Epoxy Resin Market Summary

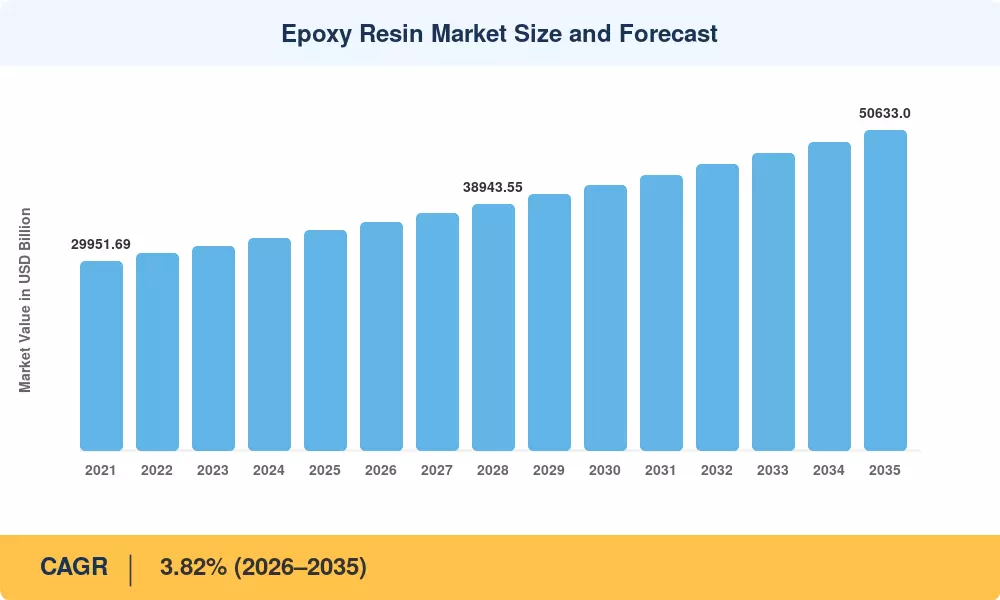

The global Epoxy Resin Market reached an estimated USD 34,800 million in 2025 and is projected to climb from USD 36,130 million in 2026 to USD 50,633 million by 2035, registering a CAGR of 3.82% during 2026–2035. This trajectory reflects sustained capital allocation toward renewable-energy infrastructure—particularly wind-turbine blade manufacturing—and a global push for electrification that demands high-reliability thermosetting resin materials in power electronics and battery enclosures[2]. Government stimulus packages in the United States, China, and the European Union continue to earmark billions of dollars for grid modernization and highway rehabilitation, directly boosting consumption of industrial coating resins and adhesive resin compounds.

Technology is impacting the Epoxy Resin Market with legacy solvent-borne formulations being replaced by waterborne, bio-circular and low-VOC chemistries. Since 2022, resin manufacturers have invested over $2.4 billion in total on next-generation laminating resin systems [3] because of stricter rules on exposure to bisphenol A and volatile organic compounds. These investments target recyclable thermoset chemistries and plant-based feedstocks that can meet both performance standards and sustainability mandates.

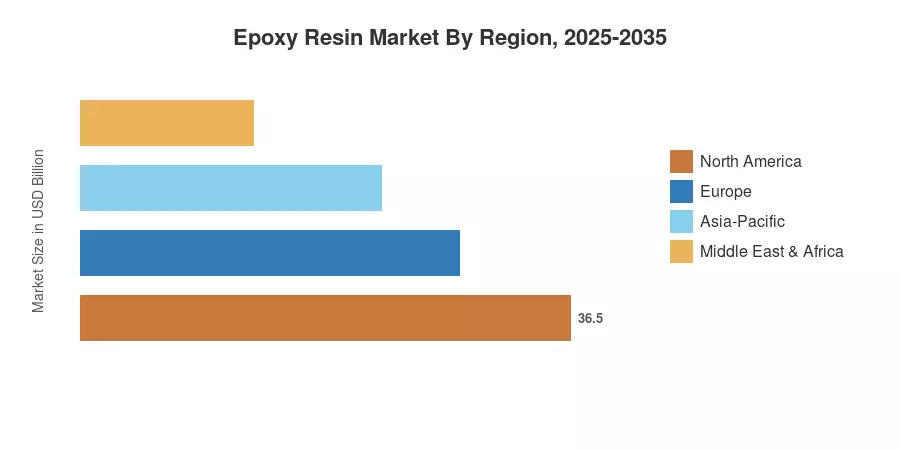

Asia-Pacific holds approximately 43.8% of the Epoxy Resin Market, aided by China’s construction boom and India’s infrastructure expansion. Europe is a little behind at around 23.2% share, driven by wind energy and environmental regulations that are speeding up the use of protective coating chemicals. North America has a stake of around 22.5%, owing to the reshoring of semiconductor manufacture. The market will travel on an upward trend till 2035 due to the rising demand for composite resin materials in aerospace and automotive lightweighting in the next few years [4][5].

Key Report Takeaways

• By Raw Material

- DGBEA (Bisphenol A and ECH) resins captured approximately 39.5% of the Epoxy Resin Market in 2025, driven by their versatility in industrial coating resins and adhesive resin compounds.

- Bio-based and cycloaliphatic grades are forecast to expand at a 7.18% CAGR through 2035, reflecting heightened demand for specialty resin chemicals that comply with evolving BPA regulations.

- Novolac epoxy resins continue to anchor the Epoxy Resin Market for high-temperature electrical insulation resins, particularly in semiconductor packaging.

• By Application

- Paints and coatings held a 54.2% share of the Epoxy Resin Market in 2025, underpinned by infrastructure rehabilitation programs globally.

- Composites represent the fastest-growing application segment at a 5.95% CAGR, fueled by wind-energy and aerospace demand for composite resin materials.

• By Geography

- Asia-Pacific accounted for 43.8% of the Epoxy Resin Market in 2025 and is projected to post a 6.55% CAGR through 2035.

- North America's growth is propelled by semiconductor fab construction and highway refurbishment programs that consume large volumes of construction resin products.

Epoxy Resin Market Size and Forecast (2021–2035)

MRFR’s market sizing technique involves triangulating supply-side shipment data from resin producers, downstream procurement quantities of coating and adhesive manufacturers, and import-export customs databases spanning 42 countries. Historical numbers are based on audited yearly reports and official statistical yearbooks. Forecast estimates are based on regression models, calibrated to industrial production indices, trends in construction permits and energy-investment roadmaps[6].