Livestock Monitoring Market Summary

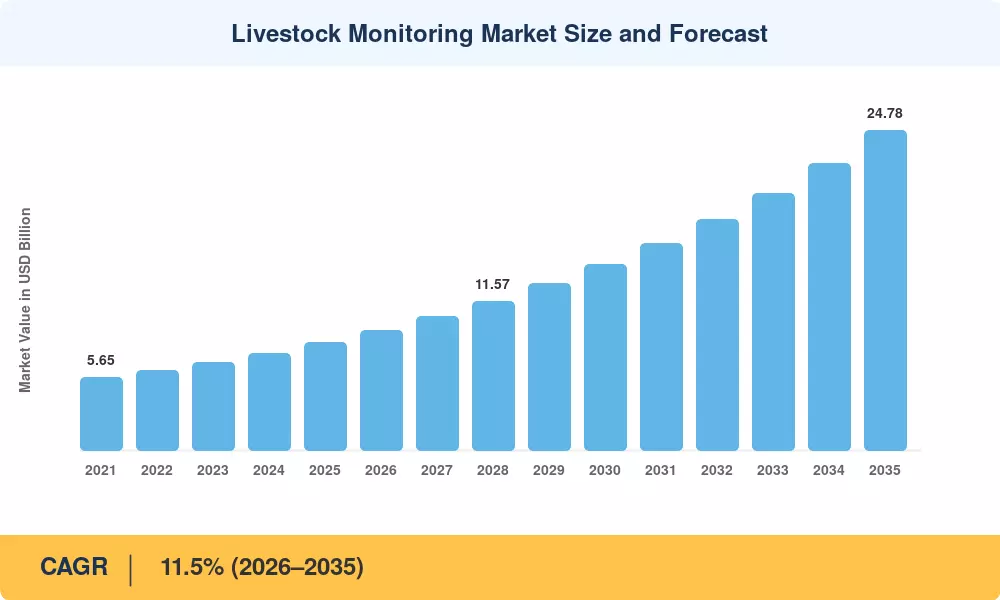

The Livestock Monitoring Market size was valued at USD 8.35 Billion in 2025, and the market is projected to grow from USD 9.31 Billion in 2026 to USD 24.78 Billion by 2035, registering a CAGR of 11.5% during the forecast period 2026–2035. Expanding global herd sizes — India, Brazil, and China alone account for roughly two-thirds of the world's cattle inventory — have made manual observation impractical at scale [1]. Governments and multilateral agencies are channeling funds into digital agriculture programs, and the European Union's Horizon Europe framework allocated over EUR 300 million toward smart farming and animal welfare technologies between 2021 and 2024 [2].

A technological shift is redefining how producers manage herds. Legacy visual-inspection routines and paper-based record-keeping are giving way to IoT-enabled sensor networks, AI-driven health analytics, and cloud-based herd management platforms. In April 2023, Advantech Co. Ltd. launched an AI-powered system combining infrared thermal imaging with machine learning to detect early signs of bovine illness [3]. Global investment in agri-tech exceeded USD 10 billion in 2023 alone, with livestock intelligence platforms attracting a rising share of that capital [4].

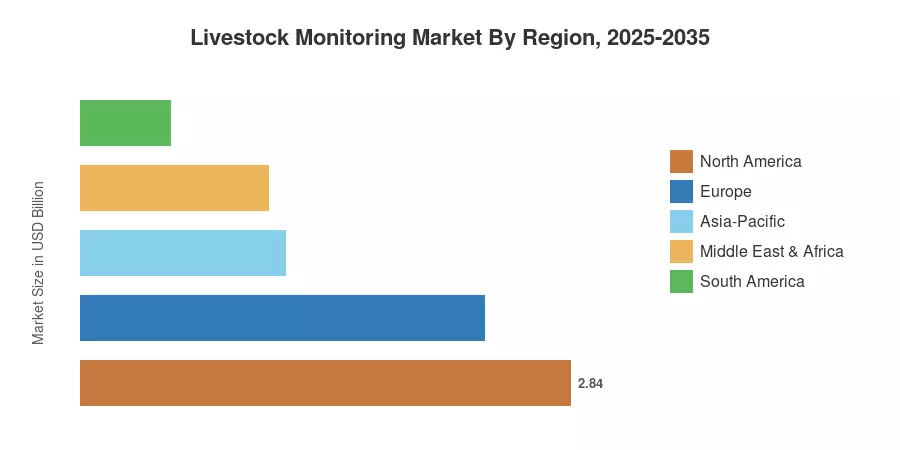

North America commands the largest share of the Livestock Monitoring Market at approximately 34%, driven by high dairy automation rates and favorable USDA data-connectivity programs. Asia-Pacific is the fastest-growing region, expanding at an estimated 14.2% CAGR as large-scale commercial farming accelerates across India and China. Europe holds roughly 28% of global revenue, anchored by stringent EU animal welfare mandates. As emerging economies industrialize their protein supply chains, the Livestock Monitoring Market is positioned for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Component

- Hardware (sensors, wearables, on-farm readers) holds the largest revenue share at approximately 46% of the Livestock Monitoring Market, reflecting heavy capital deployment in connected devices.

- Software platforms are expanding at the fastest CAGR of 13.8%, fueled by demand for cloud analytics and herd-level dashboards.

- Services — including installation, data integration, and consulting — generated roughly USD 1.59 billion in 2025.

• By Animal Type

- Cattle monitoring dominates the Livestock Monitoring Market, accounting for about 52% of total revenue.

- Poultry monitoring is the second-largest segment, growing at a CAGR of 12.1%.

• By Region

- North America leads the Livestock Monitoring Market with an estimated 34% share.

- Asia-Pacific is the fastest-growing region, registering a CAGR of approximately 14.2%.

- Europe contributes about 28% of global market revenue.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining primary interviews with farm-technology OEMs, secondary data from FAO and USDA livestock censuses, and proprietary bottom-up revenue modeling across 45 countries. All historical figures reflect actual industry performance; forecast values apply the calibrated 11.5% CAGR with adjustments for regional adoption velocity.