Prefilled Syringes Market Summary

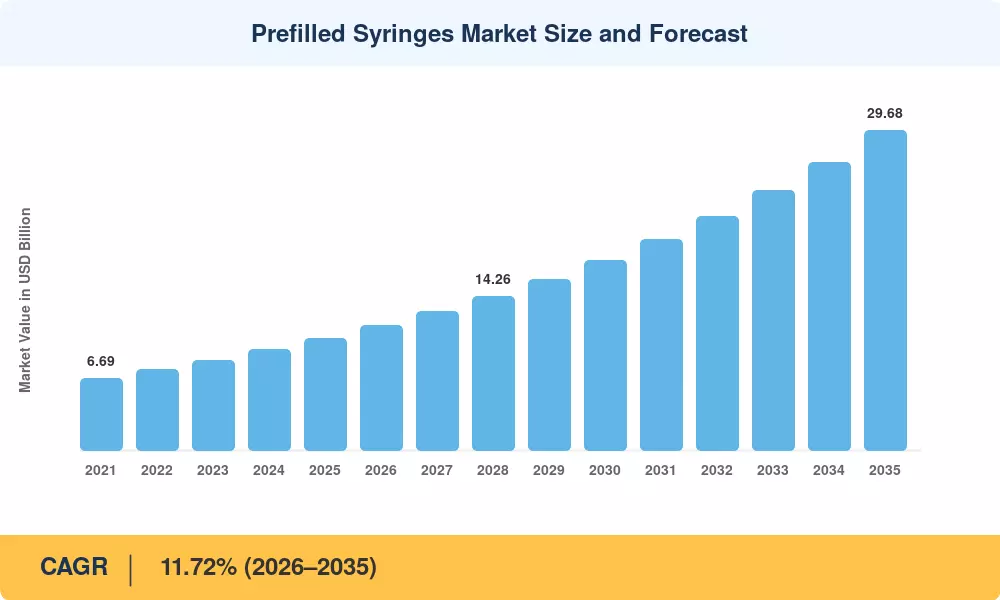

The Prefilled Syringes Market was valued at USD 10.42 billion in 2025 and is projected to reach USD 11.58 billion in 2026 before climbing to USD 29.68 billion by 2035, registering a CAGR of 11.72% during the 2026–2035 forecast window. Two catalysts are anchoring this trajectory: the global biologics pipeline — which now exceeds 8,000 active clinical-stage molecules requiring cold-chain-compatible single-dose drug delivery formats — and tightening occupational safety mandates such as the EU Sharps Directive (2010/32/EU), which compel hospitals to adopt safety-engineered needle-based drug administration systems [2][3].

A generational shift in primary packaging is underway across the pharmaceutical supply chain. Legacy vial-and-syringe workflows are giving way to ready-to-use injectable devices that reduce overfill waste by 15–20% and cut bedside preparation time from minutes to seconds. Cyclic-olefin polymer barrels are challenging decades of borosilicate glass dominance, offering break-resistance, lower extractables, and compatibility with sensitive biologics prefilled packaging requirements. Global investment in fill-finish capacity additions surpassed USD 4.8 billion in 2024 alone, with Schott, Gerresheimer, and Stevanato Group commissioning new high-speed lines across the U.S. and Southeast Asia [4][5].

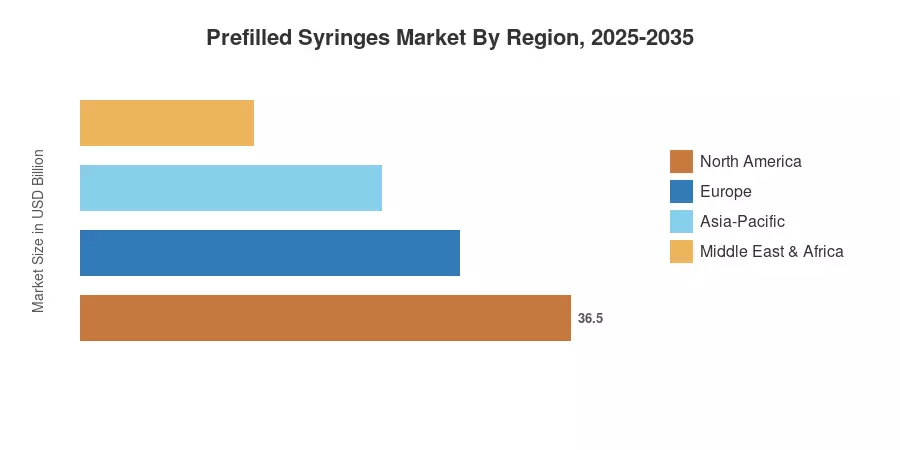

North America commands roughly 41% of the Prefilled Syringes Market, powered by Medicare Part B reimbursement reforms that favor physician-administered biologics in autoinjector pen systems. Asia-Pacific is the fastest-growing region at an estimated 13.15% CAGR, fueled by India's production-linked incentive scheme for medical devices and China's volume-based procurement expansion. Europe holds the second-largest share, anchored by Germany's robust biosimilar adoption and the EU's Pharmaceutical Strategy for Europe. The decade ahead will see these dynamics intensify as payers globally push treatment settings from hospitals toward home healthcare

Key Report Takeaways

• By Material

- Glass dominated the Prefilled Syringes Market with approximately 73% of 2025 revenue, supported by decades of regulatory precedent in borosilicate barrel manufacturing

- Polymer is advancing at a CAGR of 11.84% through 2035, driven by biologics prefilled packaging requirements that demand low-protein-adsorption surfaces

• By Application

- Diabetes accounted for roughly 37% of prefilled syringe shipments in 2025, reflecting the global insulin pen installed base exceeding 300 million units

- Vaccines represent the fastest-expanding application at a 14.58% CAGR, propelled by pandemic-preparedness stockpiling and WHO prequalification of single-dose drug delivery formats

• By End User

- Hospitals & clinics held a 44.8% share of the Prefilled Syringes Market in 2025, driven by needlestick-injury compliance mandates

- Home healthcare is growing at a 12.74% CAGR as autoinjector pen systems simplify self-administration of biologics

• By Region

- North America contributed approximately USD 4.27 billion in 2025 Prefilled Syringes Market value

- Asia-Pacific is projected to post a 13.15% CAGR through 2035, led by China and India

Prefilled Syringes Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling from over 45 fill-finish contract manufacturers and top-down validation against pharmaceutical industry secondary shipment data. Historical figures (2021–2024) are reconciled with company filings, while the 2026–2035 forecast applies a calibrated compound growth model anchored to biologics pipeline progression and regional reimbursement trends.