Injectable Drug Delivery Devices Market Summary

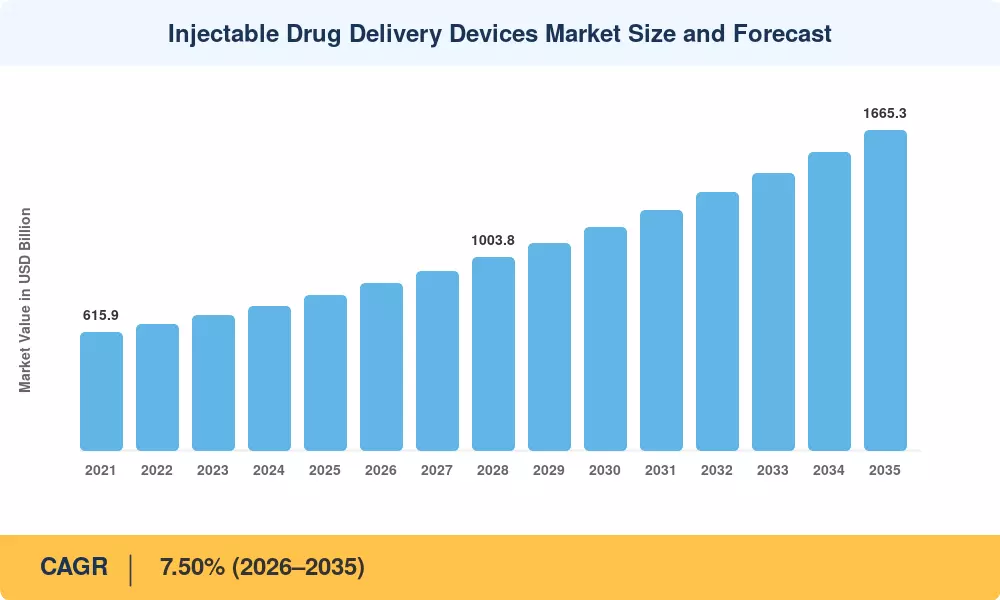

The Global Injectable Drug Delivery Devices Market size was valued at USD 808.00 Billion in 2025, and the market is projected to grow from USD 868.60 Billion in 2026 to USD 1,665.30 Billion by 2035, registering a CAGR of 7.50% during the forecast period 2026–2035. Two structural forces are powering this trajectory: an unprecedented biologics pipeline that requires parenteral delivery platforms and a decisive policy push—anchored by FDA's updated combination-product guidance (2024)—that rewards integrated device-drug co-development. Pharmaceutical sponsors now embed delivery-system selection during Phase II trials, compressing time-to-peak revenue by 12–18 months relative to legacy sequencing [3].

The market for injectable drug delivery devices is experiencing a generational technological transition. On-body wearable delivery devices, sensor-embedded smart platforms, and polymer-based containers are replacing glass barrel cartridges and manual syringes. In 2023–2024, connected injectors that can send temperature and dose-timing data to cloud dashboards attracted over USD 3.2 billion in venture and strategic investment, indicating payer willingness to tie reimbursement to actual adherence evidence [4][5].

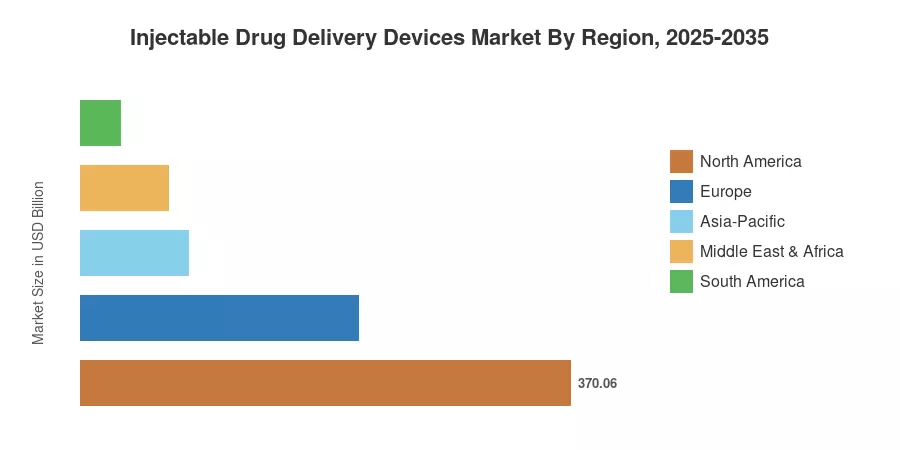

With an estimated 45.80% of 2025 revenue, North America holds the greatest share of the injectable drug delivery devices market due to the region's well-established biologics adoption and advantageous reimbursement policies. With a predicted 10.10% CAGR through 2035, Asia-Pacific is the fastest-growing market due to developing biosimilar production capacity and an increase in the prevalence of diabetes. At over USD 209.60 billion, Europe continues to be the second-largest contributor, with Germany and the UK driving demand. The market for injectable drug delivery devices is expected to grow by double digits over the next ten years in a number of important regions as the burden of chronic illnesses increases and home-administration models expand worldwide.

Key Report Takeaways

• By Device Type

- Conventional drug delivery devices—anchored by standard vials and cartridges—accounted for 38.50% of the Injectable Drug Delivery Devices Market revenue in 2024.

- Advanced drug delivery devices, including wearable on-body platforms, are projected to grow at a 12.70% CAGR through 2035, outpacing every other device category.

• By Therapeutic Application

- Diabetes held the leading therapeutic share at 33.50% of the Injectable Drug Delivery Devices Market in 2024, sustained by insulin-delivery innovation.

- Oncology is the fastest-expanding therapeutic segment, registering a 12.40% CAGR as subcutaneous monoclonal-antibody formulations gain traction.

• By Region

- North America dominated the Injectable Drug Delivery Devices Market with 45.80% revenue share in 2024.

- Asia-Pacific is forecast to post a 10.10% CAGR, the highest among all regions, driven by biosimilar uptake and government immunization programs.

- Europe contributed approximately USD 209.60 billion in 2025, supported by the EU Medical Device Regulation (MDR) transition.

Injectable Drug Delivery Devices Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from regulatory filings, manufacturer shipment data, and proprietary primary surveys covering 38 countries. Forecast projections layer demographic disease-burden modeling onto device-adoption S-curves calibrated by region and therapeutic area[6].