High Purity Alumina Market Summary

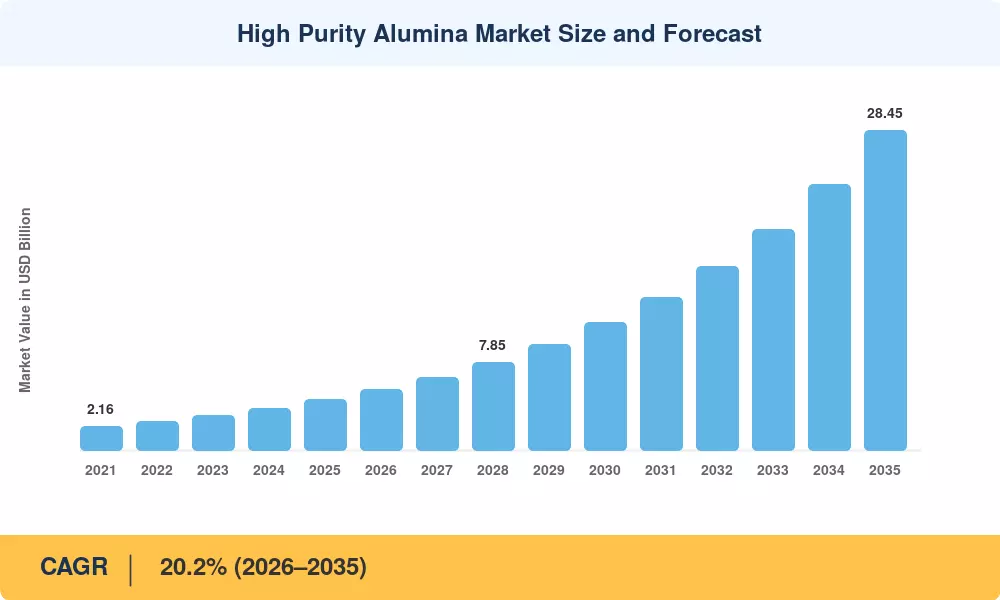

The High Purity Alumina Market reached a valuation of USD 4.52 billion in 2025 and is projected to grow from USD 5.43 billion in 2026 to USD 28.45 billion by 2035, registering a CAGR of 20.2% across the forecast period (2026–2035). This acceleration is anchored by two converging forces: the U.S. Inflation Reduction Act's USD 6 billion allocation for critical-mineral processing [2] and the European Critical Raw Materials Act mandating that at least 10% of strategic mineral refining occur domestically by 2030 [3]. Both policies are funneling capital directly into high-grade aluminum oxide refining infrastructure, creating a multi-year demand runway that commodity alumina simply cannot serve.

A structural technology shift is redefining the supply landscape. Legacy Bayer-process alumina plants—designed for metallurgical-grade output—are being supplanted by hydrolysis and acid-leaching facilities capable of delivering 4N to 6N purity thresholds. BloombergNEF estimates that global capital commitments to specialty alumina powder refining exceeded USD 2.8 billion between 2023 and 2025 [4], driven by the explosion of lithium-ion battery materials demand and the proliferation of LED substrate materials for micro-LED displays. Electronic ceramic materials and sapphire glass materials applications are further broadening the addressable market for producers who can guarantee impurity levels below 10 ppm.

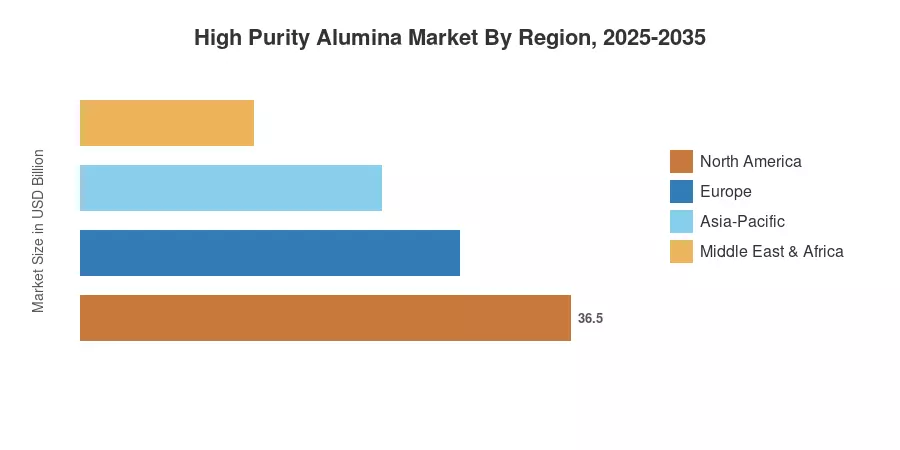

Asia-Pacific commands a dominant 70.1% share of the High Purity Alumina Market in 2025, powered by China's vertically integrated LED and battery supply chains. The region also represents the fastest-growing region at a 21.2% CAGR to 2035, followed by North America (14.8% share) where onshoring incentives are catalyzing greenfield plants. Europe accounts for roughly 9.3% of demand, buoyed by the EU Battery Regulation's separator-purity mandates. As electric-vehicle adoption accelerates globally, the High Purity Alumina Market is poised to remain in structural undersupply through at least 2028, sustaining premium pricing for grades above 5N purity.

Key Report Takeaways

• By Purity Level

- The 4N purity grade captured 67.5% of the High Purity Alumina Market share in 2025, underpinned by large-volume LED substrate materials and phosphor applications.

- The 6N grade is forecast to expand at a 24.1% CAGR through 2035, driven by semiconductor materials requiring sub-ppm impurity specifications.

• By Production Technology

- Hydrolysis accounted for 81.2% of global output volume in 2025, reflecting its cost advantage in processing aluminum alkoxide precursors.

- Hydrochloric-acid leaching is the fastest-growing production route at a 24.2% CAGR to 2035, favored for battery separator coatings feedstock.

• By Application

- LED lighting represented 50.7% of the High Purity Alumina Market in 2025, though its share is declining as newer applications scale.

- Lithium-ion battery applications are surging at a 52.4% CAGR, the fastest segment, as battery separator coatings become standard in EV cell design.

• By Region

- Asia-Pacific held a 70.1% share in 2025, with China alone accounting for over half of the regional consumption of electronic-grade materials.

- North America is advancing at a 22.8% CAGR to 2035, propelled by IRA-linked incentive structures and nearshoring of semiconductor materials supply chains.

Market Size and Forecast (2021–2035)

MRFR's estimates are built on a triangulated methodology combining primary interviews with 45+ industry participants, customs-trade databases, and plant-level capacity audits across 12 countries. Historical figures reflect reported shipments adjusted for inventory restocking; forecast values apply a compound growth framework calibrated against announced capacity expansions and off-take agreements.