High Temperature Coatings Market Summary

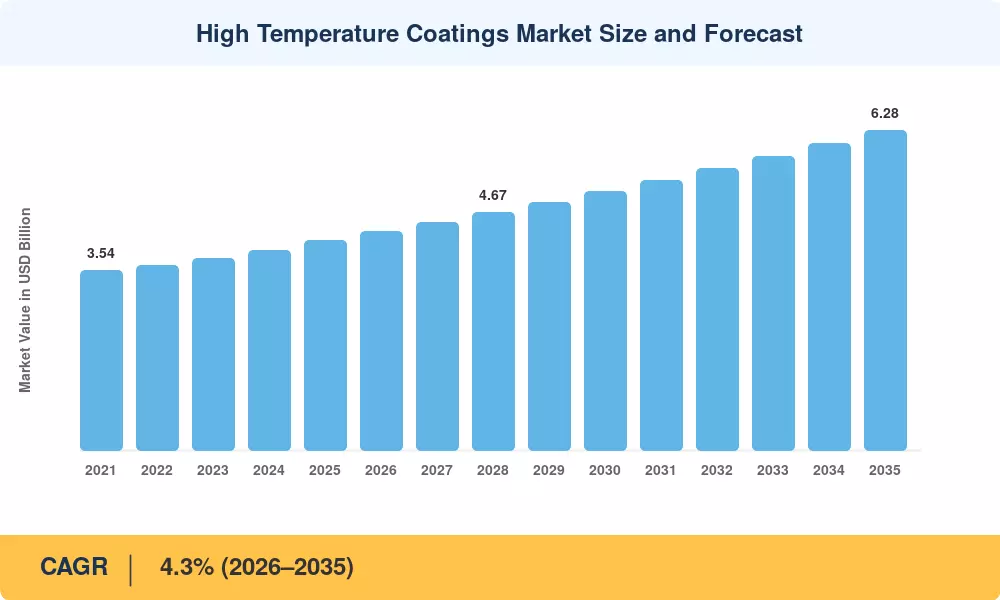

The High Temperature Coatings Market reached an estimated USD 4.12 Billion in 2025 and is projected to grow from USD 4.29 Billion in 2026 to USD 6.28 Billion by 2035, registering a CAGR of 4.3% during the forecast period (2026–2035). Rapid industrialization across developing economies and rising capital expenditure in petrochemical processing infrastructure are anchoring this growth trajectory. Government-backed programs aimed at upgrading aging refinery assets — particularly the US Department of Energy's Industrial Decarbonization Roadmap and China's 14th Five-Year Plan for the chemical sector — have created a sustained demand floor for specialized protective solutions [1][2].

The market for high-temperature coatings is changing due to a significant technological change. As authorities tighten emission restrictions for volatile organic compounds (VOCs), water-based and powder-based alternatives are gradually replacing legacy solvent-heavy formulations. Manufacturers are being forced to reformulate as a result of the European Union's updated Industrial Emissions Directive (IED), which will take effect in 2024 and reduce allowed VOC values for coating processes by 30% [3]. The urgency of this shift is demonstrated by the fact that global expenditure in low-emission coating research and development exceeded USD 1.8 billion in 2024 [4].

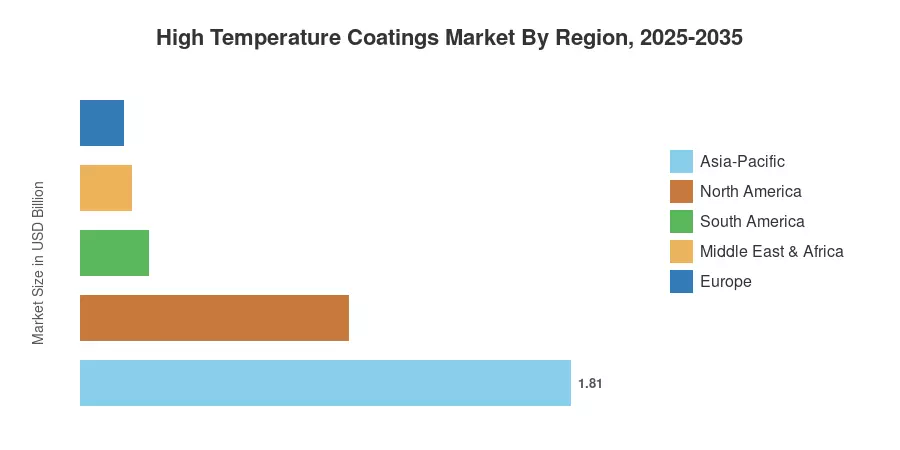

Due to India's drive for infrastructure modernization and China's petrochemical expansion, the Asia-Pacific holds the highest share of the High Temperature Coatings Market, at over 44%. Throughout the predicted period, the region also reports the quickest CAGR. Europe accounts for around 20% of the market, driven by strict emissions compliance regulations throughout its automotive and industrial base. In comparison, North America controls about 24% because to expenditure on aerospace and defense.

Key Report Takeaways

• By Type

- Silicone-based coatings hold the largest revenue share in the High Temperature Coatings Market, reflecting their superior thermal stability at temperatures exceeding 600°C.

- Epoxy formulations are growing at the fastest rate among all coating types, fueled by demand in petrochemical pipeline applications.

- Acrylic and polyester types collectively account for a meaningful share, serving mid-range temperature applications in building facades and exhaust systems.

• By Technology

- Solvent-based technology still leads overall revenue contribution, though its dominance is eroding under regulatory pressure.

- Water-based technology registers the highest CAGR in the High Temperature Coatings Market as manufacturers comply with tightening VOC mandates.

• By End-User Industry

- Petrochemical remains the top-consuming end-user sector, driven by refinery maintenance cycles and capacity additions.

- Aerospace & defense is the second-largest consumer segment, with coating specifications tied to turbine engine OEM requirements.

• By Region

- Asia-Pacific dominates with a 44% market share, propelled by industrial output in China, India, and Japan.

- North America represents approximately 24% of global value, with the US accounting for over 68% of regional demand.

Market Size and Forecast (2021–2035)

Data sourcing for this High Temperature Coatings Market assessment combines primary interviews with coating formulators, raw material suppliers, and end-user procurement teams alongside secondary analysis from trade associations, regulatory filings, and corporate financial disclosures. All historical figures (2021–2024) are validated against import-export databases and production volume records from major manufacturing hubs.