Lithium Sulfur Battery Market Summary

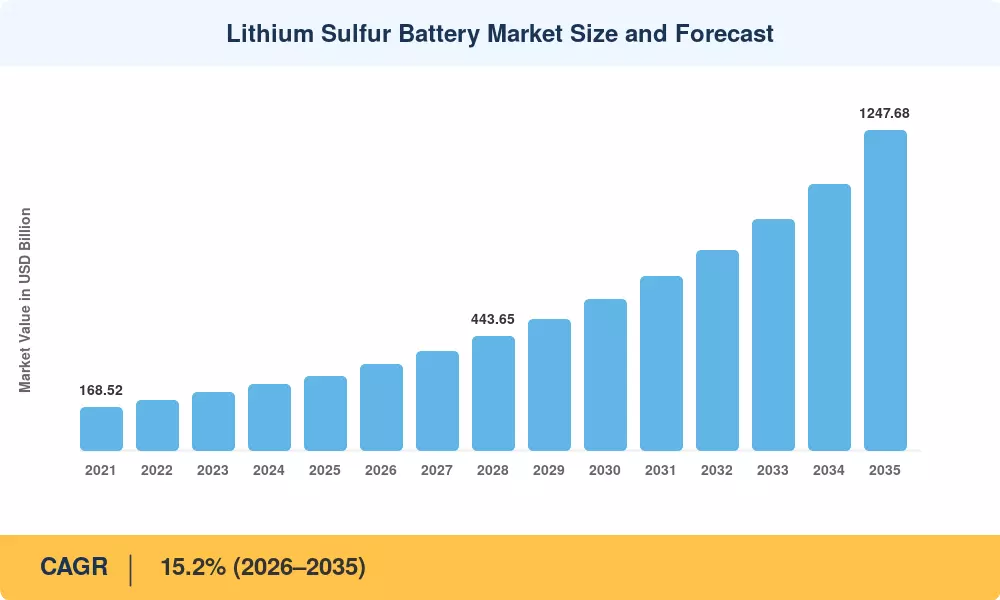

The Lithium Sulfur Battery Market reached an estimated USD 290.24 billion in 2025 and is projected to grow from USD 334.28 billion in 2026 to USD 1,247.68 billion by 2035, registering a CAGR of 15.2% during the forecast period (2026–2035). This expansion is anchored by aggressive government electrification mandates and the U.S. Department of Energy's USD 3.1 billion investment in next-generation battery research under the Bipartisan Infrastructure Law [2]. Li-S battery high energy density capabilities — exceeding 400 Wh/kg in prototype cells — position this chemistry as a disruptive alternative to conventional lithium-ion systems across weight-sensitive applications.

A fundamental technology transformation is underway in the Lithium Sulfur Battery Market as legacy lithium-ion architectures face performance ceilings in aerospace, defense, and long-range electric aviation. Solid state lithium sulfur cell development has accelerated, with multiple pilot lines commissioned globally since 2023. The European Battery Alliance committed over EUR 6 billion to advanced cell chemistries, including Li-S platforms, signaling policy-level confidence in this trajectory [3]. Lithium anode protection breakthroughs and Li-S battery electrolyte optimization efforts have reduced capacity fade rates by 30–40% in recent laboratory demonstrations.

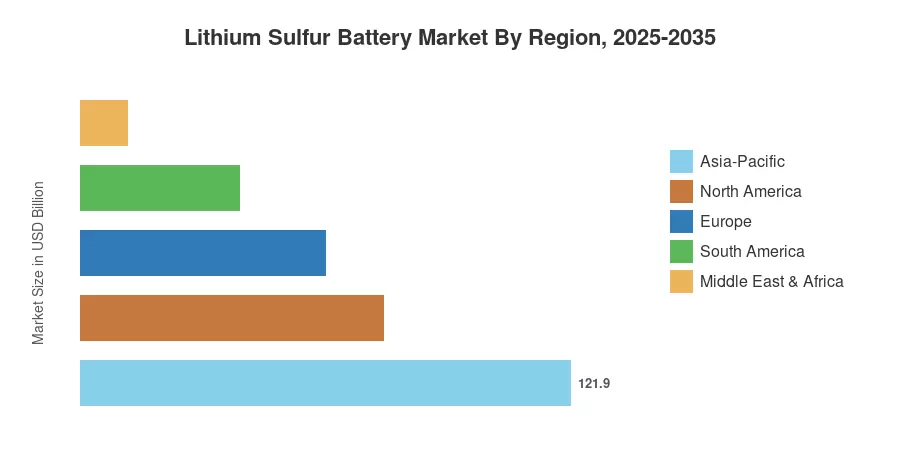

Asia-Pacific commands the dominant share of the Lithium Sulfur Battery Market at approximately 42% of global revenue, driven by China's sulfur production infrastructure and aggressive EV battery industrialization programs. The region also stands as the fastest-growing geography, expanding at a CAGR of 16.8%. North America holds the second-largest share at roughly 26%, propelled by defense procurement cycles and lithium sulfur battery aerospace drone integration programs. Europe trails closely, with sustainability-linked procurement mandates accelerating adoption across commercial aviation and grid storage verticals

Key Report Takeaways

• By End-User

- The Aerospace segment accounts for approximately 32% of the Lithium Sulfur Battery Market, reflecting demand for Li-S battery high energy density in UAV and satellite applications

- The Automotive end-user segment is expanding at the fastest CAGR of 17.4%, fueled by next-generation EV range extension strategies

- The Electronics segment generated approximately USD 49.34 billion in 2025, supported by portable device miniaturization trends

• By Technology Focus

- Polysulfide shuttle problem Li-S mitigation technologies represent the largest R&D investment category, with over USD 1.2 billion allocated globally in 2024

- Solid-state lithium sulfur cell architectures captured a 19% share of new pilot-line capacity commissioned during 2023–2025

• By Region

- Asia-Pacific leads the Lithium Sulfur Battery Market with a 42% revenue share

- South America is projected to grow at a CAGR of 13.6%, the highest among emerging regions, driven by lithium extraction proximity advantages

Market Size and Forecast (2021–2035)

The market size estimates below combine primary interviews with battery manufacturers, sulfur suppliers, and end-use procurement teams with secondary data from government energy statistics, trade databases, and patent filings. Historical figures (2021–2024) reflect actual shipments and disclosed revenues; forecast values (2026–2035) apply MRFR's calibrated CAGR model.