Medical Transcription Software Market Summary

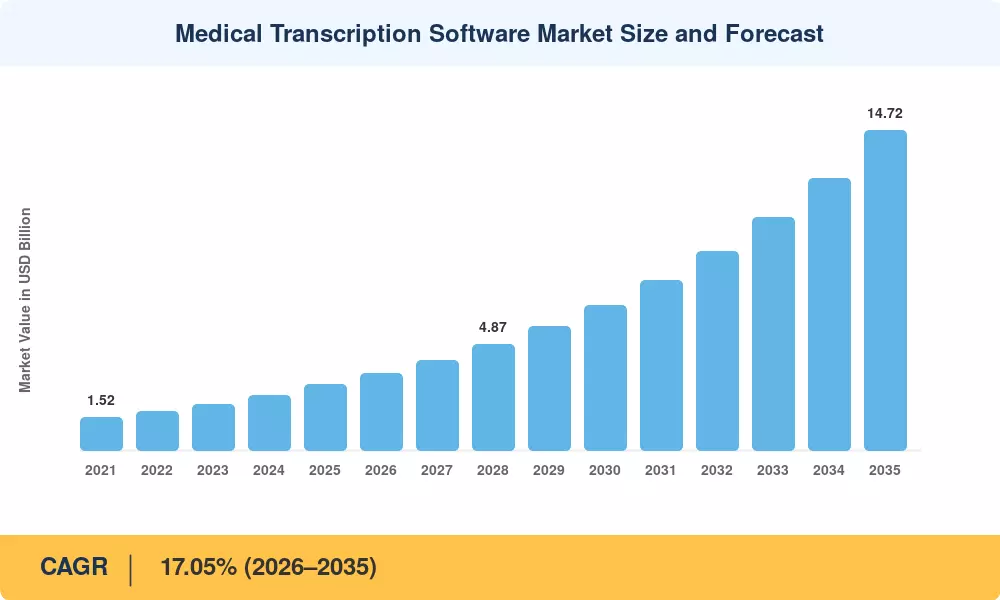

The medical transcription software market was valued at USD 3.05 billion in 2025, with the forecast period opening at USD 3.54 billion in 2026 and climbing to USD 14.72 billion by 2035 at a CAGR of 17.05%. Two catalysts are propelling this trajectory: the U.S. Centers for Medicare & Medicaid Services (CMS) mandate for standardized clinical documentation across value-based care programs [2], and a wave of venture funding that channeled over USD 1.8 billion into clinical documentation automation startups between 2022 and 2024. Physician burnout — now affecting roughly 53% of U.S. clinicians according to the AMA — has turned speech-to-text healthcare tools from a convenience into a clinical imperative.

Legacy dictation workflows that relied on offshore human transcriptionists are giving way to AI-driven voice recognition for doctors embedded directly within electronic health records. Hospitals deploying ambient clinical intelligence report documentation-time reductions of 45–55%, freeing clinicians to spend more face time with patients [4]. The ONC's 2024 interoperability rule further accelerated EHR transcription integration by requiring certified health IT systems to support standardized data exchange, making HIPAA-compliant transcription a baseline expectation rather than a premium add-on [5].

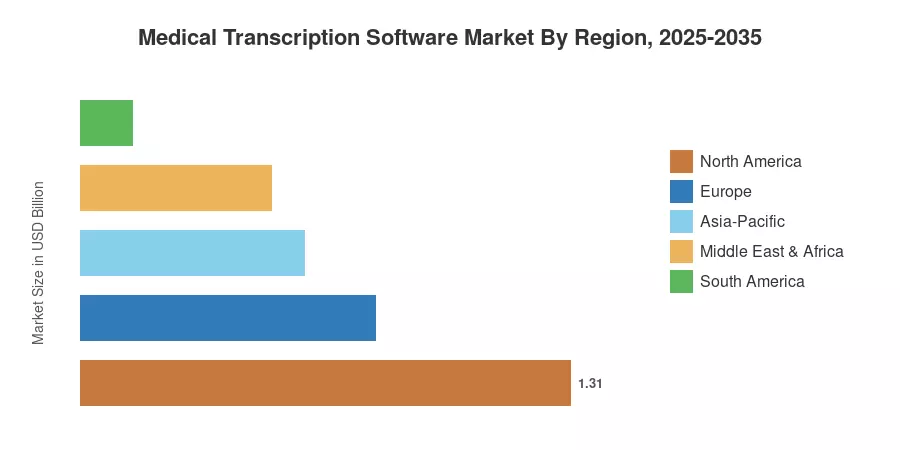

North America retained approximately 43% of the medical transcription software market in 2025, underpinned by mature EHR adoption and payer-driven documentation requirements. Asia-Pacific is the fastest-growing region at a projected 19.58% CAGR, fueled by India's Ayushman Bharat Digital Mission and China's smart-hospital initiatives. Europe holds the second-largest share at roughly 26%, driven by NHS digitization programs and EU cross-border health data regulations The decade ahead will see clinical documentation automation shift from departmental pilots to enterprise-wide deployments across every care setting.

Key Report Takeaways

• By Component

- Software accounted for 63% of the medical transcription software market in 2025, reflecting strong demand for standalone clinical documentation automation platforms

- Services are forecast to expand at an 18.35% CAGR through 2035, as health systems outsource implementation and training for speech-to-text healthcare tools

• By Deployment Mode

- Cloud-based deployment captured a 60% revenue share in 2025, favored for lower upfront costs and seamless EHR transcription integration

- On-premise models remain preferred by large academic medical centers requiring full data sovereignty under HIPAA-compliant transcription mandates

• By End User & Type

- Hospitals commanded USD 1.44 billion of the medical transcription software market in 2025, driven by high-volume documentation needs

- Integrated voice recognition with EHR is projected to climb at a 19.26% CAGR, the fastest among all type segments

• By Region

- North America leads with 43% share, while Asia-Pacific is set to post the swiftest growth among all regions

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s market sizing combines bottom-up revenue analysis of major vendors, top-down cross-validation against healthcare IT spending benchmarks from WHO and OECD, and primary interviews with 120+ CIOs, CMIOs, and health IT procurement leads across 18 countries. All figures are expressed in current USD Billion.