Life Sciences BPO Market Summary

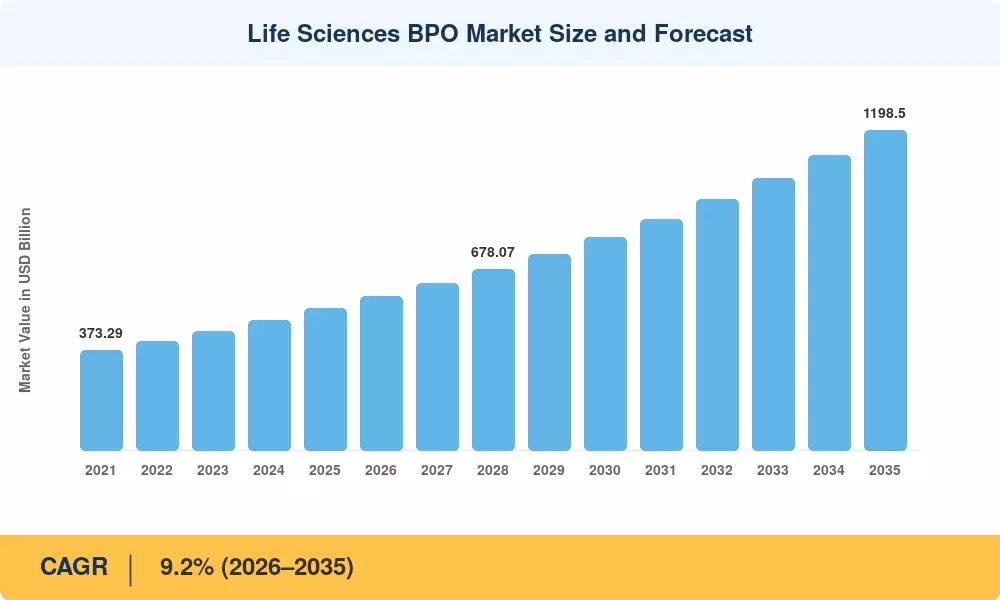

The Global Life Sciences BPO Market size was valued at USD 531.2 Billion in 2025, and the market is projected to grow from USD 581.4 Billion in 2026 to USD 1,198.5 Billion by 2035, registering a CAGR of 9.45% during the forecast period 2026–2035. Two structural forces are accelerating this trajectory: the Inflation Reduction Act's drug-pricing provisions, which compel pharmaceutical companies to protect margins through outsourced operations, and the FDA's 2024 guidance on decentralized clinical trials, which created fresh demand for clinical data management outsourcing and remote monitoring infrastructure[2]. These catalysts have shifted outsourcing from a cost-reduction tactic into a core operating model for drug development support services.

A technological transformation is reshaping how bioscience back-office operations function. Legacy paper-based regulatory submissions and manual pharmacovigilance workflows are giving way to AI-powered platforms that automate adverse-event detection, regulatory affairs services, and real-world evidence generation. Accenture estimates that life sciences companies deploying intelligent automation across outsourced functions can reduce cycle times by 30–40%, unlocking roughly USD 18 billion in annual efficiency gains industry-wide [3]. Contract development and manufacturing organizations are simultaneously investing in modular biologics capacity, with over USD 12 billion committed to new fill-finish and cell-therapy suites since 2023.

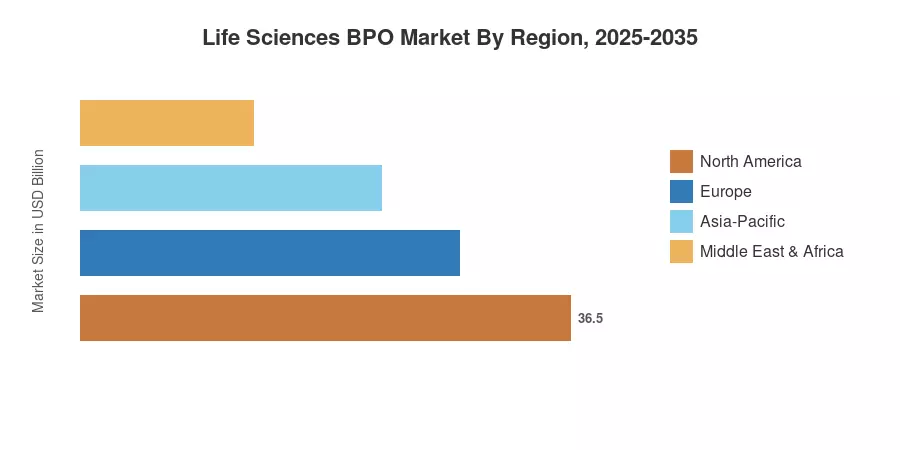

North America commands approximately 44.8% of the Life Sciences BPO Market, anchored by the US FDA's regulatory complexity and the concentration of top-20 pharma headquarters. Asia-Pacific stands as the fastest-growing region at a 9.2% CAGR, powered by India's expanding CDMO ecosystem and China-plus-one supply-chain diversification. Europe holds the second-largest share at roughly 26.3%, driven by EMA harmonization efforts and the UK's post-Brexit regulatory autonomy The decade ahead will reward companies that blend pharmaceutical outsourcing services with advanced analytics and flexible capacity models.

Key Report Takeaways

• By Service Type

- CRO services captured a leading 46.9% share of the Life Sciences BPO Market in 2024, reflecting sustained demand for externalized clinical development and clinical data management outsourcing capabilities

- CDMO/CMO services are forecast to expand at a 12.2% CAGR through 2035, the fastest service category, as biologics manufacturing and cell-gene therapy capacity constraints push drug development support services toward specialized partners

- Regulatory BPO and pharmacovigilance BPO together represent a combined opportunity exceeding USD 68 billion by 2035, fueled by tightening global regulatory affairs services requirements

• By End User

- Pharmaceutical companies accounted for 61.3% of Life Sciences BPO Market revenue in 2024, leveraging full-service partnerships to manage complex R&D pipelines

- Biotechnology firms are projected to grow at a 9.1% CAGR to 2035, driven by venture-funded clinical programs requiring scalable pharmaceutical outsourcing services

• By Region

- North America generated 44.8% of global revenue in 2024, with the US alone contributing over USD 198 billion in outsourced life sciences spending

- Asia-Pacific is set to grow at a 9.2% CAGR to 2035 as India, Southeast Asia, and Japan expand bioscience back-office operations and CDMO capacity

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling across six service verticals, validated against top-down macroeconomic indicators including global pharmaceutical R&D expenditure, biologics pipeline growth, and regulatory submission volumes. Historical figures (2021–2024) draw on company filings, customs data, and industry association reports; forecast values (2026–2035) apply segment-level growth assumptions calibrated to pipeline activity, capacity expansion announcements, and policy trajectories[5].