Medical Lifting Sling Market Summary

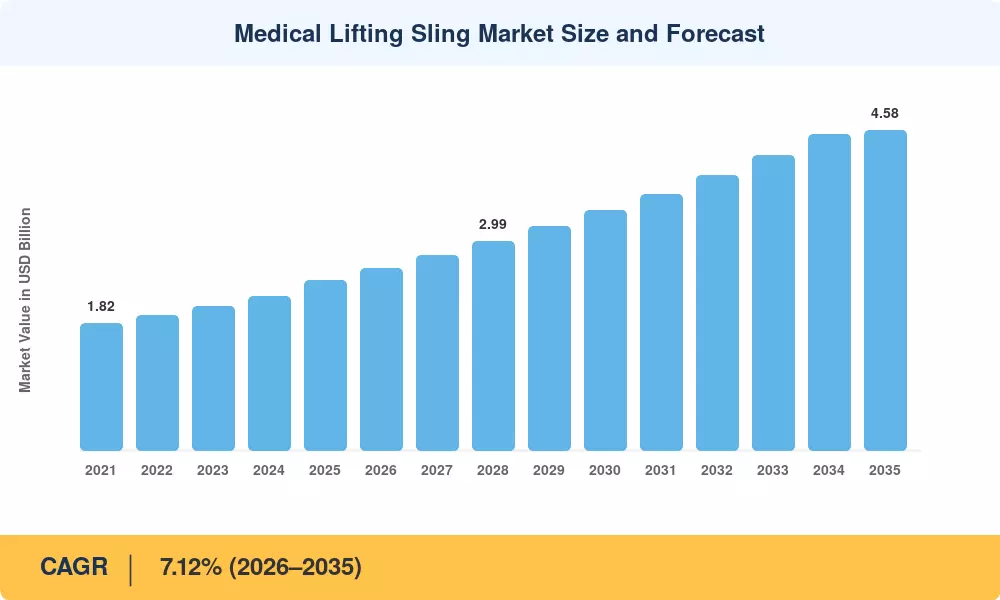

The medical lifting sling market reached an estimated USD 2.43 billion in 2025 and is projected to grow from USD 2.60 billion in 2026 to USD 4.58 billion by 2035, registering a CAGR of 7.12% during the forecast period. Two forces are reshaping procurement patterns across healthcare systems worldwide: OSHA's updated ergonomic guidelines for patient-handling tasks in acute care facilities, and CMS reimbursement expansions for durable medical equipment that now cover ceiling hoist sling systems and bariatric lifting solutions in home-care settings [2]. These policy shifts have turned what was once a discretionary equipment upgrade into a compliance-driven investment for hospitals and long-term care operators alike.

Traditional patient transfer techniques, including slide sheets, draw sheets and two-person lift protocols, are being replaced by mechanical ceiling hoist sling systems and portable patient transfer devices integrated with electronic health information. According to the U.S. Bureau of Labor Statistics, musculoskeletal injuries among healthcare workers cost employers an estimated USD 13.5 billion a year [3], a statistic that has spurred the adoption of caregiver assistive devices throughout acute and post-acute settings. RFID tracking, antimicrobial textiles and load-sensing technology in smart slings are commanding premium prices and extending the addressable market for mobility help for bedridden patients.

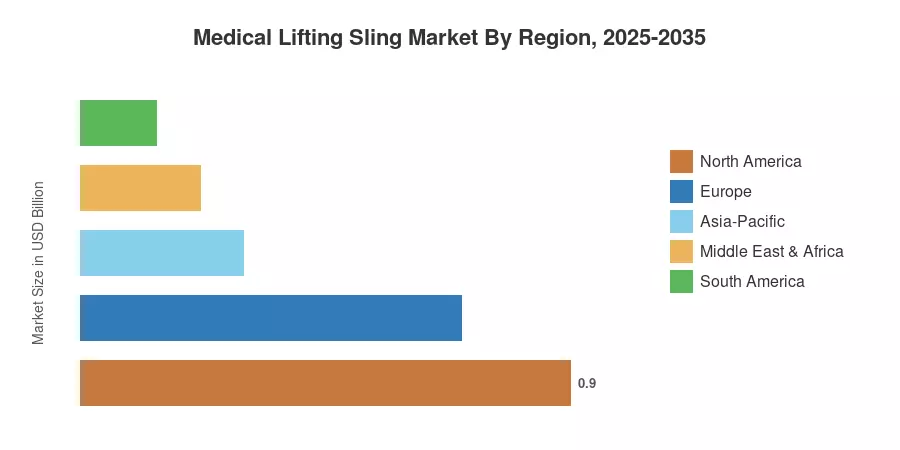

North America is estimated to contribute over 37% to the global medical lifting sling market on account of stringent workplace safety regulations and high healthcare spending per capita. Asia-Pacific is the fastest expanding geography with an anticipated CAGR of 12.18%, driven by hospital infrastructure build-outs in China and India. Europe has the second-highest proportion of over 29%, with EU Medical Device Regulation (MDR) compliance timelines pushing facility renovations until 2030 and beyond [4].

Key Report Takeaways

• By Product Type

- Seating and full-body slings led the medical lifting sling market with approximately 39% revenue share in 2025, reflecting strong demand across rehabilitation and surgical recovery workflows

- Bariatric and bari-plus slings are forecast to expand at an 11.72% CAGR through 2035, driven by rising global obesity prevalence and the need for specialized patient transfer equipment

• By Material

- Polyester accounted for roughly 72% of the medical lifting sling market in 2025, favored for its durability, washability, and compatibility with infection-control protocols

- Technical textiles incorporating antimicrobial coatings are advancing at an 11.31% CAGR, reflecting hospital demand for advanced caregiver assistive devices

• By Region

- North America captured approximately 37% of the medical lifting sling market in 2025, with the United States alone representing over 78% of regional revenue

- Asia-Pacific registers the fastest regional CAGR at 12.18%, fueled by government investments in ceiling hoist sling systems and long-term care infrastructure

Medical Lifting Sling Market Size and Forecast (2021–2035)

MRFR utilizes a triangulated methodology to estimate the market size, comprising bottom-up revenue analysis based on manufacturer filings, top-down validation using healthcare expenditure databases from the WHO and OECD, and primary interviews with procurement directors from over 120 healthcare facilities across 18 countries. Historical statistics (2021-2024) are actuals; 2025 is the expected base year; values for 2026-2035 are forecasted using the calibrated CAGR of 7.12%.