Methyl Isobutyl Ketone Market Summary

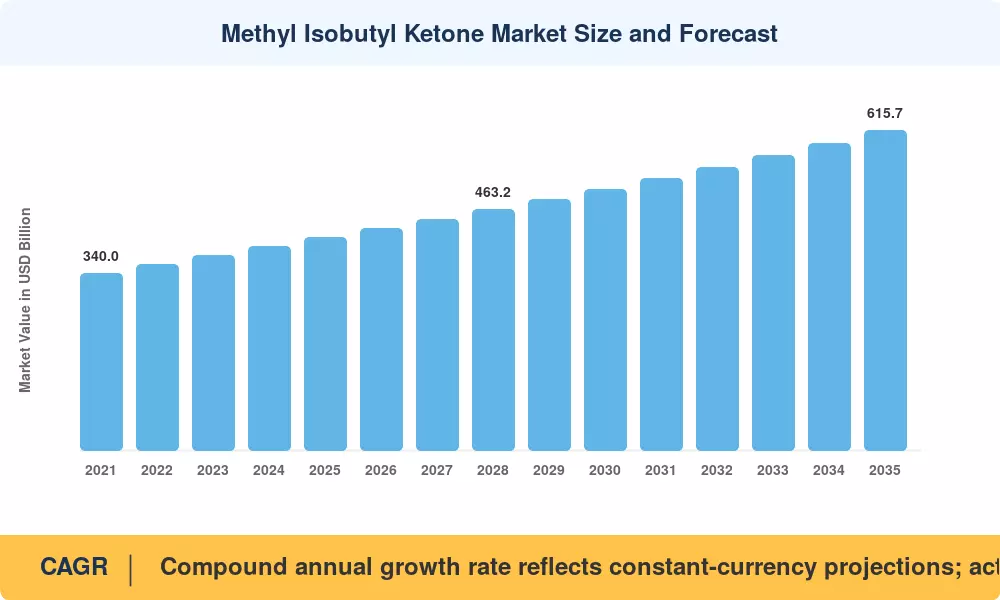

The Methyl Isobutyl Ketone Market reached an estimated USD 410.0 million in 2025 and is projected to grow from USD 427.0 million in 2026 to USD 615.7 million by 2035, registering a CAGR of 4.15% during the forecast period. Expanding infrastructure programs across emerging economies and tightening performance requirements for surface coatings have created steady demand for high-purity MIBK as a solvent and chemical intermediate [1][2]. Government spending on road networks alone — the Indian government allocated over USD 12 billion to highway construction in FY 2024 — directly pulls MIBK consumption through paints, adhesives, and rubber compounds used in transportation infrastructure [3].

Production technology is moving from the traditional sulfuric acid-catalyzed acetone condensation pathways to palladium-based single-step catalytic techniques that integrate hydrogenation and condensation of acetone in one reactor. Shell’s unique one-step MIBK technology, which reduces energy usage by almost 30% compared to the three-step approach, has been set as the bar for new-capacity greenfield investments [4]. Finally, legacy production units that are unable to satisfy tightening VOC emission limitations are being phased out under regulatory pressure under the EU’s REACH framework and amendments to the US EPA Toxic Substances Control Act (TSCA) [5].

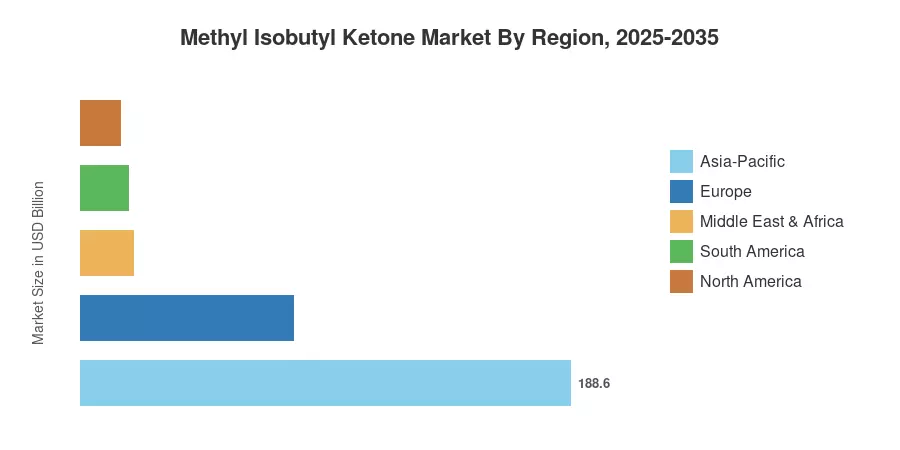

Asia-Pacific dominates the Methyl Isobutyl Ketone Market and is expected to be dominant during the forecast period, followed by North America and Europe. Asia-Pacific accounted for about 46% of the worldwide revenue, owing to the presence of a strong base of manufacturing of coatings and rubber in China. The region also displays the highest CAGR of 4.85% throughout 2035. North America is the second largest share at around 22%, fueled by automotive OEM refinish and pharmaceutical extraction demand, while Europe is about 20% with growth rooted in sustainable coatings reformulation. The bulk of capacity additions in the coming decade will be in East Asia and the Middle East, which will alter the global trade balance for this versatile ketone solvent.

Key Report Takeaways

• By Application

- Solvents accounted for the largest application share at approximately 38% in 2025, driven by widespread use in paints, coatings, and adhesive formulations requiring medium-evaporation-rate ketone solvents.

- Rubber processing chemicals represent the fastest-growing application segment with a projected CAGR of 4.9%, as tire manufacturers increase antioxidant and antiozonant loadings to meet extended-warranty specifications.

- Surfactant applications in the Methyl Isobutyl Ketone Market are valued at roughly USD 52 million in 2025, reflecting growing use in ore flotation and mineral extraction processes.

• By End-User Industry

- Paints and coatings end users command approximately 42% of total MIBK demand, linking market growth to construction and automotive output cycles.

- Pharmaceutical end users are expanding at a CAGR of 4.6% as MIBK gains traction in active pharmaceutical ingredient purification and antibiotic extraction.

• By Region

- Asia-Pacific leads the Methyl Isobutyl Ketone Market with 46% share in 2025, underpinned by China and India's manufacturing expansion.

- South America registers the second-fastest CAGR at 4.55%, propelled by Brazil's expanding automotive coatings sector.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology triangulates top-down trade-flow analysis (import/export data from UN Comtrade and national customs databases) with bottom-up capacity utilization estimates from major MIBK producers. Historical figures incorporate producer price indices published by national statistics bureaus, while forecast projections apply econometric regression linking MIBK consumption to GDP-weighted industrial production indices across 22 key consuming countries [1].