Medical Supplies Market Summary

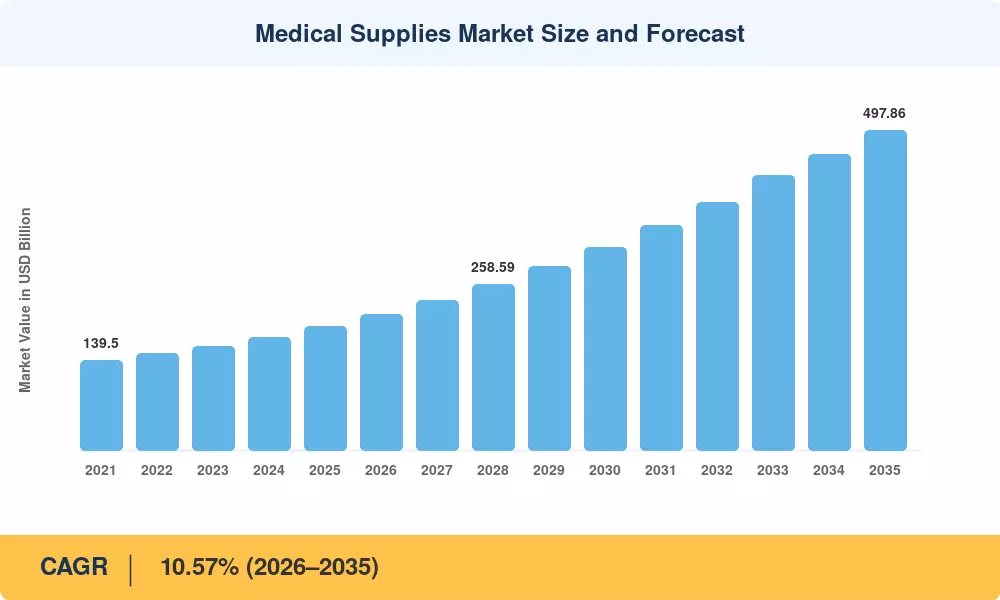

The Medical Supplies Market was valued at USD 192.21 billion in 2025 and is projected to reach USD 211.52 billion in 2026 before climbing to USD 497.86 billion by 2035, registering a CAGR of 10.57% during the forecast period (2026–2035). Tightening infection-control mandates across WHO member states and a decisive shift toward value-based reimbursement models are converting disposable clinical consumables from low-margin commodity inputs into performance-critical health-system enablers. The U.S. Pandemic Preparedness Act alone earmarked over USD 6 billion through 2027 to rebuild strategic stockpiles of sterile surgical supplies, PPE and protective equipment [2].

Technology is changing the way that hospitals buy their supplies. AI-powered demand sensing solutions are replacing legacy manual ordering systems, integrating real-time consumption data with logistical efficiency. Clinical care consumables supply chains are being rebuilt around predictive analytics and RFID-enabled traceability, such as Cardinal Health’s USD 450 million investment in automated distribution centers in 2024 [3]. At the same time, ISO 13485:2016 alignment is boosting the global quality floor, forcing smaller producers to upgrade or get out.

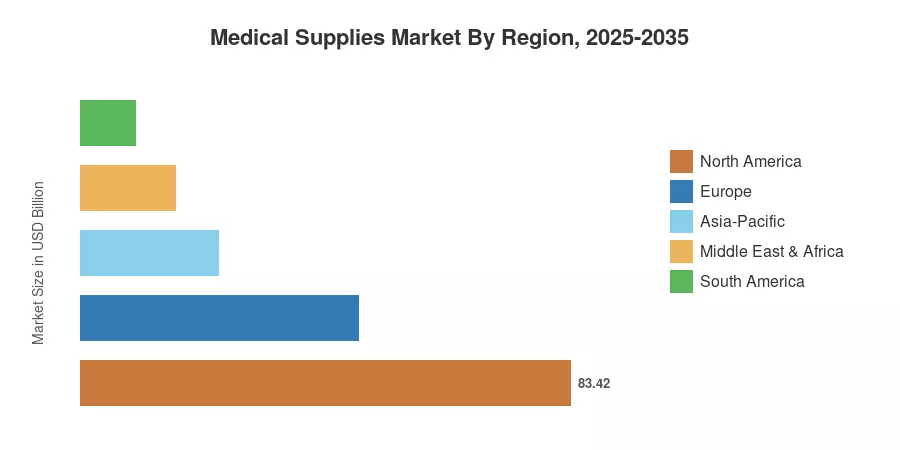

North America held a share of around 43.4% in the Medical Supplies Market in 2025, owing to the presence of a well-developed reimbursement infrastructure and early adoption of GPOs Asia-Pacific is the fastest-growing market with a projected CAGR of 12.18%, driven by increasing hospital capacity in India and China. Europe held the second-highest share at about 24.6%, balancing the new EU Medical Device Regulation (MDR) with sustainability-driven product reformulation. The Medical Supplies Market is set to accelerate its double-digit growth as the move to decentralized care and the burden of chronic diseases propel demand through 2035.

Key Report Takeaways

• By Product Type

- Infusion and injectable supplies led the Medical Supplies Market with a 24.6% revenue share in 2025, driven by rising chronic-disease management and ambulatory infusion centers

- Dialysis consumables are forecast to grow at a CAGR of 8.1% through 2035, supported by increasing end-stage renal disease prevalence globally

- Diagnostic supplies accounted for approximately USD 38.9 billion in 2025, reflecting expanded point-of-care testing adoption

• By Application

- Infection control represented 20.3% of total Medical Supplies Market revenue in 2025, as hospitals scaled up PPE and protective equipment inventories post-pandemic

- Respiratory applications are projected to expand at a 8.85% CAGR to 2035, fueled by COPD and asthma case growth in aging populations

• By End User

- Hospitals commanded a 72.1% share of total market value in 2025, reflecting their role as the primary procurement channel for sterile surgical supplies

- Home-care settings represent the fastest-growing end-user channel with a projected 9.56% CAGR, driven by payer incentives favoring outpatient recovery

• By Geography

- North America captured 43.4% of the Medical Supplies Market in 2025, sustained by entrenched GPO contracts and federal stockpile programs

- Asia-Pacific is forecast to register the highest regional CAGR at 12.18% during 2026–2035

Medical Supplies Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a triangulated research methodology, which is a mixture of supply-side and demand-side approaches. Data collected from over 120 manufacturers is aggregated at the bottom to estimate the size of the market. The top-down approach is used to cross-validate the data against hospital procurement databases and government trade-flow figures. Historical data (2021–2024) includes audited yearly reports and customs data. Forecast data (2026–2035) is based on a calibrated compound growth path based on the base year of 2025