Mass Flow Controller Market Summary

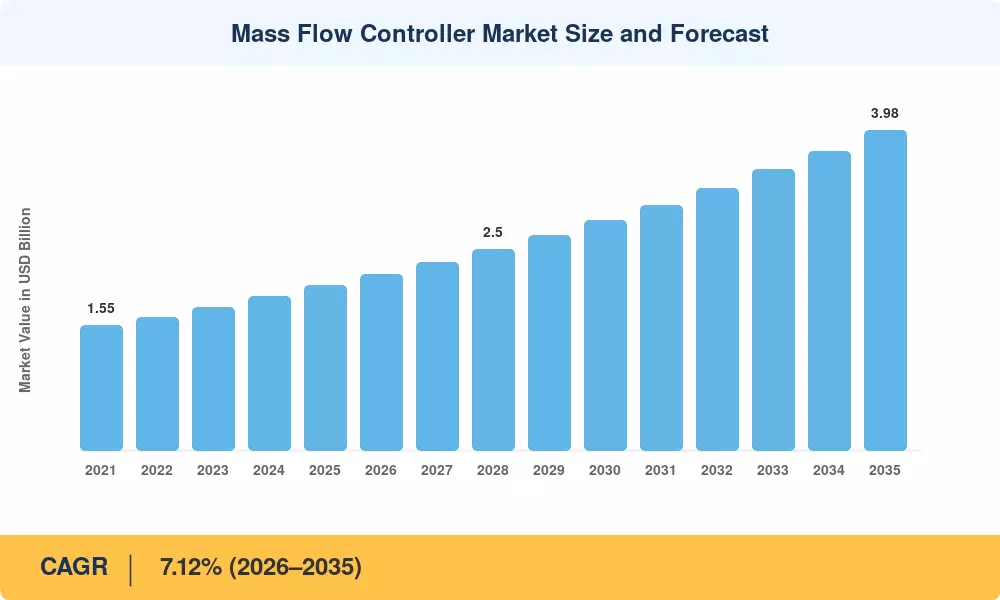

The Mass Flow Controller Market reached an estimated USD 2.05 billion in 2025 and is projected to grow from USD 2.18 billion in 2026 to USD 3.98 billion by 2035, registering a CAGR of 7.12% during the forecast period. This expansion is anchored in two converging forces: semiconductor capital-expenditure commitments exceeding USD 400 billion globally through 2030, and tightening emissions regulations that compel industrial facilities to upgrade gas flow rate control infrastructure[2]. Governments across Asia, Europe, and North America have earmarked subsidy programs specifically targeting precision manufacturing upgrades, creating a sustained procurement cycle for MFC precision flow devices.

A technology transformation is reshaping how facilities manage process gas flow management. Legacy rotameter-based systems and manual needle valves — once standard in chemical plants and pharmaceutical cleanrooms — are being displaced by digital, self-diagnosing thermal mass flow controllers capable of sub-1% accuracy at flow rates below 10 sccm. The U.S. CHIPS and Science Act alone has catalyzed over USD 52 billion in domestic fab investments, each requiring thousands of semiconductor gas flow control units per production line [3]. European REACH and F-gas regulation updates further accelerate retrofit programs, replacing analog meters with networked digital platforms.

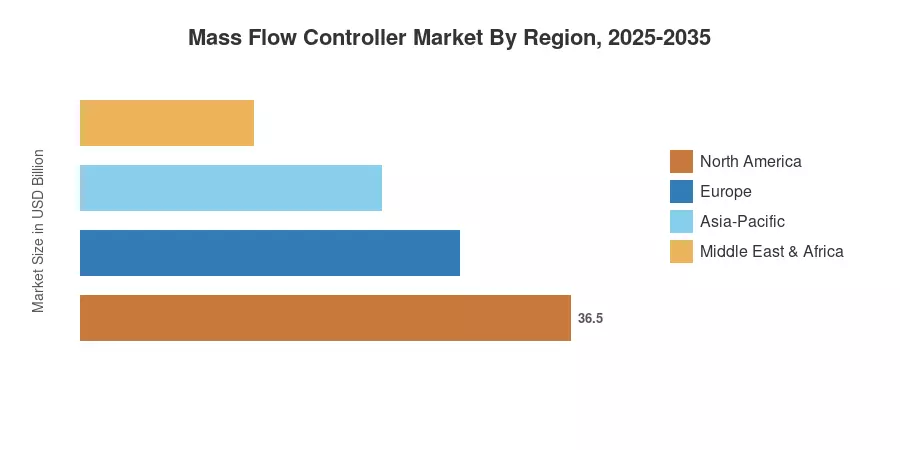

Asia-Pacific dominates the Mass Flow Controller Market with approximately 44.8% share in 2025, driven by China's, South Korea's, and Japan's aggressive fab expansion programs. The region is also the fastest-growing at a projected 10.15% CAGR through 2035. North America holds the second-largest share at roughly 26.3%, buoyed by reshoring incentives and defense-sector demand for gas flow rate control systems. Europe trails at approximately 20.1%, with growth propelled by green hydrogen electrolyzer deployments and pharmaceutical bioprocessing upgrades The decade ahead will see the Mass Flow Controller Market evolve from a component-supply business into a data-rich, service-oriented ecosystem.

Key Report Takeaways

• By Product Type

- Thermal mass flow controllers commanded the largest revenue share in 2025 at approximately 56.4%, reflecting their dominance in semiconductor gas flow control and chemical dosing applications

- Coriolis MFC units are forecast to register a 10.65% CAGR through 2035, driven by demand for direct mass measurement in biologics and green hydrogen process gas flow management

- Pressure-based MFC platforms are gaining traction in high-purity gas delivery, particularly for advanced EUV lithography nodes

• By End-User Industry

- Semiconductor fabrication accounted for roughly USD 0.79 billion of the Mass Flow Controller Market in 2025, reflecting the sector's outsized capital intensity

- Renewable energy and fuel cell applications are poised for a 13.1% CAGR to 2035, the fastest among all end-user verticals

• By Region

- Asia-Pacific captured 44.8% of the Mass Flow Controller Market share in 2025, with China alone representing over 38% of regional revenue

- North America is projected to grow at a 6.45% CAGR through 2035, supported by CHIPS Act funding and defense-sector MFC precision flow devices procurement

- Europe's Mass Flow Controller Market is accelerating due to EU hydrogen strategy mandates and pharmaceutical cleanroom modernization

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s market sizing combines bottom-up revenue modeling from manufacturer shipment data, import/export trade flows, and end-user capital expenditure surveys. Historical figures (2021–2024) are validated against publicly reported revenues of leading thermal mass flow controllers suppliers. Forecast projections (2026–2035) apply a calibrated CAGR derived from demand-side indicators, including fab construction timelines, electrolyzer deployment targets, and pharmaceutical facility expansion permits[4].