Hopped Malt Extract Market Summary

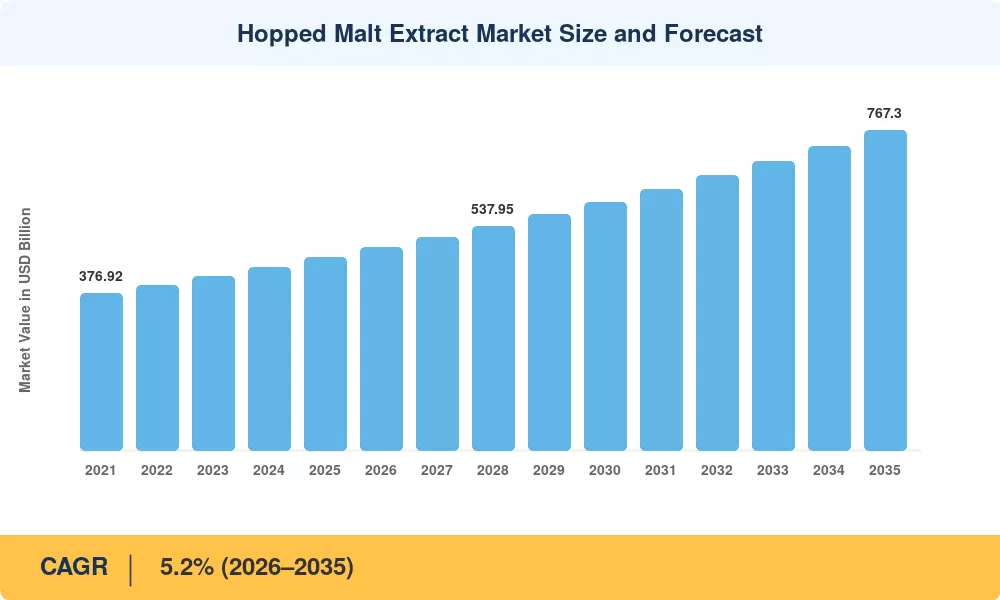

The global hopped malt extract market reached an estimated USD 462.0 million in 2025 and is projected to grow from USD 486.0 million in 2026 to USD 767.3 million by 2035, registering a CAGR of 5.2% across the forecast window. Craft beer production continues to surge worldwide — the Brewers Association reported that U.S. craft volumes grew by 5% in 2024 alone [2] — and that momentum has directly lifted demand for pre-hopped beer brewing extract among small-scale and independent breweries. Government initiatives supporting small beverage enterprises, including the EU's Excise Duty Reform Directive and India's amended brewing-license framework, reinforce the tailwinds pushing this category forward [3].

Beyond traditional brewing, the industry is witnessing a product-innovation wave that replaces manual hop-dosing workflows with standardized bittered malt extract for brewing applications. Contract breweries and brew-on-premise venues are increasingly switching to liquid and dry malt extract formulations that deliver consistent bitterness profiles batch after batch. A 2024 Brewers Journal survey found that 41% of microbreweries in Europe had adopted at least one pre-hopped extract product by year-end, up from 26% in 2021 [4]. This transition is especially pronounced in homebrewing hop malt kits, where convenience-driven consumers value simplified recipes.

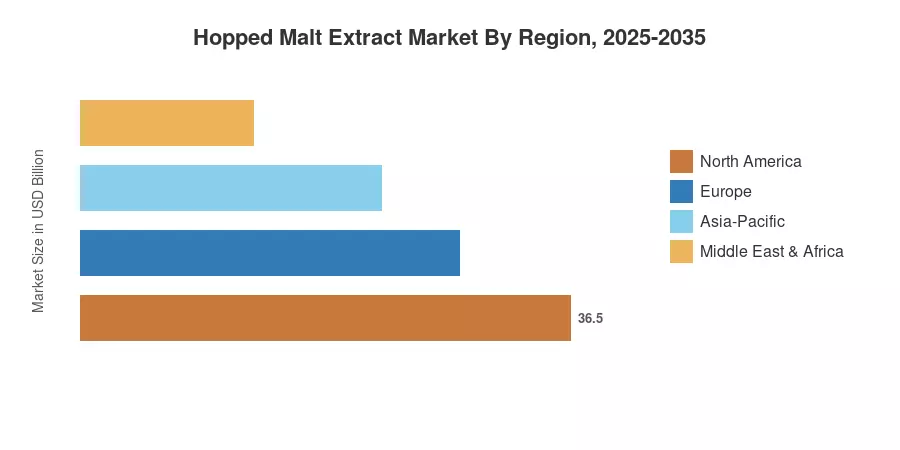

North America commands the largest share of the hopped malt extract market at roughly 34% of global revenue, driven by a mature craft-beer ecosystem and established distribution channels for brewing malt flavors and bitterness products. Asia-Pacific is the fastest-growing region with a projected CAGR of 6.4%, fueled by expanding middle-class beer consumption in China, India, and Southeast Asia. Europe holds the second-largest position at approximately 28%, anchored by heritage brewing cultures in Germany, the UK, and Belgium. Over the coming decade, emerging applications in functional foods and non-alcoholic beverages are expected to unlock incremental revenue streams for the hopped malt extract market across all regions

Key Report Takeaways

• By Form

- Liquid malt extract accounts for approximately 63% of global volume, reflecting its dominance in commercial and contract brewing operations

- Dry malt extract is anticipated to grow at a CAGR of 5.8%, supported by shelf-life advantages in homebrewing hop malt kits and export-oriented channels

• By Application

- The food and beverages segment captures the largest revenue share in the hopped malt extract market, exceeding 57% in 2025

- Pharmaceuticals and cosmetics represent high-growth niches where bittered malt extract from brewing byproducts is repurposed for bioactive compound sourcing

• By Region

- North America leads the hopped malt extract market, supported by over 9,700 operating craft breweries in the United States

- Asia-Pacific's CAGR of 6.4% outpaces all other regions, propelled by rapid urbanization and evolving taste preferences for brewing malt flavors and bitterness profiles

Market Size and Forecast (2021–2035)

MRFR's market-sizing model combines top-down revenue estimates from producer financial disclosures with bottom-up volume reconciliation across five regional clusters. Historical data (2021–2024) relies on customs-trade databases, industry association production logs, and verified distributor invoices. Forecast projections (2026–2035) apply a compound growth model calibrated against macroeconomic indicators for beer consumption, extract-adoption rates, and emerging application penetration.