India Epoxy Resins Market Summary

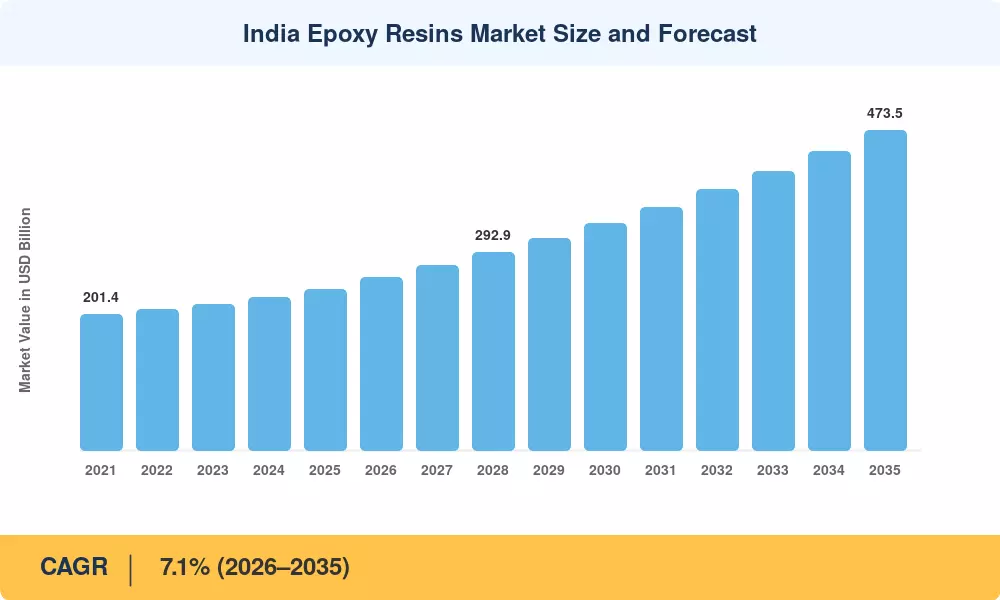

The India Epoxy Resins Market reached an estimated 238.5 kilotons in 2025, and is projected to grow from 255.4 kilotons in 2026 to approximately 473.5 kilotons by 2035, reflecting a compound annual growth rate of 7.1% over the forecast period. Two structural tailwinds anchor this trajectory: the government's Production-Linked Incentive (PLI) scheme for advanced chemistry cell manufacturing and the USD 1.4 trillion National Infrastructure Pipeline, both of which channel heavy downstream demand for protective and structural resin systems [1][2]. The removal of U.S. anti-dumping duties on certain Indian chemical exports in late 2024 has further bolstered domestic producer margins and export competitiveness.

India's resin landscape is in the middle of a materials-science shift. Legacy solvent-borne coating formulations are being displaced by waterborne and high-solid epoxy systems that meet the Bureau of Indian Standards' updated VOC limits (IS 15489:2024) [3]. Large-scale capacity additions — including Aditya Birla Chemicals' 60,000-TPA greenfield line at Vilayat and Atul Ltd's debottlenecking program — signal manufacturer confidence. The India Epoxy Resins Market is also benefiting from a parallel ramp-up of wind-turbine blade manufacturing under the National Wind-Solar Hybrid Policy, which requires high-performance laminating resins [4].

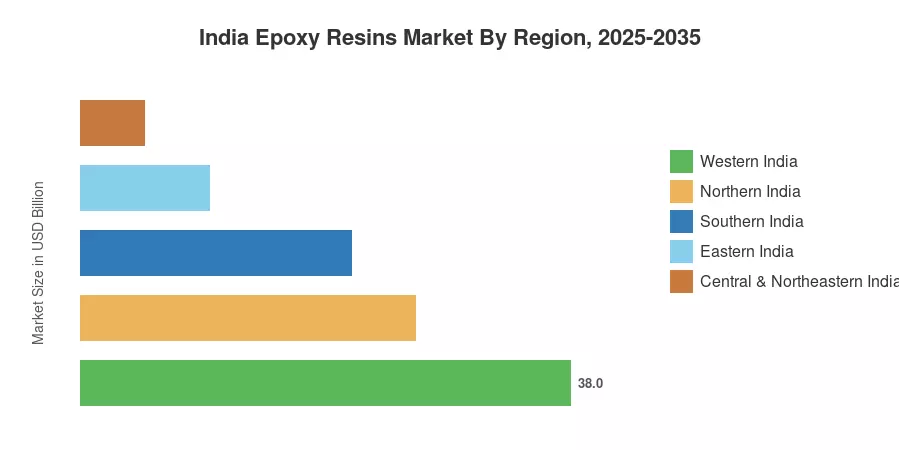

Western India commands roughly 38% of total consumption, anchored by Gujarat's chemical corridor and Maharashtra's automotive-OEM cluster. Southern India is the fastest-growing region, registering a projected CAGR above 8%, driven by electronics-manufacturing hubs in Tamil Nadu and Karnataka. Northern India holds the second-largest share at around 26%, supported by construction and metro-rail expansion across the National Capital Region. As India targets a USD 5 trillion economy, the India Epoxy Resins Market stands to benefit from every pillar of that growth ambition.

Key Report Takeaways

• By Raw Material

- DGEBA (Bisphenol A diglycidyl ether) accounted for approximately 60% of India Epoxy Resins Market volume in 2025, reinforcing its status as the default building-block chemistry for protective and structural applications.

- Novolac-based epoxies are advancing at the strongest growth rate among raw-material segments, propelled by demand from high-temperature electrical laminates and aerospace prepregs.

- DGEBF resins held a volume share of roughly 11% in 2025, favored in low-viscosity flooring and tank-lining formulations.

• By Application

- Paints and coatings represented the largest end-use segment of the India Epoxy Resins Market in 2025, registering a CAGR of approximately 8.9% through 2035.

- Adhesives and sealants are forecast to reach 71 kilotons by 2035, fueled by lightweight bonding trends in automotive and rail coach manufacturing.

- The composites application segment is growing at a CAGR of roughly 9.3%, the fastest among all application categories, driven by wind-energy and defense orders.

• By Region

- Western India contributed about 38% of India Epoxy Resins Market consumption in 2025.

- Southern India is projected to register a CAGR of 8.2% through 2035, the highest of any Indian region.

Market Size and Forecast (2021–2035)

Market Research Future's volume model integrates production-capacity filings from India's Department of Chemicals and Petrochemicals, import–export data from the Directorate General of Commercial Intelligence and Statistics (DGCI&S), and proprietary demand-side surveys across 120+ resin converters and formulators. Historical figures (2021–2024) are reconciled against actual plant utilization rates, while forecast values (2026–2035) embed announced capacity expansions and policy-driven demand scenarios for the India Epoxy Resins Market.

.webp?v=1784027892)