Medical Billing Outsourcing Market Summary

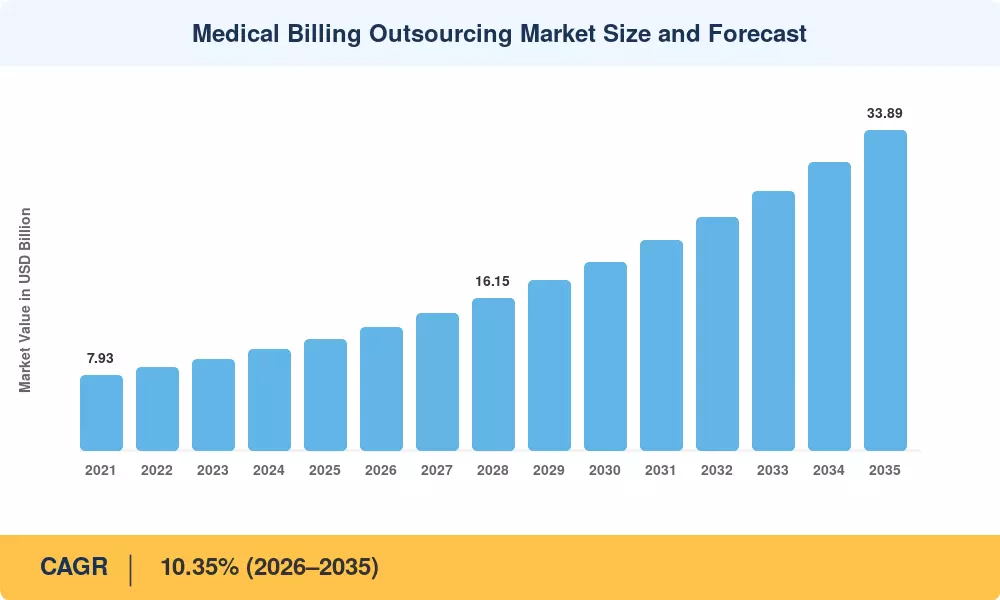

The Medical Billing Outsourcing Market was valued at USD 11.76 billion in 2025 and is projected to reach USD 13.05 billion in 2026 before climbing to USD 33.89 billion by 2035, registering a CAGR of 10.35% during 2026–2035. Healthcare providers across the United States and Europe are accelerating the shift toward third-party billing services as CMS reimbursement models grow more complex and the No Surprises Act (2022) imposes tighter compliance deadlines on claims transparency [2]. Revenue cycle management spending among U.S. hospitals alone exceeded USD 115 billion in 2024, with outsourced billing capturing an increasing slice of that total [3].

A technology transformation is reshaping how healthcare claims processing gets done. Legacy paper-based workflows and on-premise billing engines are giving way to cloud-native platforms that embed artificial intelligence for ICD coding outsourcing, real-time eligibility verification, and predictive denial management. Vendors investing in AI-powered revenue cycle management platforms have demonstrated up to 37% reductions in claim denial rates and 25-day improvements in days-in-accounts-receivable, according to a 2024 HFMA survey [4]. The result is a structural shift: outsourcing is no longer a cost play but an accuracy and speed imperative.

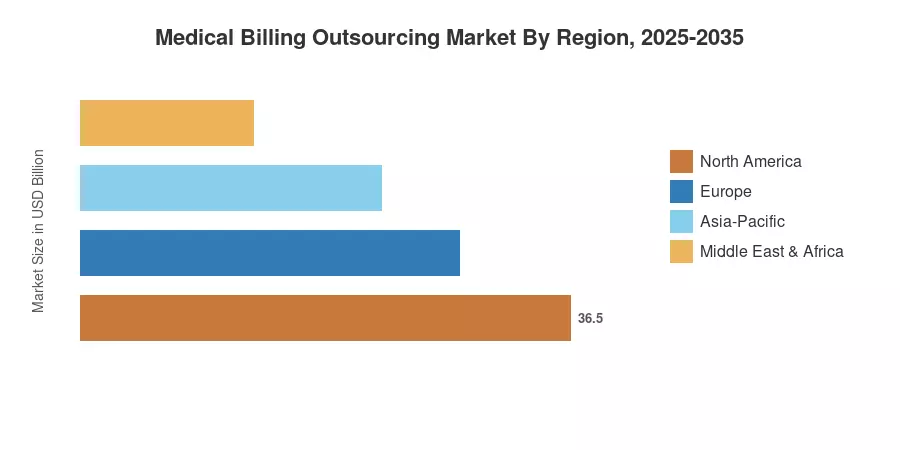

North America commands roughly 45.72% of the Medical Billing Outsourcing Market, driven by the complexity of U.S. payer systems and chronic coder shortages. Asia-Pacific is the fastest-growing region at a 11.92% CAGR through 2035, fueled by India's dominance in offshore healthcare claims processing and the expansion of insurance reimbursement services across Southeast Asia Europe holds the second-largest share at approximately 22.5%, supported by NHS digital transformation programs and EU cross-border billing harmonization efforts. The Medical Billing Outsourcing Market is poised to triple in value over the next decade as regulatory complexity, labor economics, and technology convergence accelerate outsourcing adoption globally.

Key Report Takeaways

• By Service

- Front-End services captured 45.87% of the Medical Billing Outsourcing Market revenue in 2025, anchored by patient registration and eligibility verification workflows

- Middle-End coding and healthcare claims processing segments are expanding at 11.38% CAGR through 2035, reflecting intensifying demand for accurate ICD coding outsourcing

- Back-End services — including payment posting and insurance reimbursement services — reached USD 2.94 billion in 2025

• By Deployment

- Cloud-based delivery accounted for 56.65% of the Medical Billing Outsourcing Market in 2025, as providers favor SaaS-based revenue cycle management platforms

- On-premise solutions are declining but retain relevance among large health systems with legacy EHR integrations

• By End User

- Hospitals represented the largest end-user category, commanding 51.82% of the Medical Billing Outsourcing Market share in 2025

- Ambulatory and other providers register the highest growth at 10.72% CAGR through 2035, driven by rising outpatient volumes

• By Region

- North America contributed USD 5.38 billion in 2025 revenue, anchored by U.S. third-party billing services demand

- Asia-Pacific posts the fastest CAGR of 11.92% through 2035

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling from over 150 billing service providers, validated against top-down insurance reimbursement services expenditure data from CMS, NHS Digital, and IRDAI filings. Historical figures (2021–2024) are based on audited revenues and disclosed contract values; the forecast (2026–2035) applies a calibrated CAGR of 10.35% with adjustments for regulatory milestones and technology adoption curves.

.webp?v=1783416341)