Industrial Vacuum Cleaner Market Summary

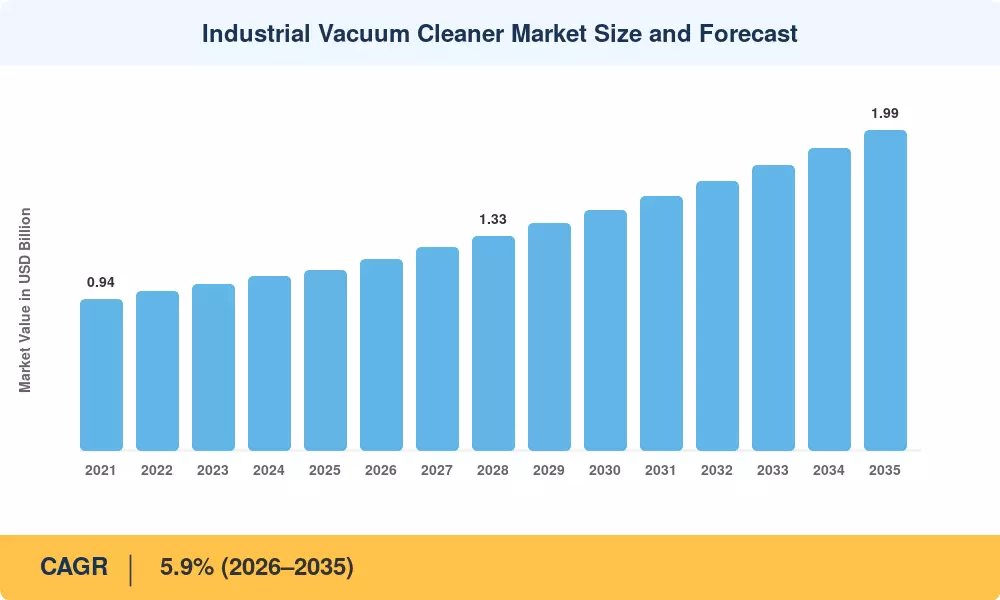

The Industrial Vacuum Cleaner Market stood at USD 1.12 billion in 2025 and is set to open the forecast window at USD 1.19 billion in 2026, climbing to USD 1.99 billion by 2035 at a 5.9% CAGR. Two forces anchor this trajectory: tightening combustible-dust enforcement under NFPA 660 in North America, and the European Union's ATEX Directive (2014/34/EU), both of which are pushing factories toward certified explosion-proof equipment on faster replacement cycles than a decade ago. Capital budgets at mid-size manufacturers are increasingly earmarked for dust-control compliance rather than treated as discretionary maintenance spend, a shift that gives this Industrial Vacuum Cleaner Market unusual resilience against broader capex pullbacks.

Three-phase, sensor-enabled systems that provide filter life and runtime to facility-management software are replacing legacy single-phase, manually emptied canister devices. Vendors are retooling supply chains to satisfy this demand without compromising margin, as Kärcher’s expenditure of about EUR 200 million in 2024 to expand Vietnam manufacturing and automate German operations indicates. Connected, IoT-enabled vacuum fleets are not a luxury anymore; they are becoming the default standard in semiconductor, pharmaceutical and food-grade facilities, where contamination audits are becoming the norm.

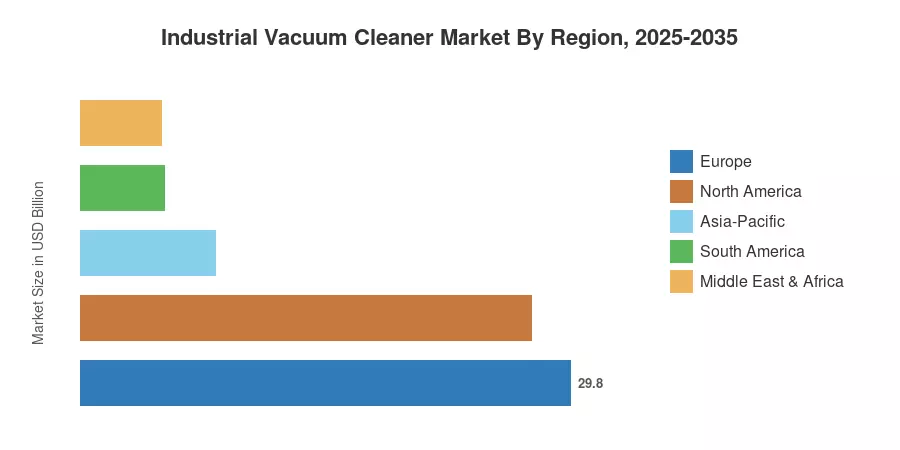

Europe accounts for the largest portion of the revenue with around 29.8% in 2025, owing to dense industrial clusters in Germany and Italy and stringent ATEX compliance standards. Asia-Pacific is projected to be the fastest developing area with an estimated CAGR of 8.2% as China and India expand contract-cleaning services and electronics production. North America is the second pillar, close behind Europe, and has been helped by OSHA combustible dust enforcement operations. In the next decade, competitive advantage in this Industrial Vacuum Cleaner Market will be driven by filtration certification and connection, and total cost of ownership, rather than motor horsepower.

Key Report Takeaways

• By Technology

- Canister systems held an estimated 44.7% share of the Industrial Vacuum Cleaner Market in 2025, the largest single product format.

- Explosion-proof, ATEX-certified units are projected to expand at an 8.5% CAGR through 2035, the fastest-growing product category.

- Electric corded platforms accounted for roughly 58.3% of 2025 revenue, though this share will compress as battery platforms scale.

• By Sector

- General manufacturing contributed an estimated 27.1% of 2025 revenue, the largest end-user vertical.

- Electronics and semiconductor facilities are forecast to grow at an 8.9% CAGR, the fastest of any end-user industry.

- Dry-only systems held close to 57.0% share in 2025, reflecting continued dominance in bulk-debris environments.

• By Geography

- Europe retained an estimated 29.8% revenue share in 2025, the largest of any region.

- Asia-Pacific is projected to post an 8.2% CAGR, the fastest regional growth rate through 2035.

- North America's market is expanding on the back of stepped-up OSHA combustible-dust citations.

Market Size and Forecast (2021–2035)

Numbers are modeled from MRFR's proprietary estimating methodology, triangulating vendor shipment data, regulatory filing patterns and industry-association survey inputs. For the historical period, numbers are reconstructed based on public business disclosures when accessible.