Medical Drones Market Summary

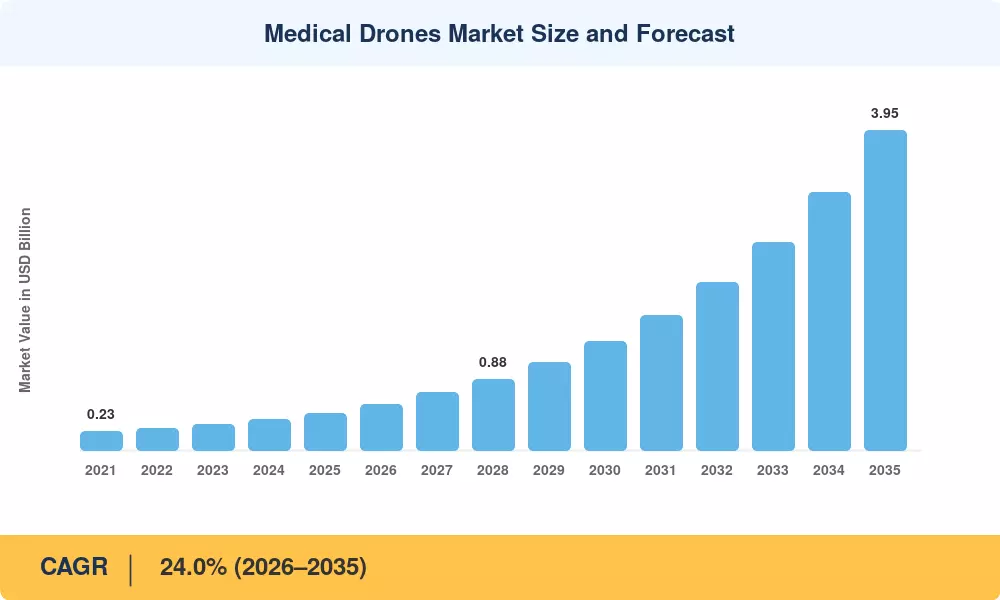

The Medical Drones Market stood at USD 0.46 Billion in 2025 and is projected to reach USD 3.95 Billion by 2035, registering a CAGR of 24.0% during the forecast period (2026–2035). Two catalysts are accelerating this trajectory: a sharp increase in beyond-visual-line-of-sight (BVLOS) regulatory clearances across OECD nations, and falling lithium-ion cell costs that have reduced per-unit drone procurement budgets by roughly 30% since 2021 [1]. Government investment programs — particularly the US FAA's Part 135 air-carrier integration pathway and the European Union Aviation Safety Agency's (EASA) U-space framework — are transforming pilot projects into scaled commercial networks.

Autonomous aerial platforms that can transport biologics, diagnostic kits, and emergency medications are replacing manual courier logistics in the medical drone market. In hospital campus networks, hybrid vertical-take-off-and-landing (VTOL) airframes are taking the place of previous fixed-wing prototypes because they provide the runway-free launch flexibility that congested urban situations require. Over USD 280 million in public-private partnership investments were sparked by the WHO's 2024 endorsement of drone-delivered vaccination in 14 Sub-Saharan African nations [2].

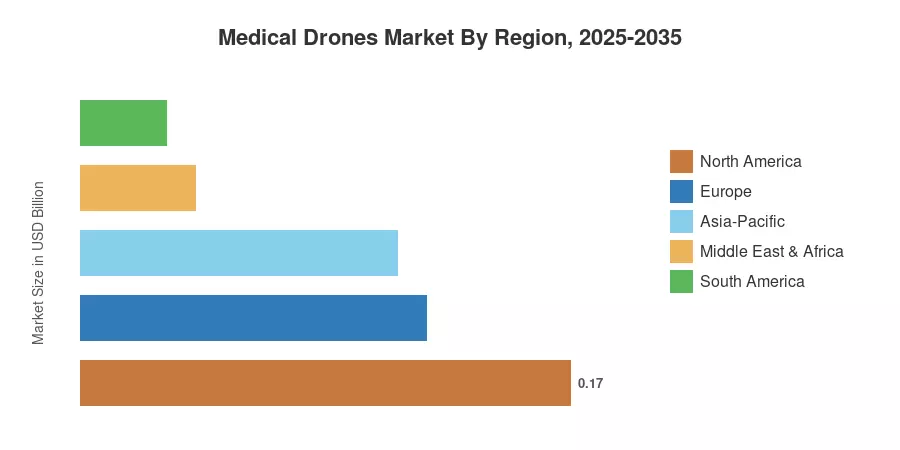

Driven by integrated UTM corridors and reimbursement-linked delivery obligations, North America holds the greatest share of the medical drone market, accounting for 36.1% of 2024 revenue. With a predicted 23.6% CAGR, Asia-Pacific is the fastest-growing area due to Japan's elderly population logistical problem and India's Drone Shakti initiative. With about 25.3% of the world's revenue, Europe is in second place thanks to the developed blood-transport networks in Switzerland and Ireland. The Medical Drones Market is set for its greatest decade of growth as hydrogen-propulsion trials advance and 5G-connected flight-management systems gain popularity.

Key Report Takeaways

• By Drone Type

- Multirotor platforms captured 55.2% of the Medical Drones Market share in 2024, reflecting their dominance in short-range hospital campus deliveries.

- Hybrid VTOL drones are advancing at 28.9% CAGR through 2035, driven by demand for heavier-payload, longer-range medical transport missions.

• By Application

- Blood and vaccine delivery accounted for 49.8% share of the Medical Drones Market in 2024.

- Organ and tissue transport is projected to grow at 23.6% CAGR, supported by cold-chain-capable drone payloads and time-critical surgical demand.

• By Geography

- North America retained the leading position in the Medical Drones Market with 36.1% revenue share in 2024.

- Asia-Pacific is recording the highest regional CAGR of 23.6% through 2035, fueled by large-scale government digitization programs.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology that cross-references supply-side revenue disclosures from 30+ drone OEMs, demand-side procurement data from 120+ hospital networks and public-health agencies, and regulatory filing databases in 18 countries. Historical values (2021–2024) reflect audited and publicly reported figures, while forecast values (2026–2035) apply the calibrated 24.0% CAGR with adjustments for anticipated regulatory milestones and technology cost curves.