Infrastructure Construction Market Summary

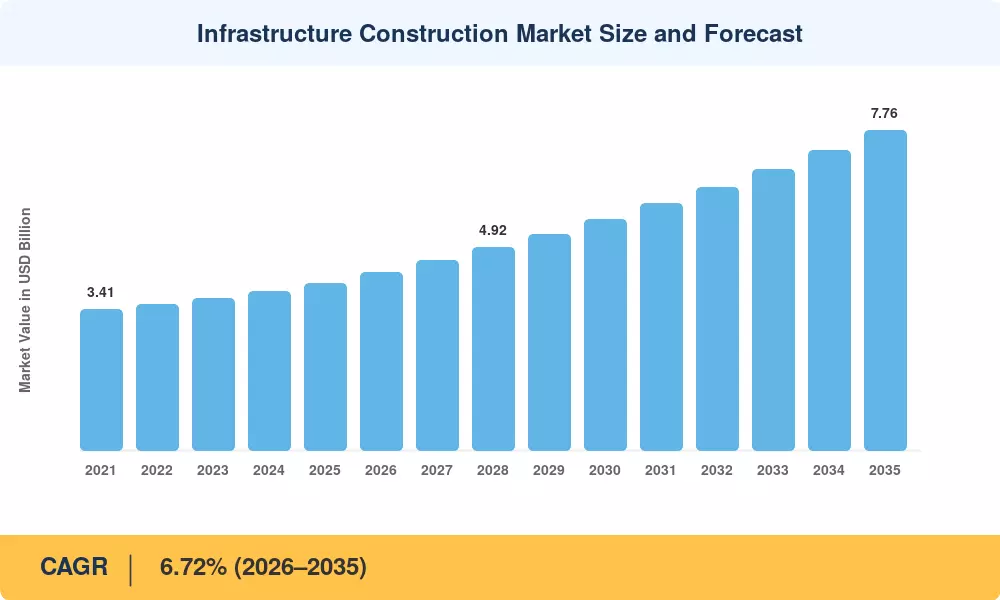

The Infrastructure Construction Market reached an estimated USD 4.05 trillion in 2025 and is projected to grow from USD 4.32 trillion in 2026 to USD 7.76 trillion by 2035, registering a CAGR of 6.72% across the forecast window. This expansion is anchored in multi-year fiscal commitments—the U.S. Infrastructure Investment and Jobs Act alone channels over USD 550 billion into roads, bridges, and broadband through 2030, while the European Union's REPowerEU plan redirects roughly EUR 300 billion toward energy and transport resilience [1][2]. These spending programs signal a structural shift from deferred maintenance to planned capital deployment.

The market for infrastructure construction is going through a generational shift in technology. Drone-based site surveys, AI-driven scheduling systems, and building information modeling are replacing analog project management and paper-based permitting. forecasts that full-scale digitization might result in yearly savings of USD 1.6 trillion for the building industry worldwide [3]. Governments now require BIM in more than 40 nations for publicly funded projects that surpass predetermined thresholds. This has accelerated adoption curves and shortened delivery timeframes for water treatment plants, rail routes, and bridges.

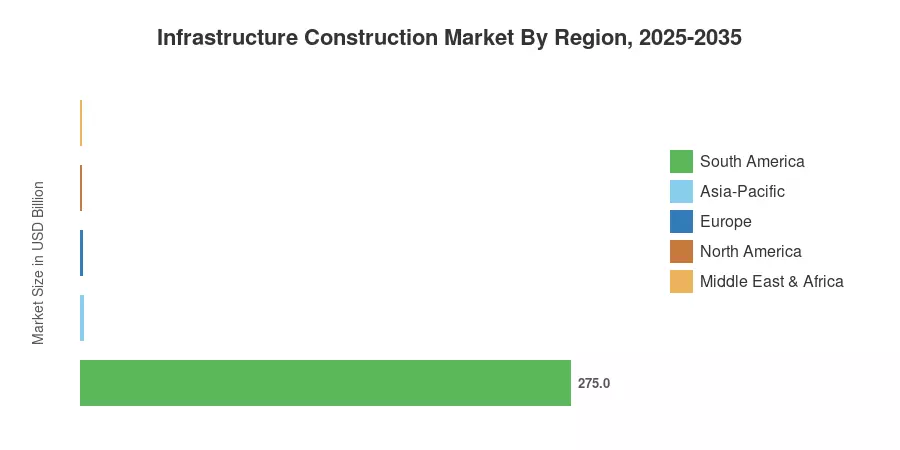

Due to India's National Infrastructure Pipeline and China's ongoing urbanization drive, the Asia-Pacific accounts for about 42.1% of the infrastructure construction market. With a 7.93% CAGR, the Middle East and Africa region is the fastest-growing geography as sovereign wealth funds in Saudi Arabia and the United Arab Emirates invest in massive projects. Thanks to improvements made to the EU's Trans-European Transport Network, Europe has the second-largest share at roughly 22.8%. Businesses that can combine digital delivery with climate-adaptive design will be rewarded in the coming ten years.

Key Report Takeaways

• By Infrastructure Segment

- Transportation held a 34.0% revenue share of the Infrastructure Construction Market in 2025, reflecting sustained rail and highway expenditure.

- Utilities are projected to expand at a 7.15% CAGR through 2035 as grid modernization accelerates globally.

- Social infrastructure—hospitals, schools, and civic buildings—accounted for roughly USD 972 billion in 2025.

• By Construction Type

- New construction captured a 68.1% share of the Infrastructure Construction Market in 2025.

- Renovation activity is forecast to record the highest segment CAGR of 6.46% over 2026–2035.

• By Investment Source

- Public funding represented 56.3% of the Infrastructure Construction Market in 2025.

- Private capital is forecast to grow at a 6.63% CAGR as availability-payment concession models gain traction.

• By Region

- Asia-Pacific accounted for a 42.1% share in 2025, led by China, India, and Japan.

- The Middle East & Africa region is predicted to expand at the fastest CAGR of 7.93% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future derives its sizing estimates through a triangulated methodology combining top-down macroeconomic modeling, bottom-up project pipeline analysis across 60+ countries, and validation against public procurement databases and annual reports of leading contractors.