Medical Spa Market Summary

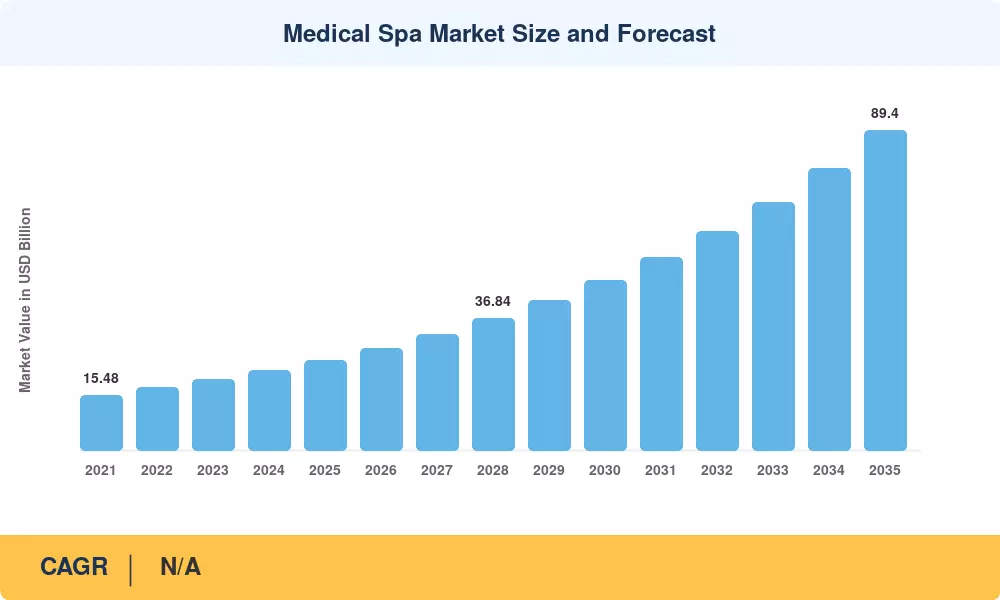

The Medical Spa Market reached an estimated USD 25.20 billion in 2025 and is projected to grow from USD 28.60 billion in 2026 to USD 89.40 billion by 2035, registering a CAGR of 13.50% during the forecast period. This expansion tracks a structural shift: consumers across age groups and income bands now treat aesthetic procedures as routine personal care rather than luxury indulgences. Private-equity platforms have accelerated the pace of clinic consolidation, viewing cash-pay aesthetic revenue as a hedge against insurance-reimbursement volatility.

Technology is rewriting the medical spa playbook. Legacy single-function laser cabinets are giving way to multi-modal energy-based platforms capable of delivering fractional resurfacing, radiofrequency skin tightening, and intense pulsed light treatments from a single console. AI-guided skin diagnostics — already deployed in more than 3,200 clinics in North America — reduce consultation time and improve treatment plan accuracy. The American Med Spa Association estimates that clinics investing in next-generation platforms see 18–22% higher per-visit revenue within the first year of adoption.

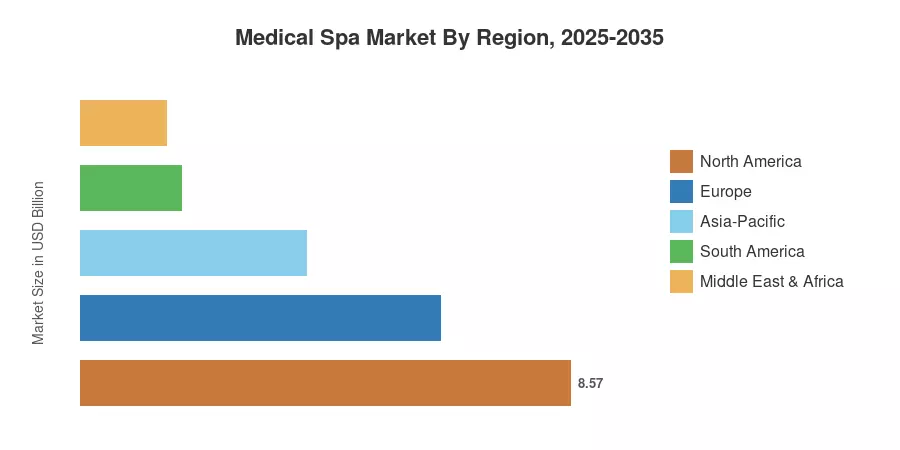

North America commands roughly 34.0% of the global Medical Spa Market revenue, anchored by high procedure volumes in the United States and a mature regulatory framework. Asia-Pacific stands as the fastest-growing region at a projected 15.7% CAGR through 2035, propelled by rising disposable incomes, booming medical-tourism corridors in Thailand and South Korea, and expanding middle-class populations in India and China. Europe holds the second-largest share at approximately 25.0%, driven by regulatory harmonization under the EU Medical Device Regulation. The coming decade will likely see these three regions collectively account for over 85% of global revenue.

Key Report Takeaways

• By Services

- Facial treatments captured approximately 48.5% of the Medical Spa Market revenue in 2025, driven by high repeat-visit rates for chemical peels, microneedling, and hydrafacials.

- Laser hair removal is advancing at a 16.3% CAGR through 2035, reflecting device miniaturization and declining per-session costs that widen the addressable patient pool.

- Injectables — including neurotoxins and dermal fillers — generated an estimated USD 3.78 billion in 2025, supported by expanded FDA-approved indications.

• By End User

- Female patients accounted for roughly 76.3% of the Medical Spa Market size in 2025, sustained by broad social acceptance and diversified treatment menus.

- Male patient spend is growing at a 17.2% CAGR through 2035, propelled by destigmatization and targeted marketing campaigns.

• By Region

- North America led with an estimated 34.0% revenue share in 2025, underpinned by high per-capita aesthetic spending.

- Asia-Pacific is projected to expand at a 15.7% CAGR through 2035, with South Korea, Thailand, and India emerging as procedure-volume leaders.

Medical Spa Market Size and Forecast (2021–2035)

Market Research Future derives historical estimates from proprietary bottom-up clinic surveys, cross-referenced with published procedure-volume data from the International Society of Aesthetic Plastic Surgery and the American Med Spa Association. Forecast projections apply a compound model that factors demographic penetration curves, device replacement cycles, and regional regulatory timelines.