Medical Foods Market Summary

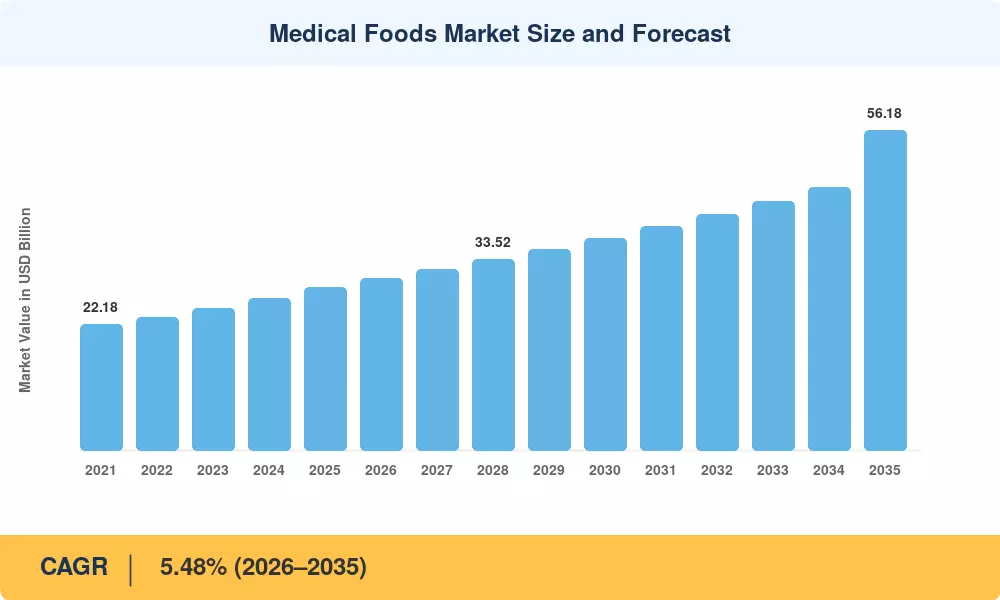

The Medical Foods Market reached an estimated USD 28.64 billion in 2025 and is projected to grow from USD 30.13 billion in 2026 to USD 56.18 billion by 2035, advancing at a CAGR of 5.48% during the forecast period. This expansion is anchored in a global policy shift toward medically supervised nutrition as a frontline intervention for chronic disease management. Government reimbursement frameworks — including India's Ayushman Bharat program and China's updated GB 29922-2025 standard for Foods for Special Medical Purposes — are converting clinical therapeutic nutrition from physician-discretionary to formulary-mandated, pulling billions in new spending into the category [2][3].

The transformation underway in the Medical Foods Market reflects a broader migration from generic oral nutritional supplements toward disease-specific nutritional formulas engineered for targeted metabolic pathways. Legacy one-size-fits-all powders are giving way to precision-formulated soft-gel capsules and lipid-based enteral nutrition therapy systems that improve bioavailability for neurological and renal applications. The European Commission's 2024 revision of Regulation (EU) 609/2013 allocated EUR 180 million for clinical validation of metabolic disorder dietary support products, signaling regulatory intent to elevate these products closer to pharmaceutical-grade oversight [4][5].

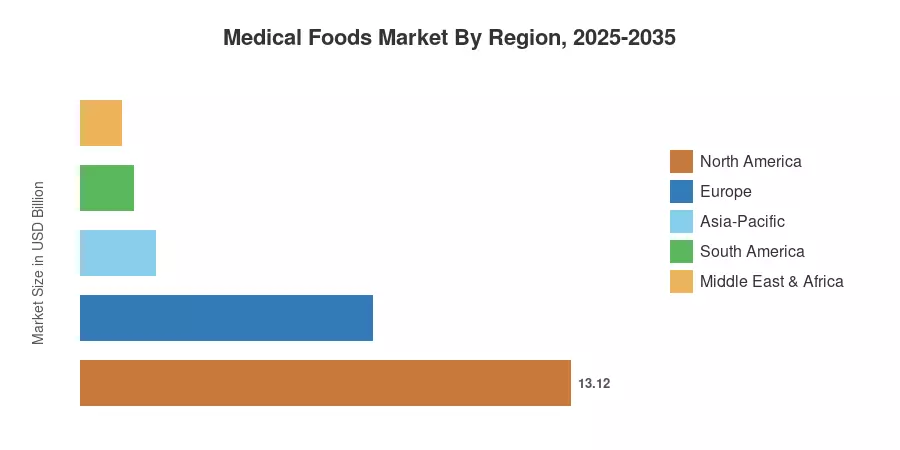

North America commands roughly 45.8% of the Medical Foods Market, driven by established hospital pharmacy infrastructure and insurer acceptance of enteral nutrition therapy protocols. Asia-Pacific represents the fastest-growing region at a projected 7.02% CAGR through 2035, fueled by aging demographics in Japan and South Korea alongside expanding middle-class demand for clinical therapeutic nutrition in India and China. Europe holds the second-largest share at approximately 27.3%, with Germany and France leading adoption of medically supervised nutrition pathways The next decade will test whether regulatory harmonization can keep pace with clinical innovation across these regions.

Key Report Takeaways

• By Product Category

- Powder formulations captured 58.9% of the Medical Foods Market in 2025, reflecting bulk reconstitution demand across hospital formularies

- Soft-gel capsules are forecast to post the fastest segment CAGR at 8.12% through 2035, driven by lipid-based delivery systems enhancing bioavailability for metabolic disorder dietary support

- Liquid formats generated approximately USD 4.87 billion in 2025 revenue, serving pediatric and geriatric patients requiring ready-to-consume enteral nutrition therapy

• By Application

- Diabetic neuropathy accounted for 28.4% of the Medical Foods Market in 2025, supported by rising Type 2 diabetes prevalence globally

- Chronic kidney disease formulations are projected to expand at a 7.98% CAGR, reflecting nephrology guidelines increasingly endorsing disease-specific nutritional formulas

• By Region

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up revenue modeling from manufacturer filings, hospital procurement databases, and distributor sell-through data with top-down validation against national health expenditure benchmarks. Historical figures (2021–2024) are actuals; the base year (2025) blends Q1–Q3 actuals with Q4 estimates; forecast years (2026–2035) apply the calibrated 5.48% CAGR with adjustments for regulatory and demographic inflection points.