Liquid Handling System Market Summary

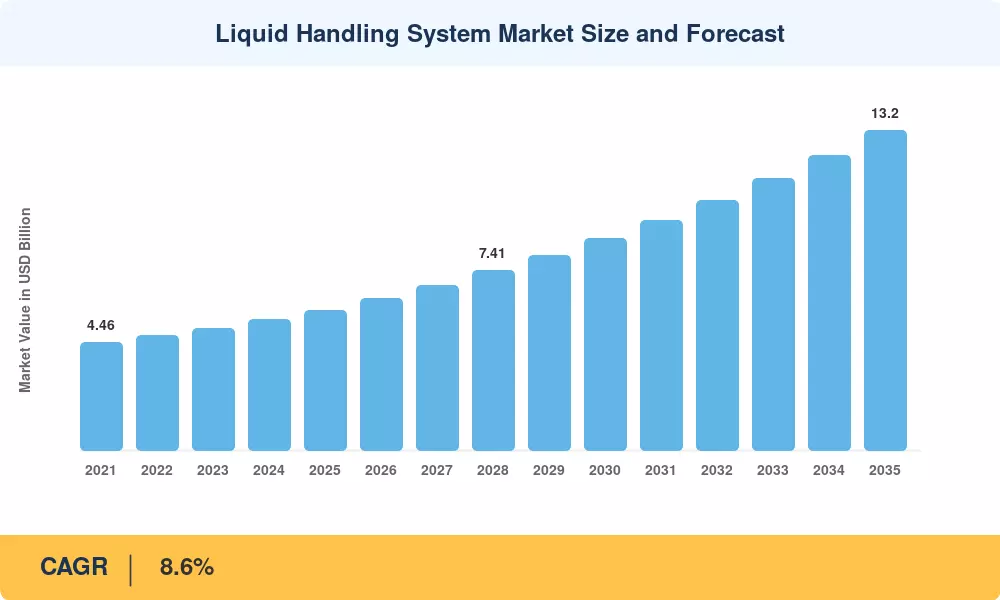

The Liquid Handling System Market reached USD 5.79 billion in 2025 and is projected to grow from USD 6.28 billion in 2026 to USD 13.20 billion by 2035, registering a CAGR of 8.6% during the forecast period. This expansion is fueled by pharmaceutical companies investing heavily in automation to meet FDA 21 CFR Part 11 compliance requirements and the ongoing scale-up of cell and gene therapy manufacturing pipelines, which demand traceable, error-free liquid transfers at volumes that manual methods cannot sustain [1][2].

Globally, a change in technology is redefining laboratories. Long the foundation of academic and clinical laboratories, legacy manual pipetting operations are being replaced by integrated robotic platforms that can process thousands of samples daily with sub-microliter accuracy. For fiscal year 2024, the US National Institutes of Health allotted more than USD 47.3 billion in research funding, much of which goes into upgrading equipment at federally funded research facilities [3]. This shift is being accelerated by acoustic dispensing and microfluidic nano-dispensing technologies, which eliminate tip-contact contamination hazards.

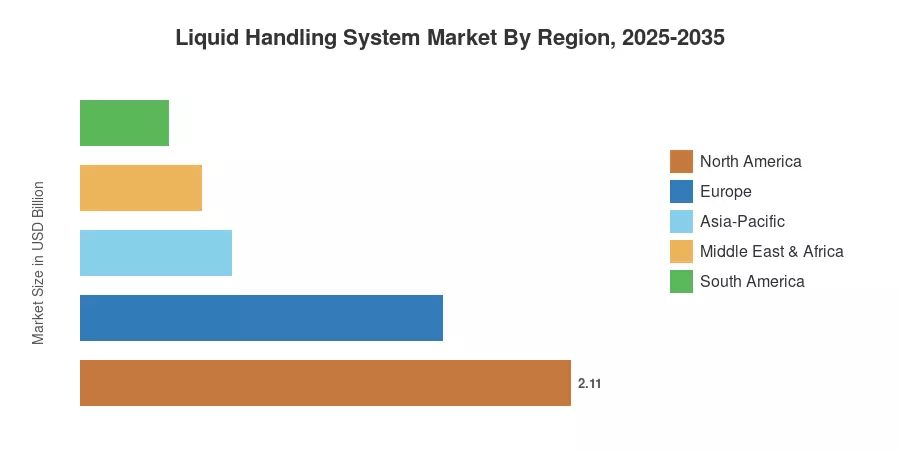

Due to a high concentration of pharmaceutical R&D facilities and contract research firms, North America accounted for the highest portion of the Liquid Handling System Market in 2025 (36.5%). With a predicted CAGR of 11.25%, Asia-Pacific emerged as the fastest-growing area, driven by government-backed biotech park developments in South Korea, China, and India. With almost 27% of the market, Europe held the second-largest position due to the EU's Horizon Europe research investment framework and Germany's pharmaceutical manufacturing corridor [4]. As AI-integrated platforms and modular funding models remove obstacles for mid-tier laboratories worldwide, the competitive landscape will change over the next ten years.

Key Report Takeaways

• By System Type

- Semi-automated platforms accounted for 30.6% of the Liquid Handling System Market in 2025, reflecting the transitional phase many laboratories are navigating between manual and fully integrated workflows.

- Fully automated systems are poised to register the fastest growth at an 11.55% CAGR through 2035, as throughput demands outpace what semi-automated configurations can reliably deliver.

• By Product Category

- Automated workstations led the Liquid Handling System Market with 26.9% revenue share in 2025, serving as the anchor platform for high-volume drug screening operations.

- Acoustic ejectors are set to expand at a 10.95% CAGR to 2035, driven by rising adoption in genomics and miniaturized assay development.

• By Application

- Drug discovery and high-throughput screening commanded 37.8% of the Liquid Handling System Market in 2025, a segment defined by the pharmaceutical industry's relentless push toward larger compound libraries.

- Cell and gene therapy manufacturing is growing at a 12.75% CAGR, the fastest among all application segments, as approved therapies move from clinical-stage to commercial-scale production.

• By End User

- Pharmaceutical and biotechnology companies represented 40.7% of revenue in the Liquid Handling System Market during 2025.

- Contract research and manufacturing organizations are expanding fastest at an 11.95% CAGR, reflecting the broader outsourcing trend in drug development.

• By Geography

- North America dominated the Liquid Handling System Market with 36.5% share in 2025.

- Asia-Pacific is advancing at an 11.25% CAGR to 2035, the highest among all regions.

Market Size and Forecast (2021–2035)

Market Research Future constructed this forecast using a triangulated approach combining bottom-up revenue analysis of key vendors, top-down validation against pharmaceutical R&D expenditure benchmarks, and primary interviews with laboratory procurement officers across 14 countries. Historical figures (2021–2024) reflect actual industry performance; the base year (2025) incorporates preliminary full-year data; forecast values (2026–2035) apply a calibrated compound annual growth rate derived from demand modeling across all end-use verticals.