Medical Device Testing Services Market Summary

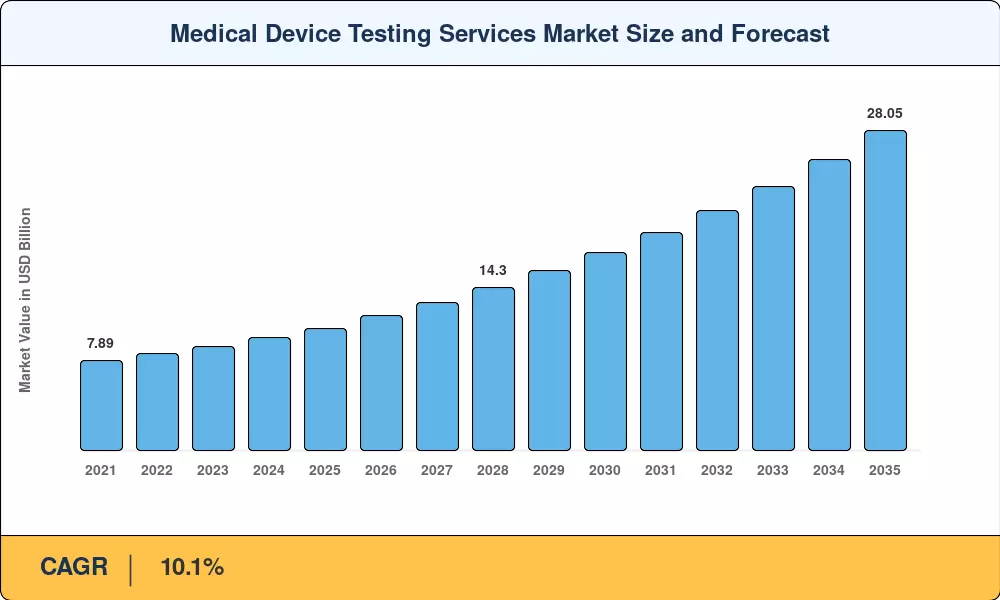

The Global Medical Device Testing Services Market size was valued at USD 10.72 Billion in 2025, and the market is projected to grow from USD 11.80 Billion in 2026 to USD 28.05 Billion by 2035, registering a CAGR of 10.1% during the forecast period 2026–2035. Two forces sit behind this trajectory: the FDA's 2023 cybersecurity pre-market guidance now compels every connected-device maker to demonstrate threat modeling, software bill-of-materials integrity, and patch-management capability before clearance [1], while the EU Medical Device Regulation (MDR) transition deadline has funneled thousands of legacy CE-marked products back through conformity assessment, overwhelming in-house validation teams and pushing spend toward accredited third-party labs [2].

The technology transition in this field is centered around the move from exclusively wet-lab biocompatibility and sterility processes to integrated digital + bench workflows. In-silico toxicological platforms and computational fatigue models already satisfy parts of ISO 10993 standards, reducing animal-study timeframes by 20-30% for qualifying device materials [3]. The FDA’s 2024 draft guidance on computer modeling and simulation (CM&S) for medical devices actively incentivizes this move, allowing sponsors to supplement physical testing with validated simulations, a policy shift anticipated to save manufacturers USD 1.2 billion in total through 2030 [4].

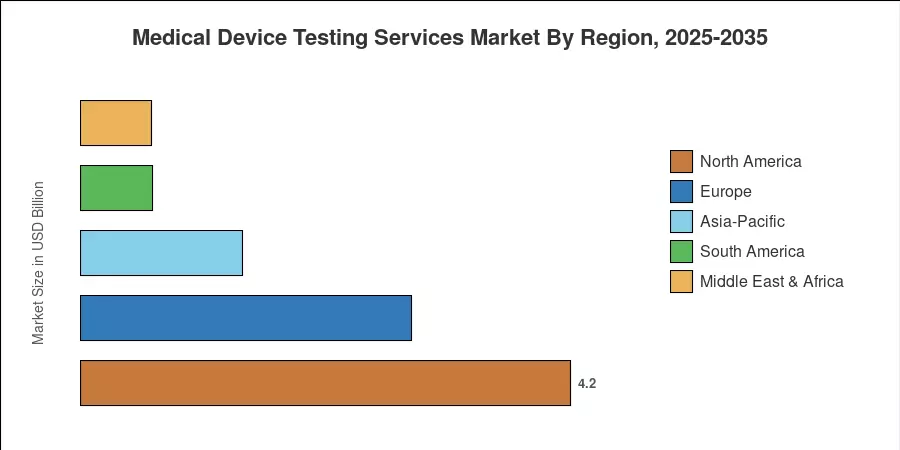

The North American market for medical device testing services accounted for 39.2% of the total market in 2024, driven by the world's most extensive network of FDA-registered testing labs and a substantial MedTech OEM presence focused in Minnesota, Massachusetts and Southern California. Asia-Pacific is the fastest developing area at 13.0% CAGR, driven by China’s NMPA reform goal and India’s burgeoning CDSCO infrastructure. Europe is second at 26.5%, because of re-certification traffic from MDR that will continue far into the late 2020s. The medical device testing services industry is set to see a decade of structurally elevated demand due to rising device complexity, from AI-powered surgical robots to biodegradable cardiac stents.

Key Report Takeaways

• By Service Type

- Biocompatibility testing commanded 32.0% of the medical device testing services market in 2024, reflecting the non-negotiable nature of ISO 10993 requirements across all device classes.

- Electrical safety and EMC testing are forecast to expand at a 14.5% CAGR through 2035, driven by the proliferation of connected wearables and AI-enabled implantables.

• By the Development Phase

- Pre-clinical testing protocols accounted for 47.5% of demand in 2024, as most regulatory pathways front-load evidence generation before first-in-human studies.

- Post-market surveillance testing will advance at a 13.8% CAGR to 2035, fueled by MDR Article 83 obligations and FDA post-market cybersecurity mandates.

• By Device Class

- Class II devices represented 55.0% of global testing volume in 2024.

- Class III device testing is set to grow at a 14.8% CAGR, tied to rising complexity in combination products and AI/ML-enabled diagnostics.

• By End User

- Medical device OEMs generated 61.0% of total spending in 2024.

- Contract research organizations are forecast to expand at a 12.8% CAGR as outsourcing accelerates among mid-tier manufacturers.

• By Geography

- North America held 39.2% of the medical device testing services market, supported by a dense regulatory infrastructure.

- Asia-Pacific will post the strongest regional CAGR at 13.0% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future used a bottom-up revenue research approach across accredited testing labs and CROs. It notified body service arms to build historical estimates for the medical device testing services industry, cross-referenced with published financials and third-party benchmarks. Forecast-period forecasts are based on a calibrated 10.1% CAGR, anchored on regulatory-pipeline demand modeling.