Medical Device Contract Manufacturing Market Summary

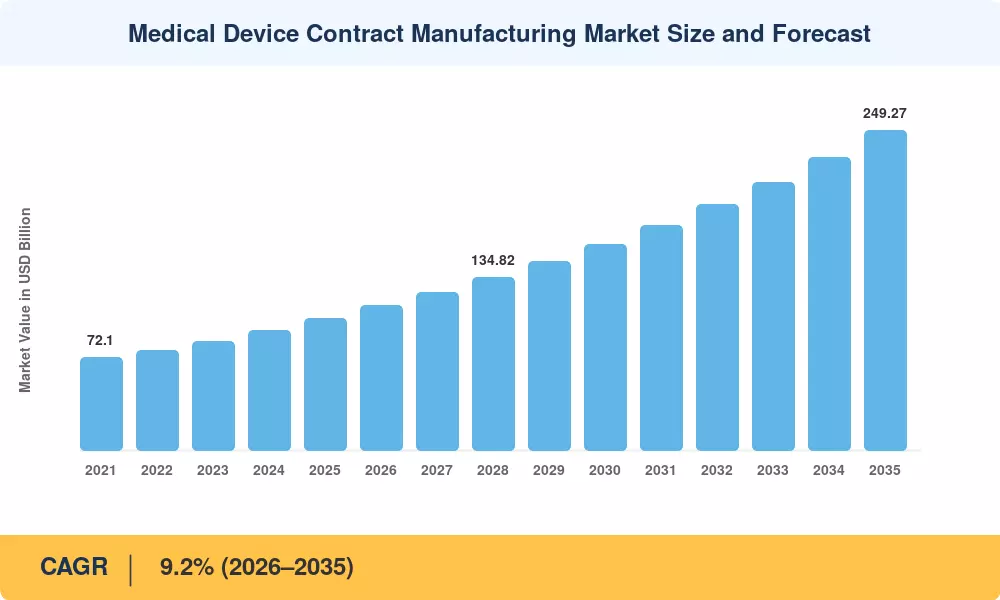

The Medical Device Contract Manufacturing Market reached a valuation of USD 102.48 billion in 2025 and is projected to grow from USD 112.87 billion in 2026 to USD 249.27 billion by 2035, registering a CAGR of 9.2% during the forecast period (2026–2035). This trajectory reflects an industry-wide shift by original equipment manufacturers toward strategic outsourcing, driven by mounting cost pressures and a regulatory environment that has grown more complex following the EU's Medical Device Regulation (EU MDR 2017/745) full enforcement and the U.S. FDA's evolving 510(k) pathway reforms [1][2]. Contract manufacturers have positioned themselves as indispensable partners in navigating these requirements while keeping production timelines competitive.

The way contract manufacturers function in the Medical Device Contract Manufacturing Market is changing due to a major technological shift. Industry 4.0 infrastructure, which includes digital twins, real-time statistical process control, and automated inspection systems, is enabling digitally connected smart factories to replace outdated batch-processing lines. A 2024 investigation found that medtech businesses that implemented smart-factory concepts cut time-to-market by up to four months and decreased production failures by 35–50% [3]. CMOs with established digital infrastructure are in high demand as regulatory agencies increasingly want electronic design history files and unique device identification (UDI) traceability [4].

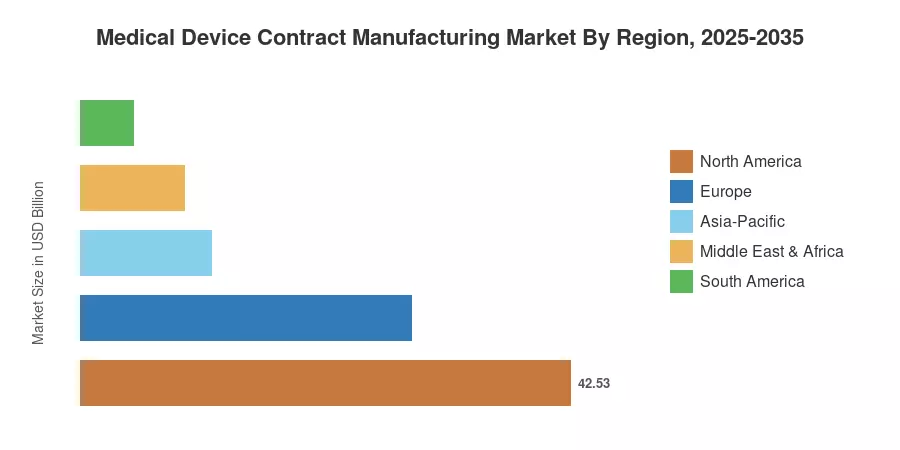

With a strong regulatory framework based on FDA oversight and a concentrated presence of international OEMs, North America has around 41.5% of the Medical Device Contract Manufacturing Market from a regional perspective. The fastest-growing region is Asia-Pacific, which is expected to grow at a compound annual growth rate (CAGR) of 11.1% through 2035 thanks to competitive labor costs, increased sterilization and cleanroom capacity in China and India, and government incentives like India's Production-Linked Incentive (PLI) scheme for medical devices [5]. Europe has the second-largest share, at about 28.0%, thanks to established precision-engineering hubs in Germany and Switzerland as well as EU MDR compliance requirements.

Key Report Takeaways

• By Device Type

- In-vitro diagnostic (IVD) devices captured a 29.8% revenue share of the Medical Device Contract Manufacturing Market in 2025, reflecting sustained global demand for point-of-care and molecular diagnostics platforms.

- Drug-delivery devices are forecast to expand at a 12.6% CAGR through 2035, propelled by the proliferation of autoinjectors, wearable infusion systems, and combination drug-device products.

• By Service Type

- Device development and manufacturing services held a 57.0% share of the Medical Device Contract Manufacturing Market in 2025, underscoring the dominance of end-to-end production partnerships.

- Quality management services are advancing at a 12.8% CAGR to 2035, as OEMs increasingly outsource post-market surveillance and regulatory submission support.

• By Region

- North America commanded 41.5% share of the Medical Device Contract Manufacturing Market in 2025, led by the United States' concentrated medtech ecosystem.

- Asia-Pacific is projected to grow at an 11.1% CAGR through 2035, driven by capacity expansion and favorable manufacturing economics.

Market Size and Forecast (2021–2035)

Market Research Future employs a combination of bottom-up revenue modeling — drawing on contract manufacturer financial disclosures, OEM outsourcing expenditure analysis, and regional capacity utilization data — supplemented by top-down validation against macroeconomic healthcare spending indicators from the WHO and World Bank [6][7]. Historical figures reflect actual reported revenues, while forecast values apply a calibrated compound growth framework adjusted for anticipated regulatory, demographic, and technology-driven shifts across the Medical Device Contract Manufacturing Market.