Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

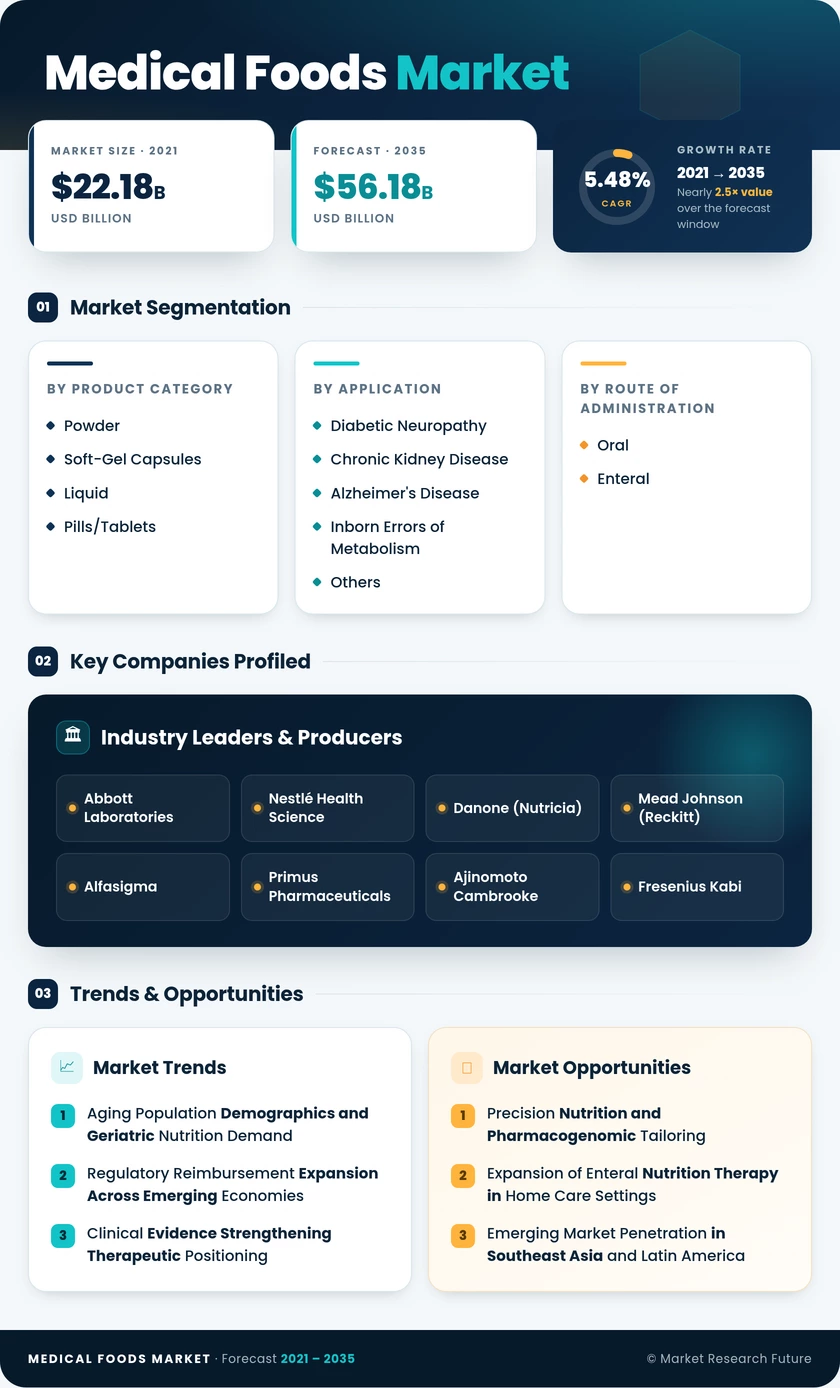

| Product Category | Powder, Soft-Gel Capsules, Liquid, Pills/Tablets | Powder | Soft-Gel Capsules |

| Application | Diabetic Neuropathy, Chronic Kidney Disease, Alzheimer's Disease, Inborn Errors of Metabolism, Others | Diabetic Neuropathy | Chronic Kidney Disease |

| Route of Administration | Oral, Enteral | Oral | Enteral |

| Patient Group | Geriatric, Adult, Pediatric | Geriatric | Pediatric |

| Distribution Channel | Hospital Pharmacy, Retail Pharmacy, Online Pharmacy | Hospital Pharmacy | Online Pharmacy |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Product Category

| Sub-Segment | Key Trend |

| Powder | Hospital bulk procurement drives volume; cost-per-serving advantage over liquids |

| Soft-Gel Capsules | Lipid-based delivery enhancing fat-soluble nutrient bioavailability |

| Liquid | Ready-to-consume convenience for geriatric and pediatric patients |

| Pills/Tablets | Ambulatory convenience for chronic condition management |

Powder formulations continue to dominate due to their flexibility in clinical settings and favorable economics for institutional buyers. Soft-gel capsules are attracting R&D investment as manufacturers seek differentiated delivery mechanisms for neurological and metabolic disorder applications.

By Application

| Sub-Segment | Key Trend |

| Diabetic Neuropathy | B-vitamin complex formulations targeting nerve function restoration |

| Chronic Kidney Disease | Protein-restricted, phosphorus-managed formulas per nephrology guidelines |

| Alzheimer's Disease | Multi-nutrient combinations (Souvenaid-type) targeting synaptic function |

| Inborn Errors of Metabolism | Amino acid-modified formulas for PKU, MSUD, and related conditions |

| Other Applications | Oncology malnutrition, IBD, and post-surgical recovery nutrition |

Diabetic neuropathy leads by revenue share, reflecting the global scale of Type 2 diabetes. Chronic kidney disease is the fastest-growing application as renal societies worldwide endorse medical nutrition therapy as standard care.

By Route of Administration

| Sub-Segment | Key Trend |

| Oral | Dominant format for ambulatory and home-based chronic disease management |

| Enteral | Growing in ICU and long-term care through tube-feeding standardization |

Oral delivery accounts for nearly two-thirds of consumption, though enteral administration is growing faster as home enteral nutrition programs expand across developed markets.

By Patient Group

| Sub-Segment | Key Trend |

| Geriatric | Largest cohort; sarcopenia and cognitive decline driving multi-nutrient demand |

| Adult | Working-age diabetes and CKD management expanding addressable market |

| Pediatric | Newborn screening programs accelerating early intervention with specialized formulas |

Geriatric patients represent over half of market volume. Pediatric formulations are the fastest-growing cohort due to expanded metabolic screening at birth.

By Distribution Channel

| Sub-Segment | Key Trend |

| Hospital Pharmacy | Formulary gatekeeping controls institutional product selection |

| Retail Pharmacy | Walk-in prescription fulfillment for chronic maintenance patients |

| Online Pharmacy | DTC subscription models and telehealth integration driving rapid growth |

Hospital pharmacies control the majority of distribution, but online channels are eroding this dominance through direct-to-patient convenience and algorithmic prescription matching.