Furniture Market Summary

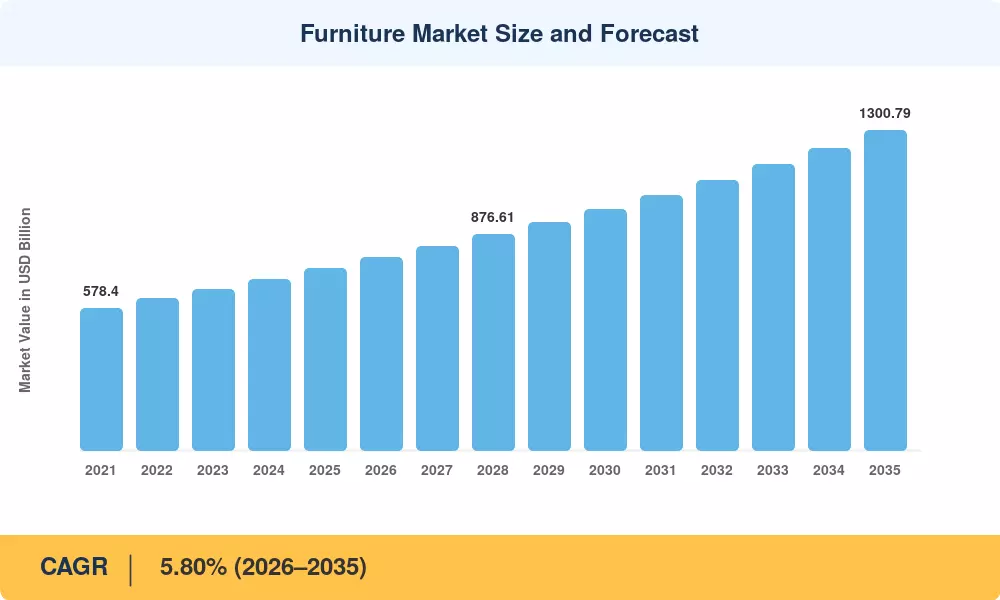

The global Furniture Market reached an estimated USD 740.20 billion in 2025 and is projected to grow from USD 783.13 billion in 2026 to USD 1,300.79 billion by 2035, registering a CAGR of 5.80% during the forecast period (2026–2035). This expansion is anchored in accelerating millennial and Gen-Z homeownership cycles that lagged historical norms by nearly a decade, combined with a wave of hybrid-work office reconfigurations triggered by post-pandemic workplace policy shifts. The U.S. implementation of Section 232 tariffs on certain wood-based furniture imports in October 2025 has simultaneously redirected supply chains and created near-term pricing pressure across North American retail channels [1].

Consumers and commercial buyers alike are pivoting away from mass-produced, single-function pieces toward space-efficient, configurable solutions designed for smaller urban footprints. Investments in direct-to-consumer digital showrooms exceeded USD 4.2 billion globally in 2024, reflecting a structural shift in how the Furniture Market reaches end users. Sustainability certifications — particularly FSC Chain of Custody and BIFMA LEVEL — are no longer differentiators but baseline procurement requirements for institutional buyers, a trend reshaping material sourcing across the value chain [3].

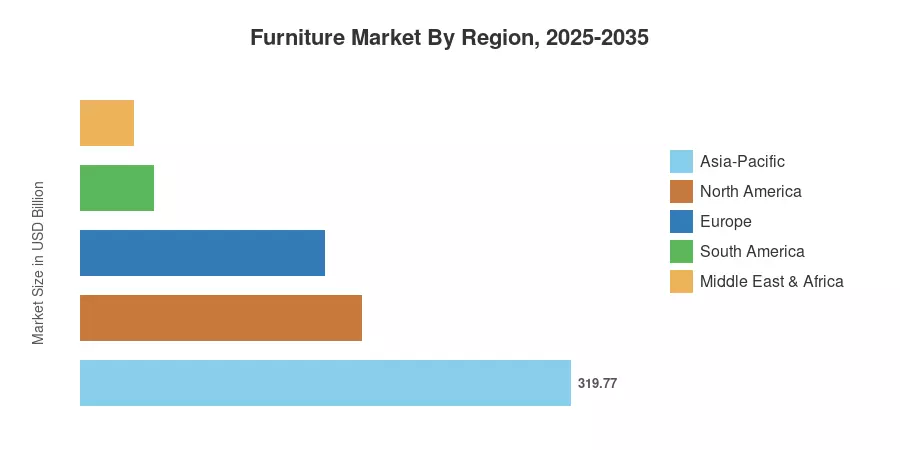

Asia-Pacific commands roughly 43.2% of global Furniture Market revenue, driven by residential construction velocity in China and India and a rising urban middle class across ASEAN nations. North America holds the second-largest share at 24.8%, buoyed by renovation-driven replacement demand and commercial office fit-out cycles. Europe accounts for 21.5%, with the Nordic countries and Germany leading in sustainable product innovation. The Furniture Market trajectory through 2035 will be defined by how efficiently manufacturers integrate circular-economy principles with digital-first distribution.

Key Report Takeaways

• By Application

- Home furniture dominated the Furniture Market with a 58.0% revenue share in 2025, reflecting steady residential construction and renovation activity globally.

- Office furniture is projected to register a 6.7% CAGR through 2035, supported by hybrid-work reconfigurations and corporate ESG-driven procurement mandates.

- Hospitality furniture demand is rising as global hotel construction pipelines in the Middle East and Asia-Pacific resume post-pandemic expansion.

• By Material

- Wood accounted for 55.4% of the Furniture Market share in 2025 due to cost versatility and broad consumer acceptance in residential settings.

- Metal is the fastest-growing material segment at an 8.2% CAGR, driven by recyclability credentials and suitability for compact commercial interiors.

• By Region

- Asia-Pacific leads the Furniture Market at 43.2% of global revenue, with China and India as primary growth engines.

- North America contributes 24.8% of global revenue, anchored by U.S. housing starts and renovation expenditure.

- South America is projected to grow at a 6.4% CAGR through 2035 as Brazilian housing credit programs expand.

Furniture Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining manufacturer revenue disclosures, trade-flow databases (UN Comtrade), retail point-of-sale aggregation, and proprietary primary interviews with 220+ industry stakeholders across 18 countries. Historical figures reflect actuals; forecast values apply a constant-CAGR extrapolation calibrated against macroeconomic inputs from the World Bank and IMF [4].

.webp?v=1784642855)