Medical Electrode Market Summary

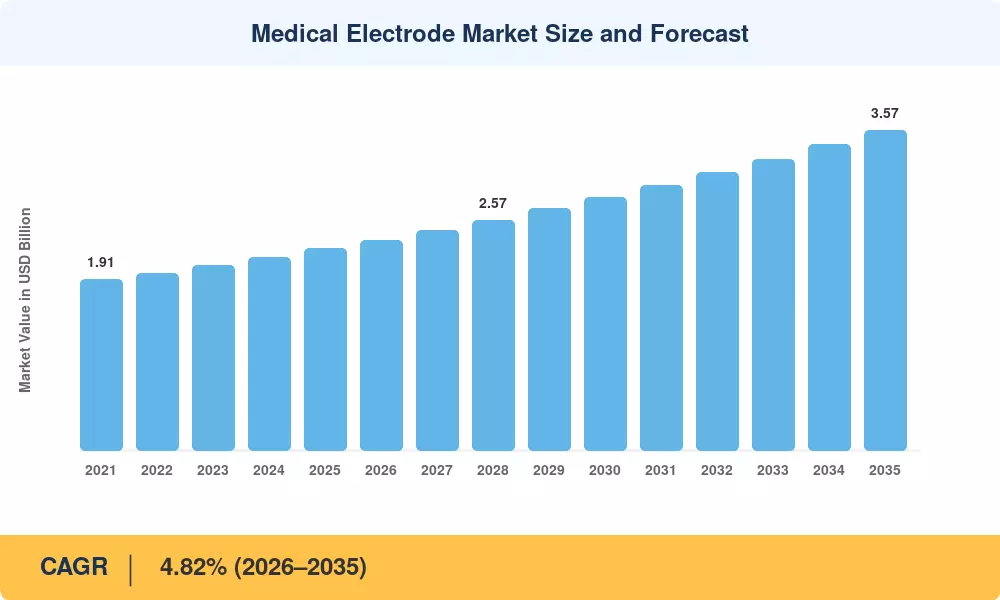

The Medical Electrode Market size was valued at USD 2.25 Billion in 2025, and the market is projected to grow from USD 2.34 Billion in 2026 to USD 3.57 Billion by 2035, registering a CAGR of 4.82% during the forecast period 2026–2035. This growth trajectory draws direct energy from two structural catalysts: the global rise in cardiovascular and neurological disease burden — with the WHO reporting over 17.9 million annual cardiovascular deaths worldwide — and accelerated government investment in remote patient monitoring infrastructure, particularly across CMS reimbursement expansions in the United States and EU MDR compliance mandates reshaping device specifications across Europe [1][2].

The landscape of the medical electrode market is being subtly altered by a technological revolution. Dry-contact and printed flexible electrode platforms that interface directly with wearable biosensor systems are replacing traditional wet-gel electrode formats, which have long been the standard for clinical diagnosis. Advances in conductive polymers and silver-silver chloride nano-coating are driving electrode innovation toward thinner, skin-conformable designs in the wearable medical device market, which is expected to be worth over USD 22 billion by 2024. The FDA and other regulatory agencies have expedited the time-to-market for next-generation electrode assemblies by introducing pre-certification paths for AI-enabled cardiac monitoring devices [4].

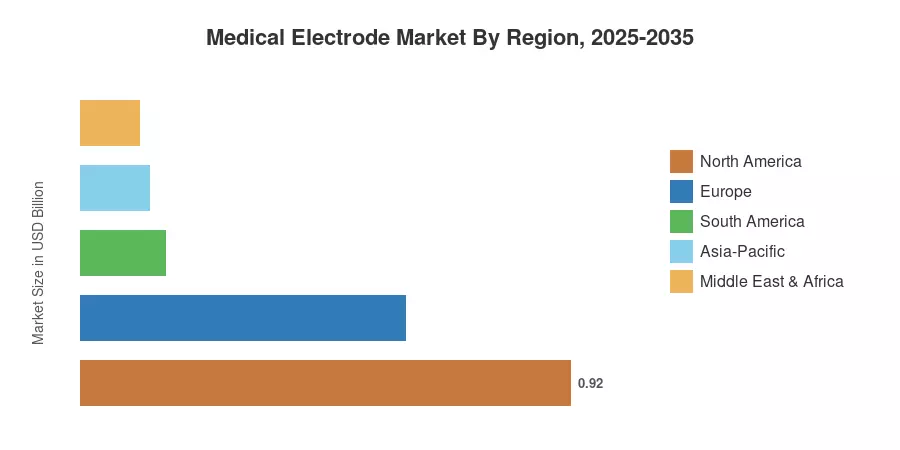

Due to well-established hospital procurement networks and advantageous insurance reimbursement schedules, North America holds around 41% of the medical electrode market. With a 5.70% CAGR through 2035, Asia-Pacific has the strongest development trajectory thanks to growing domestic manufacturing capacity in South Korea, Japan, and China. Europe has the second-largest market, at around 27%, with demand centered around clinical routes for the aging population and cardiac rehabilitation programs in Germany, France, and the Nordic nations. As the therapy of chronic diseases shifts from acute-care facilities to home and ambulatory settings, the medical electrode market is positioned for long-term, stable growth.

Key Report Takeaways

• By Product Type

- Surface electrodes captured 49% of the Medical Electrode Market share in 2025, driven by high-volume ECG and Holter monitoring utilization across hospital and outpatient settings.

- Needle electrodes are projected to expand at a 6.70% CAGR through 2035, fueled by rising electromyography (EMG) procedure volumes in neurology departments.

• By Technology

- Wet gel electrodes retained approximately 48% revenue share within the Medical Electrode Market in 2025, reflecting their established role in acute-care diagnostics.

• By Usability Type

- Disposable formats accounted for 72% of total unit volume in 2025, supported by infection-control mandates and single-use procurement policies across hospital networks.

• By Region

- North America generated approximately USD 0.92 billion in Medical Electrode Market revenue during 2025, maintaining its position as the dominant regional buyer.

- Asia-Pacific is set to record the fastest regional CAGR of 5.70% through 2035, led by government healthcare modernization initiatives in China and India.

Medical Electrode Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining bottom-up revenue analysis from manufacturer filings, top-down demand modeling from hospital procurement databases, and cross-validation against regulatory import-export records across 42 countries. Historical data (2021–2024) is derived from audited company financials and public health procurement disclosures, while forecast projections (2026–2035) apply a compound annual growth model calibrated to macro-epidemiological trends and technology adoption curves.