Medical Device Cleaning Market Summary

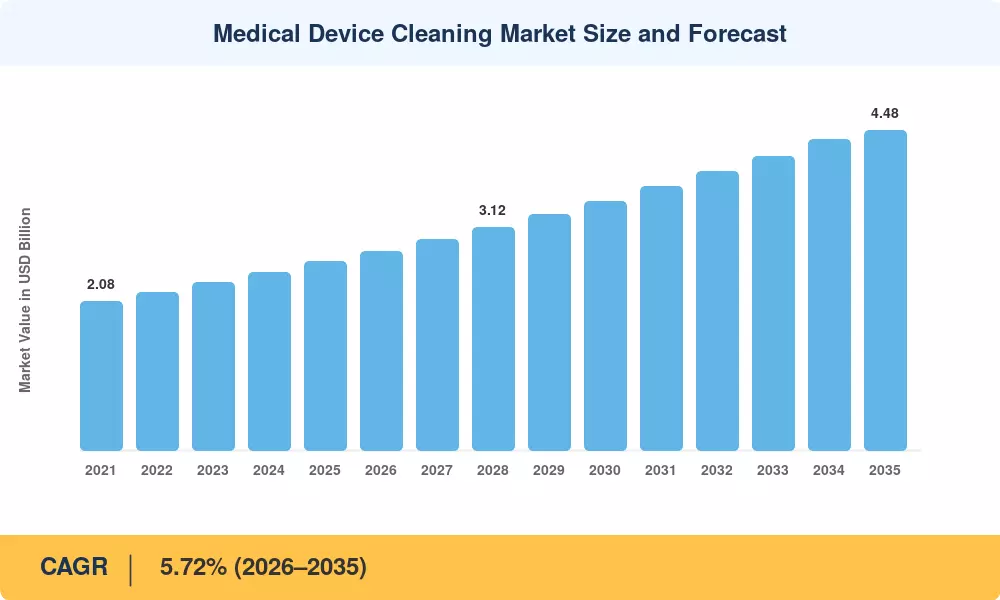

The Medical Device Cleaning Market was valued at USD 2.65 billion in 2025 and is projected to reach USD 2.79 billion in 2026 before climbing to USD 4.48 billion by 2035, registering a CAGR of 5.72% during the 2026–2035 forecast period. This trajectory is anchored to a persistent reality: roughly 1 in 31 hospitalized patients in the United States contracts a healthcare-associated infection (HAI) during any given admission [1]. Regulatory bodies — from the U.S. FDA's updated reprocessing guidance to the European Union's Medical Device Regulation 2017/745 — now mandate documented cleaning validation for every reusable device, locking in baseline demand for enzymatic detergents and automated washer-disinfectors across acute-care and ambulatory settings.

A technology transition is reshaping how facilities approach sterilization of surgical instruments and reusable device decontamination. Legacy manual scrubbing protocols are giving way to automated washer-disinfectors equipped with digital cycle monitoring, while low-temperature enzyme-based detergents are displacing ethylene oxide sterilization amid growing environmental scrutiny. The U.S. EPA's tightened emission standards for ethylene oxide facilities, finalized in 2024, have accelerated capital reallocation toward alternative chemistries and UV/ozone-based systems. Global investment in endoscope reprocessing infrastructure alone exceeded USD 420 million in 2024 [2].

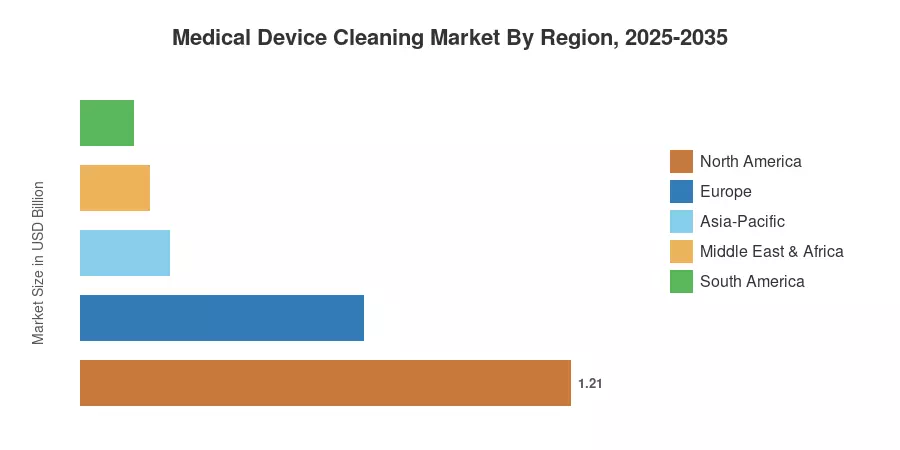

North America commands approximately 45.7% of the Medical Device Cleaning Market, driven by stringent CDC and Joint Commission compliance frameworks. Asia-Pacific represents the fastest-growing region at a projected 8.38% CAGR through 2035, propelled by hospital infrastructure expansion across India, China, and Southeast Asia. Europe holds the second-largest share at roughly 26.3%, supported by MDR 2017/745 enforcement timelines. As surgical volumes continue to rise globally and outpatient facility counts multiply, the Medical Device Cleaning Market is positioned for sustained, regulation-driven expansion through the next decade.

Key Report Takeaways

• By Product Type

- High-Level Disinfectants captured 39.5% of Medical Device Cleaning Market revenue in 2025, reflecting their critical role in hospital disinfection protocols for semi-critical and critical devices

- Enzymatic Detergents are projected to expand at 7.15% CAGR through 2035, driven by the shift toward low-temperature cleaning chemistries compatible with modern reusable device decontamination workflows

- Non-Enzymatic Detergents contributed approximately USD 0.48 billion in 2025 revenue, serving as baseline cleaners in manual pre-cleaning steps

• By Cleaning Process

- Automated Washer-Disinfectors led the Medical Device Cleaning Market with 43.5% revenue share in 2025, benefiting from hospital mandates requiring validated autoclave sterilization methods and documented cycle logs

- UV/Ozone/Emerging Technologies are forecast to grow at 8.01% CAGR to 2035, as facilities seek ethylene oxide alternatives for endoscope reprocessing

• By Application

- Surgical Instruments accounted for 42.7% of the market in 2025, reflecting the dominance of sterilization of surgical instruments in central sterile processing departments

- Endoscopes are forecast to rise at 7.45% CAGR through 2035, as GI and pulmonary procedure volumes grow and endoscope reprocessing standards tighten

• By End User

- Hospitals contributed 48.1% of Medical Device Cleaning Market revenue in 2025

- Ambulatory Surgical Centers are advancing at 7.78% CAGR, propelled by the migration of procedures to outpatient facilities with dedicated reusable device decontamination requirements

• By Region

- North America commanded 45.7% of revenue in 2025; Asia-Pacific is poised for the fastest growth at 8.38% CAGR between 2026–2035

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue analysis of cleaning chemical and equipment sales across 42 countries, validated against hospital procurement databases, regulatory filing volumes, and top-down cross-referencing with published healthcare expenditure data from WHO and OECD sources [3].