Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

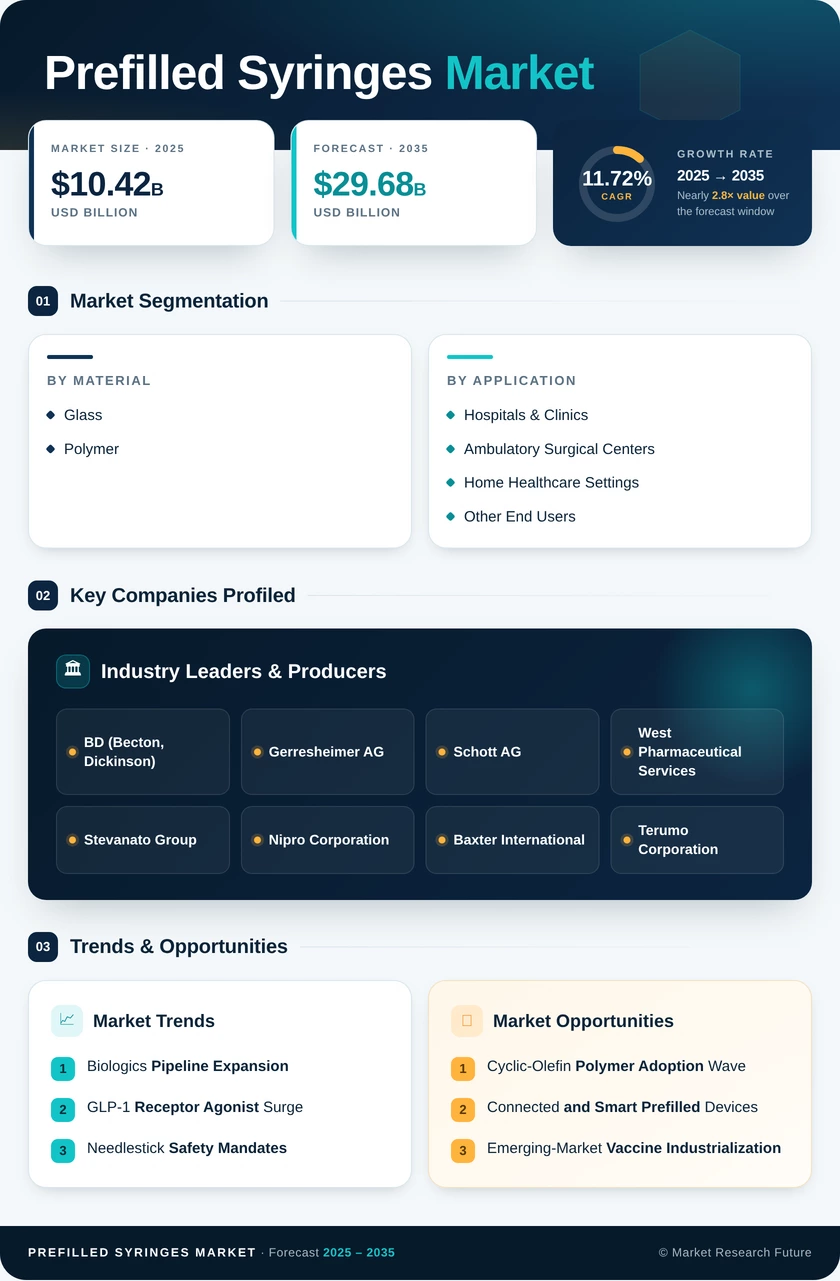

| By Material | Glass, Polymer | Glass | Polymer |

| By Application | Diabetes, Rheumatoid Arthritis, Vaccines, Anticoagulants, Other Applications | Diabetes | Vaccines |

| By End User | Hospitals & Clinics, Ambulatory Surgical Centers, Home Prefilled Syringes Market Settings, Other End Users | Hospitals & Clinics | Home Prefilled Syringes Market Settings |

| By Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Material

| Sub-Segment | Key Trend |

| Glass | Continued dominance driven by regulatory familiarity and established pharmacopeial standards for Type I borosilicate |

| Polymer | Accelerating adoption for biologic drugs requiring silicone-oil-free, break-resistant primary packaging |

Glass barrels remain the default choice for most injectable drug products due to their extensive regulatory track record. Polymer (COP/COC) is gaining rapid share as pharmaceutical companies prioritize biologics-compatible, lightweight, and break-resistant alternatives for sensitive formulations.

By Application

| Sub-Segment | Key Trend |

| Diabetes | Largest volume driver anchored by global insulin pen and GLP-1 autoinjector demand |

| Rheumatoid Arthritis | Steady growth from TNF-inhibitor and JAK-inhibitor self-injection programs |

| Vaccines | Fastest growth driven by pandemic preparedness, WHO prequalification, and emerging-market immunization expansion |

| Anticoagulants | Stable demand from low-molecular-weight heparin home-administration protocols |

| Other Applications | Expanding with oncology supportive care, fertility hormones, and migraine biologics |

Diabetes and vaccines together account for over half of global prefilled syringe unit volumes. The GLP-1 agonist category is a major near-term catalyst, while vaccine preparedness investments ensure sustained long-term expansion.

By End User

| Sub-Segment | Key Trend |

| Hospitals & Clinics | Dominant channel driven by needlestick safety mandates and in-facility biologic administration |

| Ambulatory Surgical Centers | Growing with the outpatient procedure shift and same-day discharge protocols |

| Home Prefilled Syringes Market Settings | Fastest-growing segment as payers incentivize self-injection to reduce healthcare facility costs |

| Other End Users | Includes long-term care facilities, retail pharmacies, and specialty infusion centers |

The site-of-care shift from hospitals to home settings is the defining structural trend in end-user dynamics. Autoinjector platforms designed for patient self-administration are the primary beneficiary of this transition.