Medical Device Security Market Summary

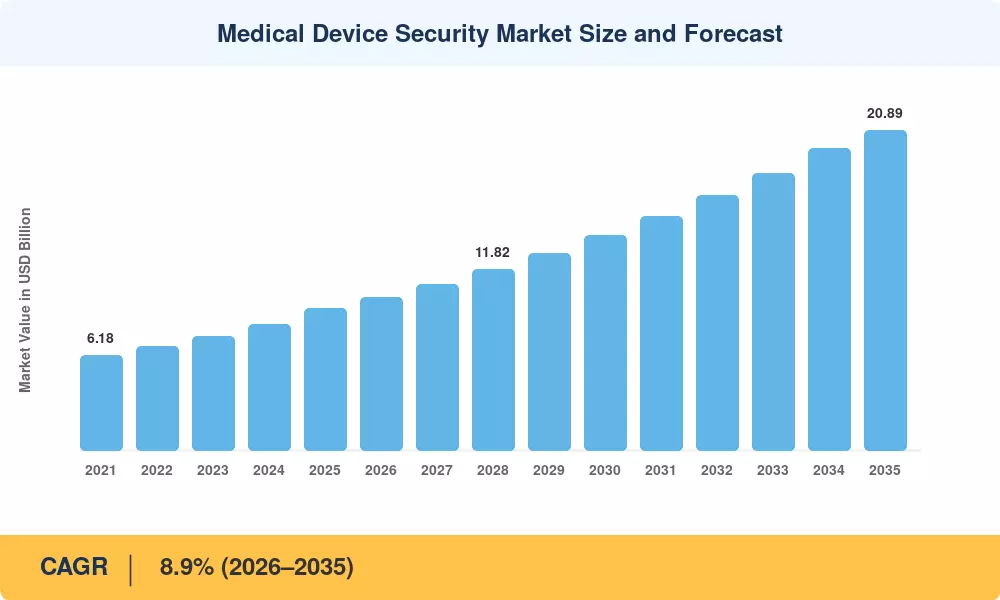

The Medical Device Security Market reached an estimated USD 9.24 Billion in 2025, reflecting the accelerating urgency around protecting connected clinical infrastructure from cyber threats. Starting from a forecast base of USD 9.96 Billion in 2026, the Medical Device Security Market is projected to expand to USD 20.89 Billion by 2035, registering a CAGR of 8.9% across the 2026–2035 forecast window. Two catalysts are shaping this trajectory: the FDA's strengthened premarket cybersecurity requirements under Section 524B of the FD&C Act, and the cumulative cost of healthcare data breaches, which averaged USD 10.93 million per incident in 2023, the highest of any sector for the thirteenth consecutive year [2].

A sweeping technology shift is underway within hospital networks. Legacy perimeter-based firewalls and siloed antivirus tools are giving way to integrated IoMT data protection platforms that combine real-time device discovery, behavioral anomaly detection, and automated patch orchestration. The U.S. Department of Health and Human Services allocated over USD 1.3 Billion in cybersecurity-related grants and technical assistance programs between 2023 and 2025, accelerating this modernization cycle [3]. Connected device vulnerability management now ranks among the top three capital priorities for hospital CISOs surveyed by CHIME in 2024.

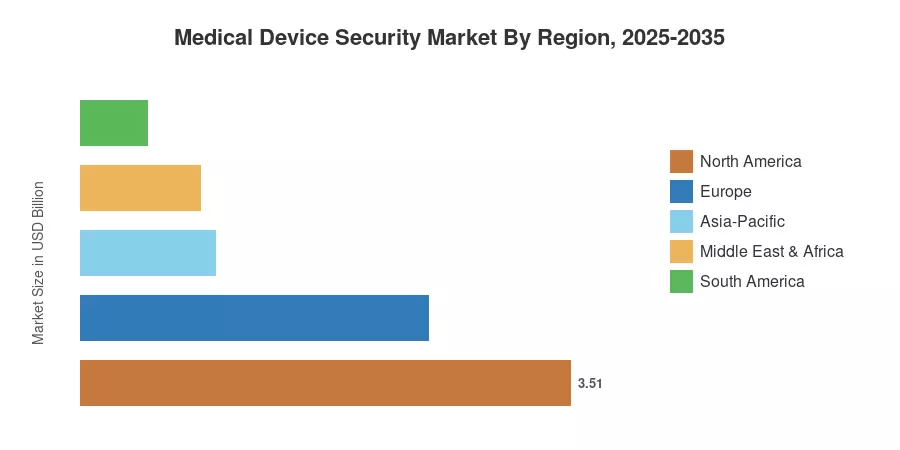

North America commands roughly 38% of the global Medical Device Security Market, buoyed by stringent FDA cybersecurity compliance mandates and a dense installed base of networked clinical devices. Asia-Pacific is the fastest-growing region at an estimated CAGR exceeding 10.5%, fueled by rapid hospital digitization campaigns in China, India, and Japan. Europe holds the second-largest share at approximately 27%, driven by the EU Medical Device Regulation (MDR) and the NIS2 Directive's expanded scope covering healthcare entities. As ransomware threats intensify and regulatory frameworks tighten globally, spending on patient data breach prevention is set to accelerate through the decade.

Key Report Takeaways

• By Solution

- Data Loss Prevention Solutions account for approximately 24% of the Medical Device Security Market, driven by tightening HIPAA enforcement and cross-border data transfer rules

- Encryption Solutions are expanding at a CAGR of 10.2% through 2035, reflecting growing demand for end-to-end IoMT data protection across telehealth platforms

- Network and Endpoint Security solutions represent an estimated USD 2.31 Billion in 2025, as hospitals scale zero-trust architectures to address connected device vulnerability

• By Device Type

- Hospital Medical Devices dominate with over 47% share of the Medical Device Security Market, given the high volume of networked imaging and infusion systems in acute-care settings

- Wearable and External Medical Devices exhibit the fastest growth, with remote patient monitoring expanding the attack surface and raising the urgency of healthcare cybersecurity

• By Region

- North America leads with a 38% revenue share, anchored by the FDA cybersecurity compliance framework and active enforcement by the HHS Office for Civil Rights

- Asia-Pacific is projected to grow at a CAGR of 10.5%, as China's Class III device cybersecurity guidelines and India's Digital Health Mission amplify demand for patient data breach prevention

- Europe captures approximately USD 2.49 Billion in 2025, supported by MDR Annex I cybersecurity requirements and the NIS2 Directive's incident-reporting mandates

Market Size and Forecast (2021–2035)

The following table presents historical and forecast market sizing for the Medical Device Security Market based on MRFR's proprietary methodology combining bottom-up vendor revenue analysis, top-down macroeconomic modeling, and primary expert interviews across 14 countries. Historical data reflects actual vendor disclosures and regulatory filings, while forecast figures incorporate scenario-weighted demand projections.