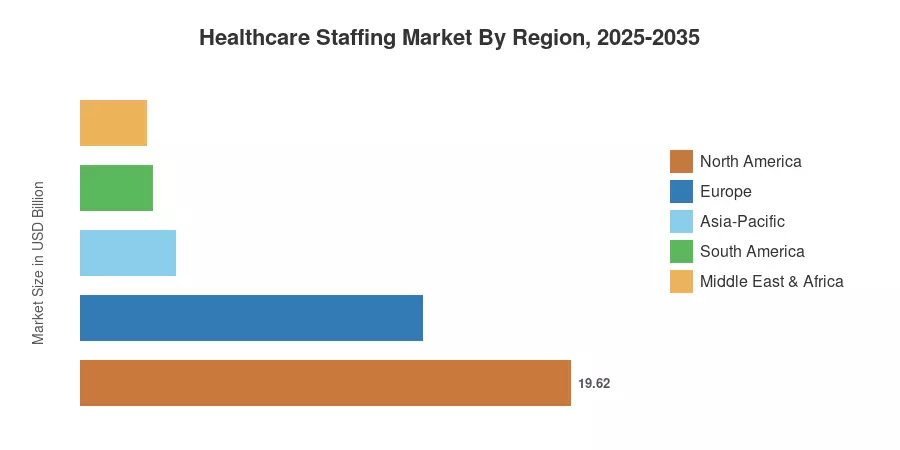

North America commands roughly 40.8% of the Healthcare Staffing Market, driven by high per-capita healthcare expenditure and an entrenched temporary-staffing culture across acute-care facilities. Asia-Pacific represents the fastest-growing geography at a projected 7.9% CAGR, fueled by hospital capacity expansion in India, China, and Southeast Asia. Europe holds the second-largest share at approximately 28.5%, supported by aging demographics and cross-border clinical workforce solutions. The Healthcare Staffing Market is poised for sustained double-digit expansion in emerging regions through 2035.

Key Report Takeaways

• By Service

- Travel nurse staffing accounted for 47.5% of the Healthcare Staffing Market in 2025, reflecting sustained demand for rapid-deployment clinical coverage across acute-care settings.

- Locum tenens is the fastest-growing service segment, projected to expand at an 8.8% CAGR through 2035 as physician shortages intensify in rural and underserved geographies.

• By End-User

- Hospitals represented 45.2% of total Healthcare Staffing Market revenue in 2025, driven by high-acuity patient volumes and regulatory nurse-ratio mandates.

- Home-health agencies are projected to grow at a 9.7% CAGR, making them the fastest-expanding end-user category as care delivery shifts to post-acute and community-based settings.

• By Region

- North America generated 40.8% of the Healthcare Staffing Market revenue in 2025.

- Asia-Pacific is forecast to register a 7.9% CAGR through 2035, underpinned by government-led hospital construction initiatives and rising private insurance penetration.

Healthcare Staffing Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated research methodology combining bottom-up revenue modeling from agency-level billing data, top-down macroeconomic calibration against national healthcare expenditure statistics, and cross-validation with publicly filed financials of leading staffing firms. The Healthcare Staffing Market size estimates below reflect this blended approach.