Infection Control Market Summary

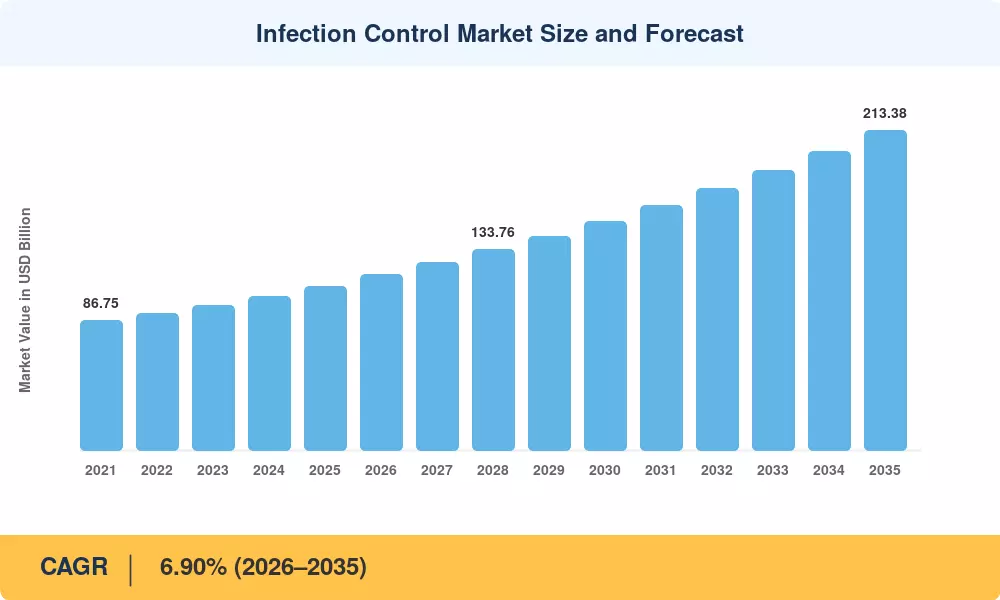

The Infection Control Market size was valued at USD 109.50 Billion in 2025, and the market is projected to grow from USD 117.06 Billion in 2026 to USD 213.38 Billion by 2035, registering a CAGR of 6.90% during the forecast period 2026–2035. Two catalysts are driving capital reallocation across healthcare systems worldwide: the U.S. Centers for Medicare & Medicaid Services (CMS) penalty structure that now withholds up to 3% of reimbursements from hospitals reporting elevated hospital-acquired infection (HAI) rates [1], and the WHO's updated global patient-safety action plan mandating that member states allocate dedicated budgets for infection prevention infrastructure by 2030 [2].

A technology transformation is reshaping the Infection Control Market as legacy high-temperature steam autoclaves and manual chemical disinfection workflows give way to low-temperature hydrogen peroxide gas plasma sterilizers and AI-powered environmental surveillance platforms. The U.S. EPA's tightened ethylene oxide (EtO) emission limits, finalized in late 2024, have accelerated adoption of alternative sterilization chemistries, with hospital capital expenditures on advanced sterilization platforms exceeding USD 4.2 Billion globally in the past two years [3].

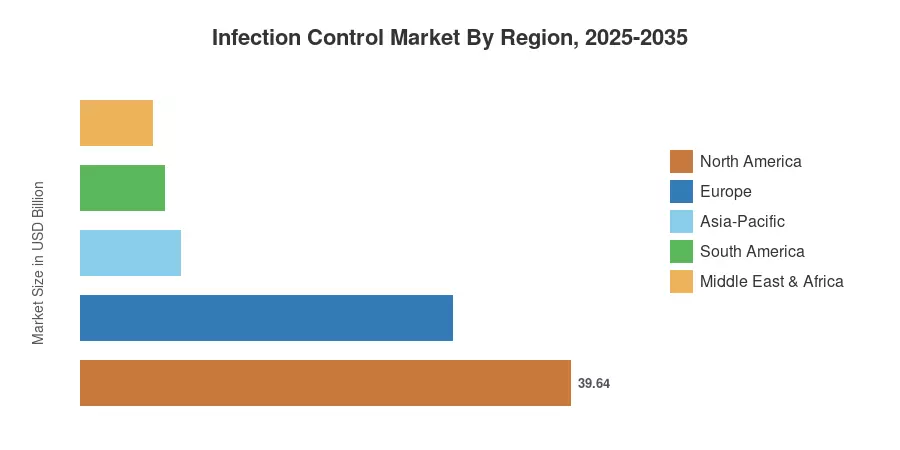

North America held approximately 36.20% of the global Infection Control Market revenue in 2025, supported by stringent regulatory enforcement and high per-bed spending on infection prevention. Asia-Pacific stands as the fastest-growing region at a projected CAGR of 7.35%, driven largely by China's ongoing hospital construction cycle and India's Ayushman Bharat digital health infrastructure expansion [4]. Europe retained the second-largest share at roughly 27.50%, anchored by the EU Medical Device Regulation's heightened reprocessing standards. The decade ahead will reward vendors who combine sterilization hardware with predictive analytics and bundled service contracts.

Key Report Takeaways

• By Products & Services

- Sterilization Products and Services accounted for approximately 39.10% of the Infection Control Market in 2025, reflecting ongoing capital investment in hydrogen peroxide and ozone-based platforms.

- Protective Barriers are projected to expand at a 7.15% CAGR through 2035, propelled by single-use gown and drape mandates across surgical settings.

• By Service Delivery Mode

- In-House Infection Control programs held roughly 49.10% of the Infection Control Market in 2025, though budget pressures are shifting volumes toward outsourced models.

- Contract Infection Control services are recording the highest projected CAGR at 7.10% through 2035 as specialist operators amortize compliance costs across multiple facilities.

• By End User

- Hospitals and Clinics commanded approximately 35.15% of the Infection Control Market in 2025, given their concentration of complex surgical procedures and ICU beds.

- Ambulatory Surgery Centers are advancing at a 7.25% CAGR through 2035, driven by outpatient volume migration and tighter ASC accreditation standards.

• By Region

- North America occupied roughly 36.20% of the Infection Control Market in 2025, anchored by CMS HAI penalty programs and robust private-payer infection benchmarking.

- Asia-Pacific is scaling at a 7.35% CAGR through 2035, fueled by Chinese provincial hospital expansion and Indian public-health modernization.

Infection Control Market Size and Forecast (2021–2035)

Market size estimates draw on primary interviews with 120+ procurement directors and infection preventionists, cross-validated against public filings from leading sterilization and disinfectant manufacturers and national health expenditure databases maintained by the WHO and OECD [5].