Insulin Syringes Market Summary

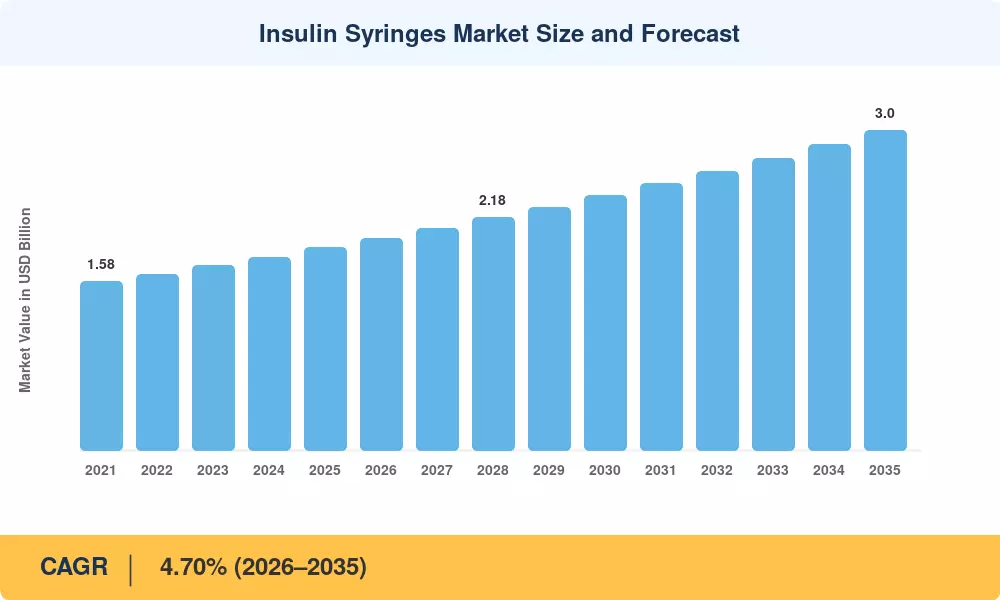

The Global Insulin Syringes Market size was valued at USD 1.90 Billion in 2025, and the market is projected to grow from USD 1.99 Billion in 2026 to USD 3.00 Billion by 2035, registering a CAGR of 4.70% during the forecast period 2026–2035. Two catalysts anchor this expansion: the International Diabetes Federation's latest atlas projects 643 million adults living with diabetes by 2030, while U.S. Medicare Part B reimbursement updates in 2024 restored favorable coverage tiers for insulin delivery syringes, stabilizing hospital procurement volumes [1][4]. These structural forces ensure that the Insulin Syringes Market retains resilient demand even as newer delivery platforms gain traction.

A technology transition is reshaping the product mix within the Insulin Syringes Market. Legacy standard-bore syringes are steadily giving way to safety-engineered and low dead-space designs that reduce needlestick injuries and conserve expensive concentrated insulins. The U.S. Occupational Safety and Health Administration's Bloodborne Pathogens Standard continues to drive safety-syringe adoption across healthcare facilities, and the 2024 EU Medical Device Regulation amendments tightened post-market surveillance requirements for sharps devices [8][9][13]. Becton Dickinson alone invested over USD 200 million in safety syringe manufacturing capacity between 2022 and 2024, signaling industry-wide commitment to this upgrade cycle [10].

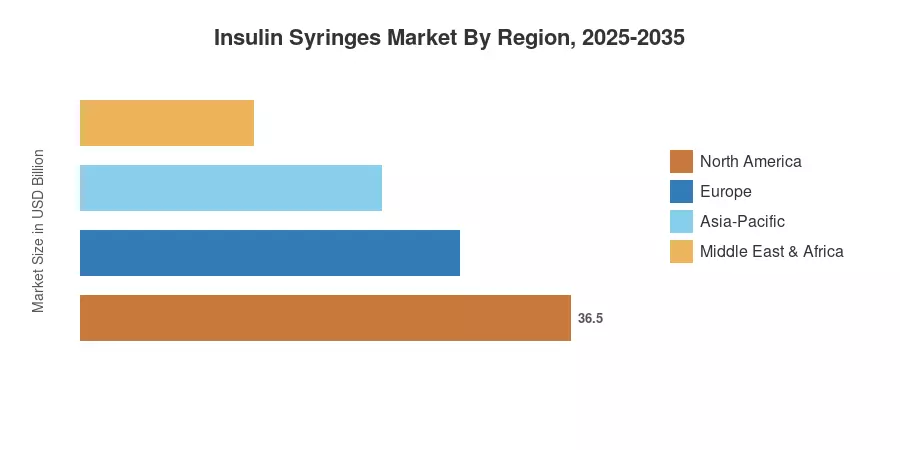

North America commands a 43.0% revenue share, supported by entrenched GPO contracts and comprehensive payer programs. Asia-Pacific is the fastest-growing region with a projected 5.55% CAGR, fueled by diabetes screening expansions in India and China. Europe holds the second-largest position at roughly 26% share, driven by NHS and statutory health insurance mandates. As biosimilar insulin launches accelerate across emerging economies, the Insulin Syringes Market is poised for broad-based geographic expansion through 2035.

Key Report Takeaways

• By Volume Capacity

- The 0.5 mL segment captured 47.3% of the Insulin Syringes Market share in 2025, reflecting its role as the default specification for standard U-100 dosing regimens

- The 1.0 mL category is projected to register a 5.50% CAGR through 2035, propelled by the growing use of concentrated U-500 insulin therapies

• By Insulin Concentration

- U-100 formulations accounted for 74.5% of the Insulin Syringes Market share in 2025, underpinned by global formulary standardization

• By Diabetes Type

- Type 1 diabetes applications exhibit the fastest CAGR at 5.50%, driven by pediatric diagnosis growth and intensive insulin protocols

• By End User

- Hospitals and clinics held 51.0% share in 2025, anchored by institutional procurement contracts and inpatient insulin management needs

- Home-care settings are rising at a 5.60% CAGR, reflecting patient preference for self-administration and telehealth-guided dosing

• By Region

- North America led with 43.0% revenue share in 2025, backed by a robust reimbursement infrastructure

- Asia-Pacific is on track for a 5.55% CAGR, driven by national diabetes control programs in India and China

Insulin Syringes Market Size and Forecast (2021–2035)

Market sizing relies on a triangulated methodology combining manufacturer revenue disclosures, import-export trade data, and insulin prescription volume proxies from national diabetes registries. Historical figures (2021–2024) draw on confirmed company filings and customs records, while forecast values (2026–2035) apply a calibrated compound annual growth rate validated against multiple independent benchmarks.

.webp?v=1782976211)