High Purity Gas Market Summary

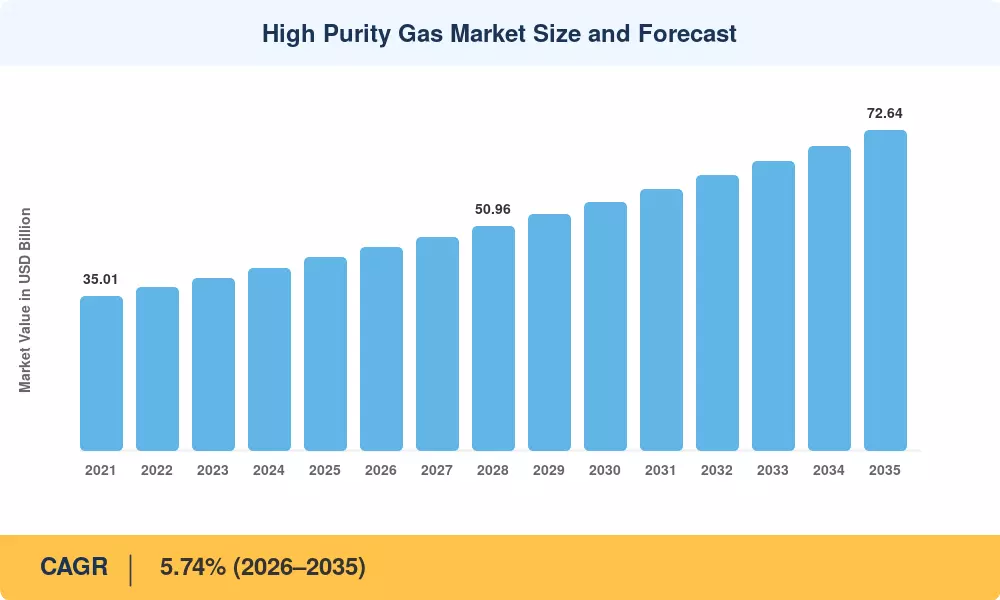

The High Purity Gas Market reached USD 43.78 billion in 2025 and is projected to grow from USD 46.12 billion in 2026 to USD 72.64 billion by 2035, registering a CAGR of 5.74% across the forecast period. Semiconductor fabrication expansion across East Asia — anchored by over USD 380 billion in committed fab investments through 2030 — and the parallel scale-up of green-hydrogen electrolyzer installations are the two primary demand engines driving ultra-high-purity gases consumption[2]. Government incentives such as the U.S. CHIPS and Science Act and the EU Chips Act are locking in multi-year supply agreements for electronic-grade gases well ahead of production timelines.

The industrial gas filtration space is witnessing a fundamental shift. We upgrade legacy cryogenic air separation machines, many built prior to 2010, with membrane-based and molecular-sieve polishing modules to reach the sub-ppb contamination thresholds required by 3 nm and 2 nm semiconductor process gas requirements [3]. AI-driven purity-analytics platforms, now used by at least four of the top five suppliers, are reducing analyzer downtime by 30–40% and increasing product recovery rates, providing a clear cost advantage for early adopters in the compressed specialty gases category.

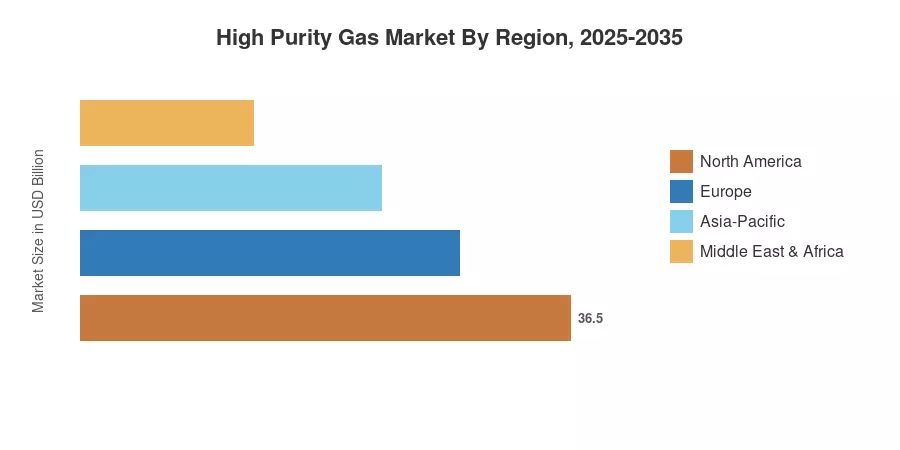

Asia-Pacific dominates the High Purity Gas Market with about 42% share due to fab clusters in Taiwan, South Korea and mainland China. The region also registers the quickest CAGR of 5.62% through 2035, on account of the need for electrolyzer-grade high-purity nitrogen. North America is second, with a roughly 26% share, fueled by the reshoring of semiconductor capacity and increased biopharma fill-finish activity. Europe is a close second on the back of the continent’s fast green-hydrogen corridor buildout and stringent medicinal gas purity regulations [4][5].

Key Report Takeaways

• By Product Type

- High-purity atmospheric gases held a 44.18% revenue share of the High Purity Gas Market in 2025, underpinned by nitrogen, oxygen, and argon demand from semiconductor and metal-production end users

- Noble gases are set to expand at a 6.15% CAGR through 2035, with helium and neon supply constraints accelerating on-site recycling investments in the High Purity Gas Market

- Carbon gases reached USD 5.83 billion in 2025, driven by CO₂ purification needs in food-grade and analytical grade gases applications

• By Application

- Insulation applications captured a 31.72% share of the High Purity Gas Market in 2025, led by SF₆ alternatives and specialty blends for switchgear

- Coolant applications are advancing at a 6.32% CAGR, supported by liquid-nitrogen and liquid-helium use in MRI systems and quantum-computing cryogenics

• By End-User Industry

- Electronics commanded 33.56% of the High Purity Gas Market in 2025, reflecting fab-level consumption of semiconductor process gases

- Medical and healthcare is the fastest-growing end-user segment at a 5.98% CAGR, fueled by rising demand for medical specialty gases in cell-and-gene-therapy manufacturing

• By Region

- Asia-Pacific accounted for 42.15% of 2025 revenue in the High Purity Gas Market and is expanding at a 5.62% CAGR

- North America contributed approximately USD 11.38 billion in 2025, driven by reshored fab capacity and laboratory gases demand

Market Size and Forecast (2021–2035)

The forecasts mentioned below are based on Market Research Future’s (MRFR) patented bottom-up methodology, triangulated against primary interviews of gas suppliers, fab procurement managers and electrolyzer OEMs. Historical statistics (2021–2024) are based on audited revenue declarations from publicly listed industrial gas firms; projection years are based on a calibrated CAGR and adjusted for projected capacity expansions and demand shifts dictated by policy.