Luxury Furniture Market Summary

The Luxury Furniture Market stood at USD 34.30 Billion in 2025 and is projected to reach USD 36.32 Billion in 2026, climbing to USD 60.83 Billion by 2035 at a 5.90% CAGR across the forecast period. Sustained growth in ultra-high-net-worth household formation feeds directly into premium residential and hospitality procurement budgets. Post-pandemic lifestyle recalibrations have shifted consumer spending toward experiential living spaces, making the home a primary expression of personal identity and status.

The way luxury goods are created, marketed, and used is changing due to a technological revolution. Immersion omnichannel tactics that combine augmented reality room visualization with appointment-only galleries are replacing traditional showroom-only shopping. Between 2023 and 2025, Roche Bobois and Restoration Hardware both committed more than USD 50 million to digital customer-journey platforms [2]. In the meantime, material innovation—such as bio-based leathers, repurposed metals, and engineered hardwoods—allows companies to comply with the EU Ecodesign Directive's increasingly stringent requirements without compromising the craftsmanship tales that fetch higher prices [3].

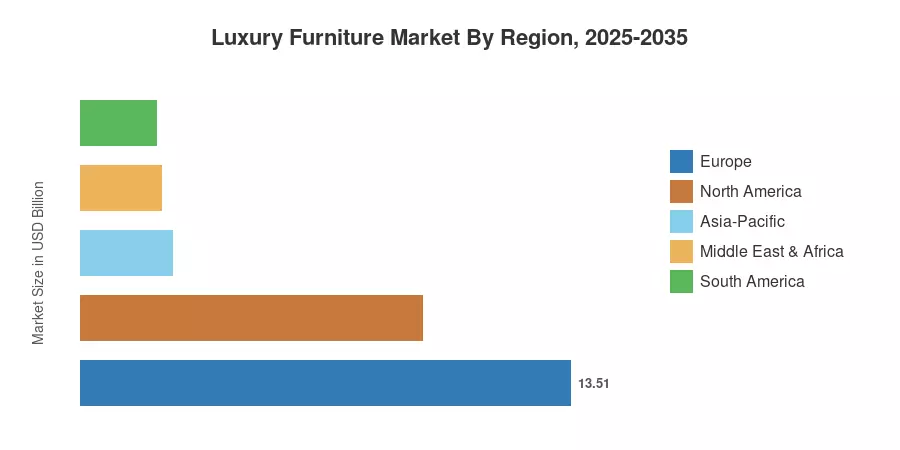

With 39.4% of worldwide revenue in 2025, Europe continues to dominate the luxury furniture market, led by legacy houses from Scandinavia and Italy. With a predicted 7.40% CAGR, Asia-Pacific is the fastest-growing region thanks to wealth growth in China, India, and the ASEAN hospitality corridors. The second-largest region, North America, maintains demand through partnerships with designer brands and a thriving luxury home market. The combination of artisan skill and smart-home capabilities will define competitive difference across all price points over the course of the next ten years.

Key Report Takeaways

• By Application

- Luxury Home Furniture captured 63.2% of the Luxury Furniture Market in 2025, driven by premium residential renovation cycles and rising interior-design spend.

- Luxury Hospitality Furniture is expected to expand at a 6.40% CAGR through 2035 as branded-hotel pipeline openings accelerate in Asia and the Middle East.

• By Material

- Wood accounted for 49.1% of the Luxury Furniture Market share in 2025, reflecting enduring consumer preference for solid-hardwood and engineered timber pieces.

- Glass-based luxury furnishings are forecast to register a 6.80% CAGR from 2026 to 2035, supported by contemporary minimalist design trends.

• By Distribution Channel

- B2C/Retail channels held 71.8% of the Luxury Furniture Market value in 2025 through a combination of flagship boutiques and department-store concessions.

- Online retail is advancing at a 7.00% CAGR through 2035 as AR-enabled platforms reduce purchase hesitation for high-ticket items.

• By Region

- Europe commanded 39.4% of the Luxury Furniture Market in 2025, led by Italy, Germany, and France.

- Asia-Pacific is poised to climb at a 7.40% CAGR through 2035, with China and India as primary growth engines.

Luxury Furniture Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing framework triangulates top-down macroeconomic indicators—HNWI population growth, luxury housing starts, hospitality CapEx—with bottom-up company revenue analysis across 45+ publicly listed and privately held furniture manufacturers. Historical figures reflect verified trade data; forecast projections apply a calibrated compound annual growth rate validated against independent third-party benchmarks [4].