Manhole Covers Market Summary

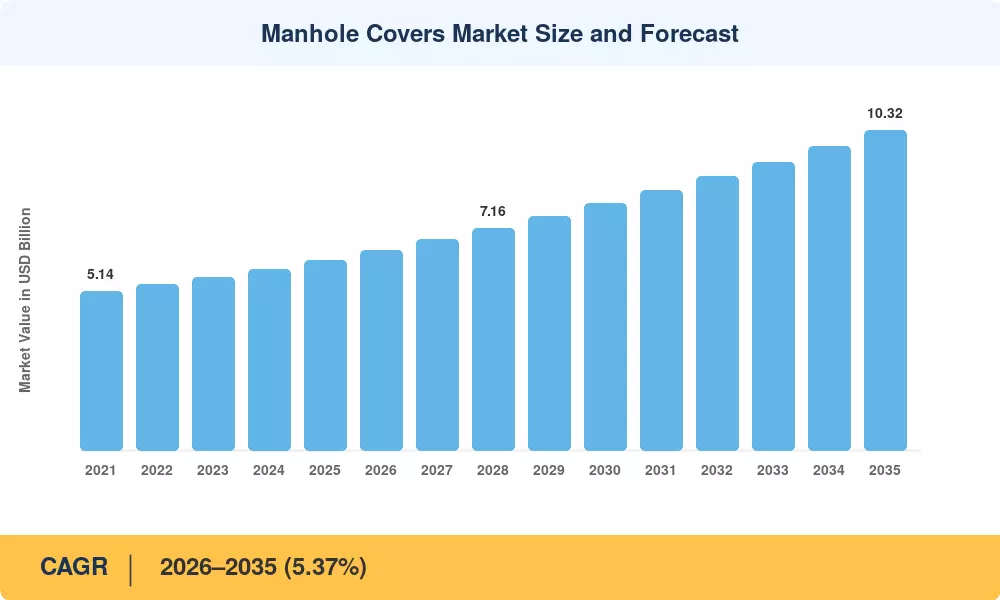

The global Manhole Covers Market was valued at USD 6.12 Billion in 2025 and is projected to grow from USD 6.45 Billion in 2026 to USD 10.32 Billion by 2035, registering a CAGR of 5.37% during the 2026–2035 forecast period. This growth is anchored in accelerating urbanization — the UN projects 68% of the global population will live in cities by 2050 — and the corresponding surge in underground utility buildouts. Governments across the EU, China, and North America have collectively pledged over USD 420 Billion toward water, wastewater, and broadband infrastructure between 2024 and 2032, directly expanding procurement volumes for the Manhole Covers Market [1][2].

A material technology shift is redefining the competitive landscape of the Manhole Covers Market. Traditional grey iron and ductile iron covers, long the default specification, are losing ground to fiber-reinforced polymer (FRP) composites and polymer-concrete alternatives that offer superior corrosion resistance, lower installation weight, and built-in anti-theft characteristics. Telecom operators rolling out 5G small cells require RF-transparent lids that metal simply cannot provide, while smart-city pilot programs in Seoul, Amsterdam, and Singapore are integrating IoT sensors directly into cover assemblies to monitor flood risk, gas accumulation, and unauthorized entry [3][4].

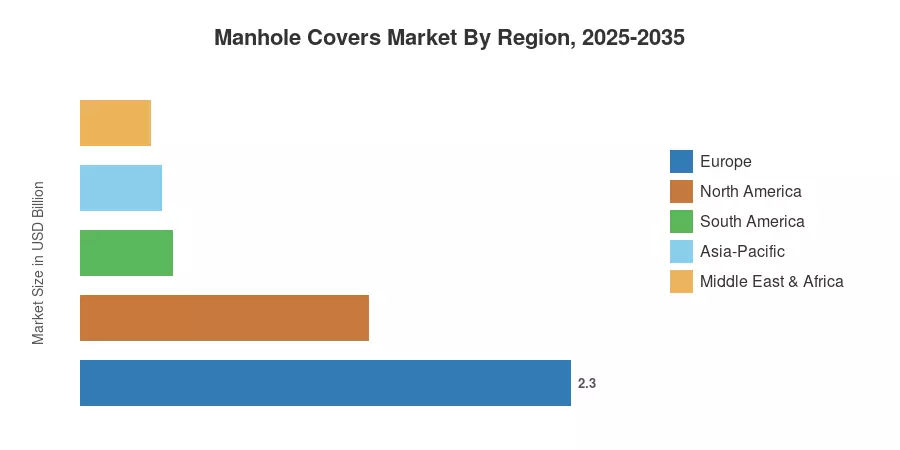

Europe commands the largest share of the Manhole Covers Market at approximately 37.6% of 2025 revenue, driven by strict EN 124-compliant procurement standards and dense underground utility networks. Asia-Pacific is the fastest-growing region, posting an anticipated CAGR of 6.13% through 2035, led by massive metro rail expansions in India and China's "sponge city" stormwater programs. North America holds roughly 22% of the global Manhole Covers Market, where aging water systems and the Bipartisan Infrastructure Law's USD 55 Billion water allocation are sustaining replacement-cycle demand [5][6]. The decade ahead will see material innovation, digital integration, and regulatory harmonization converge to reshape how municipalities procure and manage these essential assets.

Key Report Takeaways

• By Material Type

- Cast Iron captured approximately 42.7% of Manhole Covers Market revenue in 2025, reflecting its continued specification dominance in legacy road and highway projects across Europe and North America.

- Composite materials are forecast to register the fastest material-type CAGR of 6.29% through 2035, propelled by telecom 5G lid requirements and anti-theft mandates.

- Ductile Iron remains the second-largest material segment within the Manhole Covers Market, valued at approximately USD 1.41 Billion in 2025.

• By Application

- Road infrastructure accounted for roughly 31.7% of the Manhole Covers Market in 2025, underpinned by highway resurfacing programs and new expressway construction in Asia.

- Telecommunication and Data applications are projected to expand at a 6.49% CAGR through 2035, the fastest among all application segments.

• By Region

- Europe led the Manhole Covers Market with a 37.6% share in 2025.

- Asia-Pacific is expected to record the highest regional CAGR of 6.13% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from customs trade data, foundry production indices, and municipal procurement filings, while forecast projections integrate urbanization trajectories, infrastructure spending pipelines, and material substitution curves.