Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Group | Group I, Group II, Group III, Group IV (PAO), Group V | Group I (45.5% share, 2025) | Group III (3.25% CAGR) |

| By Base Stock | Mineral-Oil, Synthetic, Semi-Synthetic, Bio-Based | Mineral-Oil (71.0% share, 2025) | Bio-Based (3.48% CAGR) |

| By Product Type | Engine Oils, Transmission & Gear Oils, Hydraulic Fluids, Metalworking Fluids, Other | Engine Oils (55.2% share, 2025) | Other / EV Thermal Fluids (2.86% CAGR) |

| By End-User Industry | Automotive, Power Generation, Heavy Equipment, Other Industries | Automotive (60.4% share, 2025) | Power Generation (3.12% CAGR) |

| By Geography | Asia-Pacific, North America, Europe, South America, Middle East & Africa | Asia-Pacific (48.7% share, 2025) | Middle East & Africa (3.45% CAGR) |

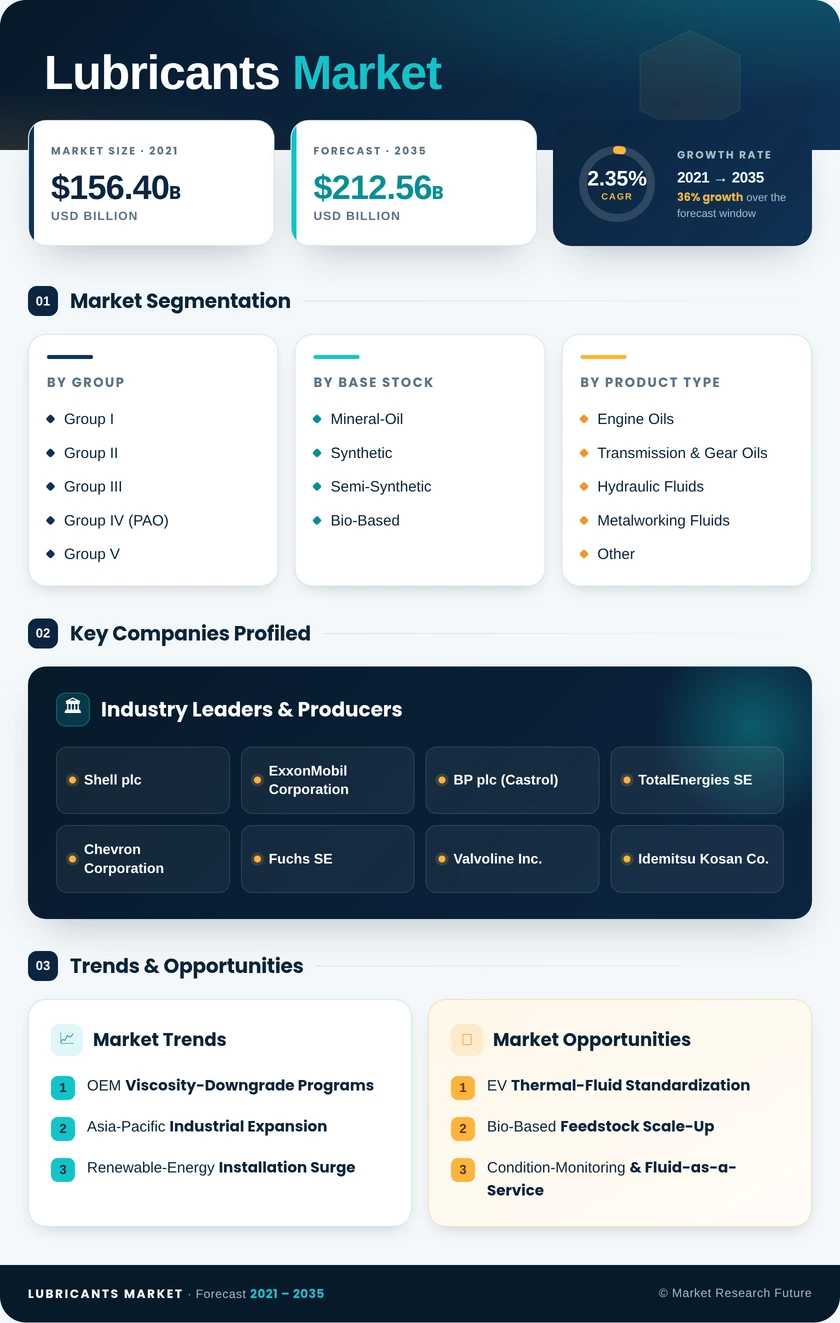

Market Segmentation Overview

By Group

| Sub-Segment | Key Trend |

| Group I | Capacity rationalization in Europe; sustained demand in South Asia and Africa |

| Group II | Expanding as the default all-purpose base stock for automotive and industrial grades |

| Group III | Rapid capacity additions in Middle East and South Korea narrowing cost gap with Group II |

| Group IV (PAO) | Premium positioning in extreme-temperature and aviation applications |

| Group V | Specialty esters and polyglycols growing in EV and refrigeration niches |

Group classification defines the performance ceiling and price floor of finished lubricant products. Group I remains dominant by volume due to its entrenched position in price-sensitive emerging markets, while Group III represents the industry's structural growth vector as new refinery investments bring synthetic-quality base stocks to near-mineral-oil cost levels.

By Base Stock

| Sub-Segment | Key Trend |

| Mineral-Oil | Still the volume leader; gradual share erosion as OEM specs tighten |

| Synthetic | Growing on the back of extended-drain and fuel-economy requirements |

| Semi-Synthetic | Serving as a transitional grade bridging mineral and full-synthetic tiers |

| Bio-Based | Niche but fastest-growing, propelled by EU regulatory mandates and ESG procurement |

Base-stock selection increasingly reflects regulatory and sustainability pressures rather than pure cost optimization. Bio-based formulations, while small in absolute volume, are attracting disproportionate R&D investment as formulators position for anticipated green-procurement mandates beyond Europe.

By Product Type

| Sub-Segment | Key Trend |

| Engine Oils | Viscosity downgrades driving reformulation; largest revenue pool |

| Transmission & Gear Oils | Wind-turbine and heavy-duty truck demand sustaining growth |

| Hydraulic Fluids | Lubricants Market and mining expansion in Asia-Pacific and Latin America |

| Metalworking Fluids | Precision machining for EV battery-tray and motor-housing components |

| Other (incl. EV Thermal Fluids) | Fastest-growing sub-segment; nascent but high-margin category |

Product-type dynamics reflect the broader energy transition. Engine oils face long-term structural headwinds from BEV adoption but remain the core revenue generator for the foreseeable planning horizon, while specialty categories—particularly EV thermal fluids—offer formulators a path to higher margins and deeper OEM integration.

By End-User Industry

| Sub-Segment | Key Trend |

| Automotive | Largest segment; transitioning from ICE-centric to mixed-powertrain servicing |

| Power Generation | Wind and gas-turbine expansion driving specialty fluid demand |

| Heavy Equipment | Mining and construction booms in emerging markets sustaining hydraulic-fluid volumes |

| Other Industries | Marine, rail, food-grade, and aerospace niches with specialized formulation needs |

End-user dynamics are shifting as electrification and renewable-energy deployment create new demand pools. The automotive segment's internal composition is changing rapidly—hybrid and electric vehicles require different fluid portfolios than traditional ICE platforms—while power generation emerges as the highest-growth industrial vertical on the strength of global wind-energy commitments.