Luxury SUV Market Summary

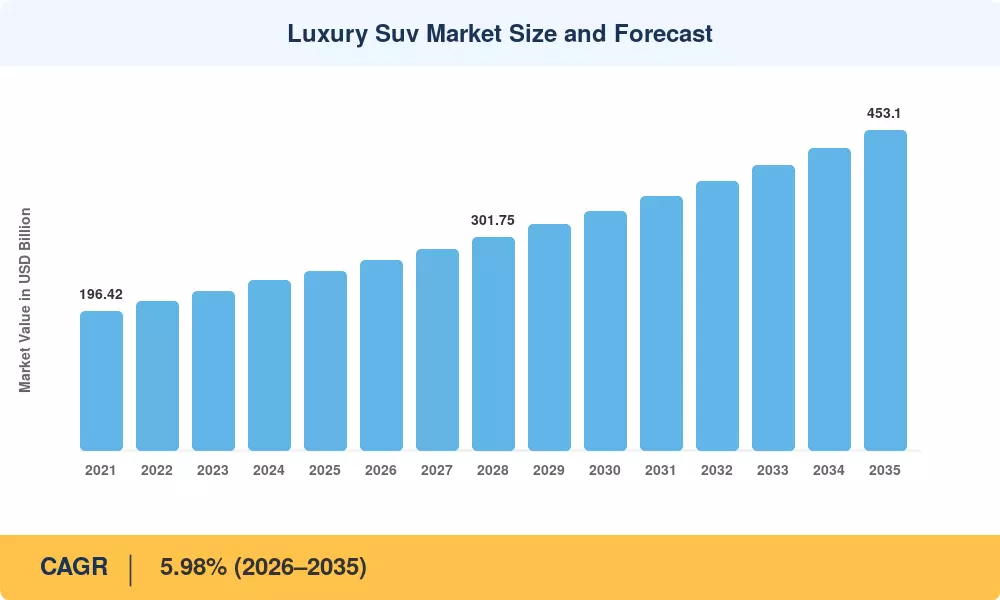

The global Luxury SUV Market stood at USD 253.50 Billion in 2025 and is projected to reach USD 268.66 Billion in 2026 before climbing to USD 453.10 Billion by 2035, registering a CAGR of 5.98% across the forecast window. Two forces are propelling this trajectory: a sustained rise in global high-net-worth individual (HNWI) populations — Knight Frank's 2024 Wealth Report counted 2.7 million ultra-HNWIs worldwide, up 4.2% year-on-year [1] — and an unmistakable buyer migration away from premium sedans toward sport-utility body styles that offer both road presence and interior versatility.

A powertrain transformation is rewriting the competitive playbook across the Luxury SUV Market. Legacy naturally aspirated and turbocharged petrol architectures are giving way to battery-electric platforms, with OEMs committing over USD 515 Billion collectively to electrification through 2030 [2]. The EU's Fit for 55 package, which mandates a 55% CO₂ reduction by 2030 relative to 2021 levels, is accelerating this shift in Europe, while China's dual-credit NEV policy pushes domestic and foreign brands to scale zero-emission SUV line-ups rapidly [3].

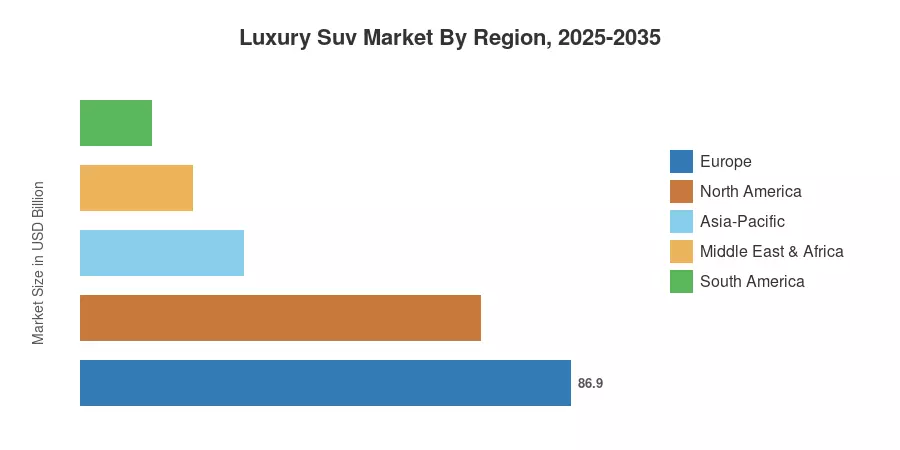

Europe commands the largest slice of the Luxury SUV Market with a 34.28% revenue share in 2024, underpinned by deep brand heritage from German and British marques and robust purchase incentives for zero-emission vehicles. Asia-Pacific is the fastest-growing region at an 11.42% CAGR through 2035, fueled by rising affluence in China and India and expanding public charging networks [4]. North America holds the second-largest share at roughly 28.00%, driven by strong full-size utility demand and favorable consumer financing conditions. The decade ahead promises intensifying competition as electrification, autonomous driving features, and software-defined vehicle platforms converge.

Key Report Takeaways

• By Body Style & Fuel Type

- Crossover SUVs accounted for 55.70% of the Luxury SUV Market in 2024, reflecting consumer preference for car-like handling combined with elevated ride height.

- Battery-electric variants are set to expand at a 26.92% CAGR through 2035, the fastest growth of any fuel segment, as OEMs launch dedicated EV architectures.

- Coupe-style SUVs are projected to grow at a 12.65% CAGR, driven by younger, affluent buyers seeking sportier aesthetics.

• By Drivetrain & Seating Capacity

- All-wheel-drive configurations captured 72.86% of the Luxury SUV Market in 2024, reinforcing consumer expectations of dynamic traction in the premium tier.

- Seven-seat layouts will register a 9.12% CAGR through 2035, propelled by demand among multi-generational households in Asia-Pacific and North America.

• By Region

- Europe held 34.28% of the Luxury SUV Market revenue in 2024, anchored by German, British, and Swedish OEMs.

- Asia-Pacific leads regional growth at an 11.42% CAGR, with China alone representing over 42% of regional revenue.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up OEM shipment data with top-down macroeconomic modelling, cross-validated against customs, registration databases, and annual reports from publicly listed automakers. Historical figures (2021–2024) reflect actual reported revenues, while the forecast period (2026–2035) applies a calibrated compound annual growth rate consistent with powertrain mix evolution, regulatory timelines, and regional wealth projections.