Medical Radiation Shielding Market Summary

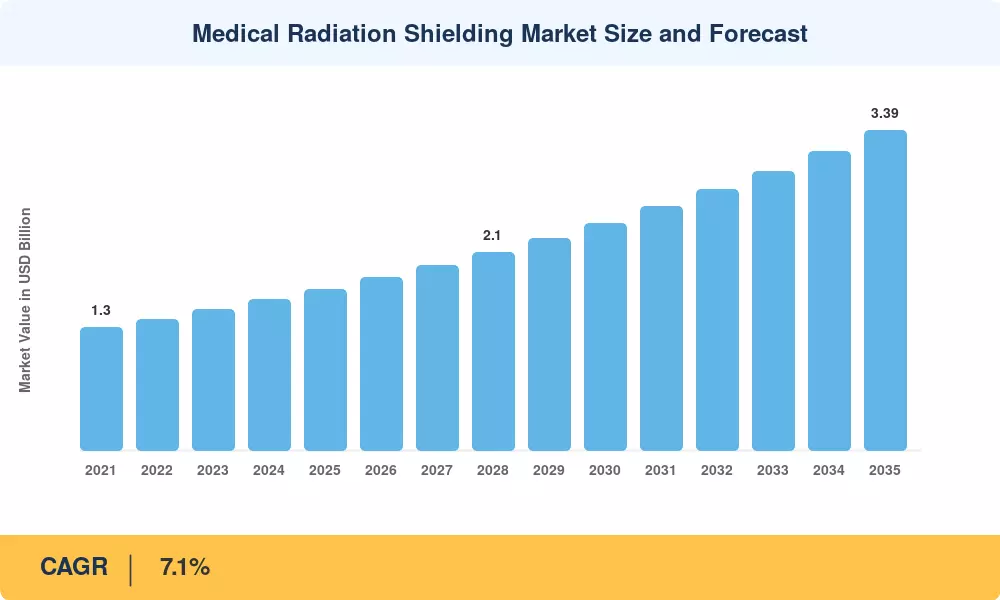

The Global Medical Radiation Shielding Market size was valued at USD 1.71 Billion in 2025, and the market is projected to grow from USD 1.83 Billion in 2026 to USD 3.39 Billion by 2035, registering a CAGR of 7.1% during the forecast period 2026–2035. Two forces are driving this expansion: the global cancer burden — which the World Health Organization projects will produce 35 million new cases annually by 2050 [1] — and the rapid build-out of proton therapy and radiopharmaceutical manufacturing facilities across Asia and the Middle East [2]. Government mandates for radiation safety in healthcare settings, including the European Union's revised Basic Safety Standards Directive (2013/59/Euratom) and updated U.S. Nuclear Regulatory Commission (NRC) guidelines, are creating binding compliance timelines that funnel capital directly into shielding upgrades [3].

A generational shift in shielding materials is underway within the medical radiation shielding market. Lead — the dominant barrier material for over a century — is gradually ceding ground to non-lead composite alternatives that reduce structural weight by 30–40% and eliminate hazardous disposal requirements [4]. Hospitals retrofitting legacy diagnostic imaging suites are choosing bismuth- and barium-based composites because they can be installed without structural reinforcement, cutting project timelines by weeks. The U.S. Department of Energy's 2024 Isotope Program invested over USD 200 million to expand domestic molybdenum-99 production, and every new hot cell requires Class I shielding that meets 10 CFR Part 20 standards [5].

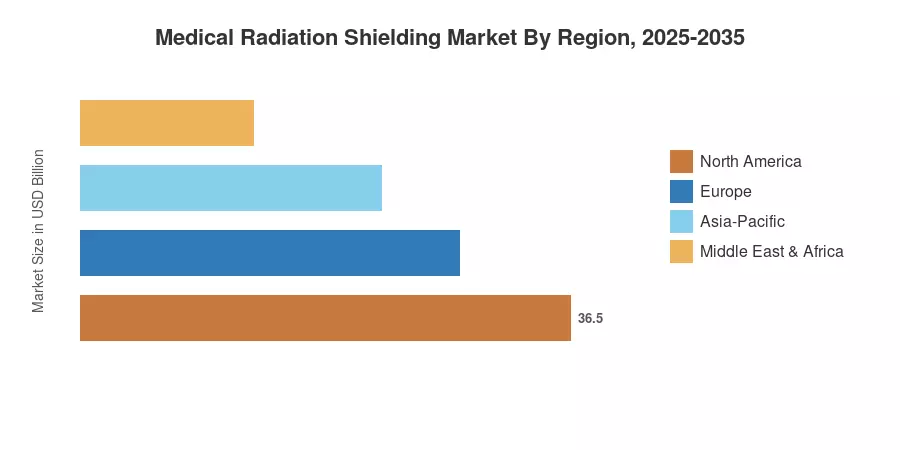

North America held roughly 38% of global revenue in 2025, anchored by the largest installed base of linear accelerators and PET-CT scanners in the world. Asia-Pacific is the fastest-growing region in the medical radiation shielding market, projected to advance at an approximate 7.8% CAGR through 2035, fueled by China's "Healthy China 2030" initiative and India's Ayushman Bharat expansion of tertiary oncology centers [6]. Europe claimed the second-largest share at about 27%, supported by the EU4Health Programme's radiation safety mandates [7]. The decade ahead will reward suppliers that combine advanced materials science with turnkey project delivery.

Key Report Takeaways

• By Material

- Lead retained approximately 76% of the medical radiation shielding market in 2025, reflecting its established regulatory acceptance and cost-effectiveness for high-energy photon attenuation.

- Non-lead composites are projected to grow at about a 9.0% CAGR from 2026 to 2035, driven by environmental regulations restricting lead use in healthcare construction.

• By Imaging/Therapy Modality

- Diagnostic radiology commanded roughly 58% of revenue in the medical radiation shielding market in 2025, owing to the sheer volume of X-ray and CT installations worldwide.

- Proton and heavy ion therapy is forecast to post the fastest segment CAGR of approximately 10.2% through 2035.

• By End User

- Hospitals accounted for an estimated 66% of the medical radiation shielding market size in 2025.

- Ambulatory surgery centers are expected to expand at a roughly 10.6% CAGR from 2026 to 2035.

• By Region

- North America captured approximately 38% of the 2025 revenue in the medical radiation shielding market.

- Asia-Pacific is projected to register the highest regional CAGR of about 7.8% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's proprietary estimation framework combines bottom-up procurement data from hospital networks, radiation facility construction permits, material supplier shipments, and top-down macroeconomic indicators. Historical figures (2021–2024) are triangulated against published import-export databases and verified through primary interviews with shielding contractors. Forecast projections (2026–2035) apply segment-level growth assumptions modeled on planned facility pipelines and regulatory compliance schedules.