Microcrystalline Cellulose MCC Market Summary

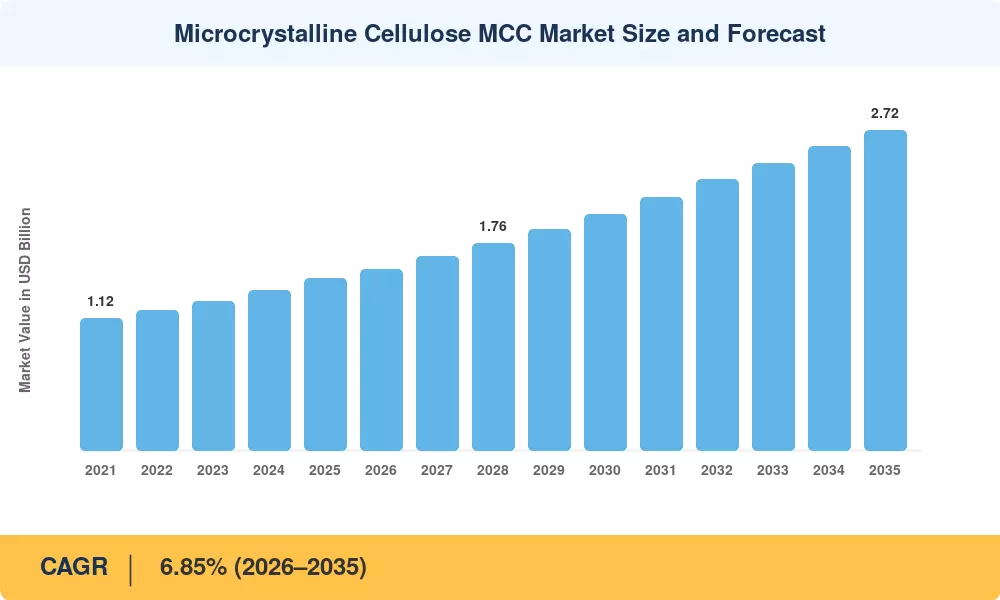

The Microcrystalline Cellulose Market was valued at USD 1.46 billion in 2025 and is projected to reach USD 1.54 billion in 2026 before climbing to USD 2.72 billion by 2035, registering a CAGR of 6.85% during the forecast period (2026–2035). Sustained demand for pharmaceutical excipients in generic drug manufacturing across South and Southeast Asia, combined with tightening clean-label mandates under the EU's Farm to Fork Strategy, anchors the upward trajectory. Capital commitments exceeding USD 320 million toward cellulose processing capacity expansions in India and China during 2024–2025 underscore the commercial momentum behind purified cellulose supply chains [2][3].

A fundamental shift is underway in how cellulose powder is produced and utilized. Legacy batch acid-hydrolysis lines — long the workhorse for tablet binding agents — are steadily giving way to continuous steam-explosion and enzyme-mediated processes that cut energy consumption by 25–30% and reduce chemical waste streams [4]. The European Chemicals Agency's updated REACH dossier for MCC powder grades, finalized in late 2024, has accelerated this transition by rewarding low-emission processing with expedited registration pathways [5].

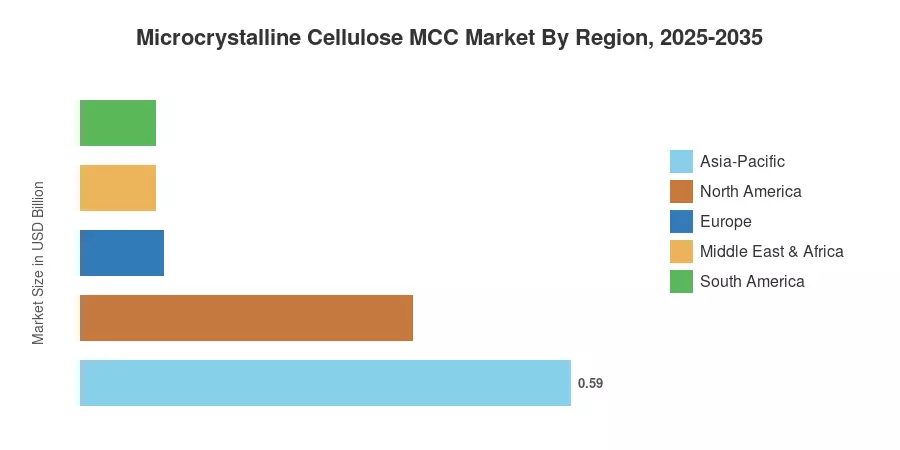

Asia-Pacific commands roughly 40.12% of the Microcrystalline Cellulose Market, making it both the largest and fastest-growing region at a projected 7.38% CAGR through 2035. North America holds the second-largest share at approximately 27.5%, buoyed by strong demand for dietary supplement ingredients and functional food additives across the United States. Europe follows closely, driven by the adoption of cosmetics-grade cellulose-based excipients. The next decade will see non-wood feedstock sources — cotton linters, bamboo, agricultural residues — reshape the competitive supply map as sustainability pressures intensify [6].

Key Report Takeaways

• By Source

- Wood-based sources dominated the Microcrystalline Cellulose Market with a 61.34% revenue share in 2025, reflecting deep integration with established pharmaceutical ingredients supply chains

- Non-wood-based alternatives are forecast to expand at a 7.58% CAGR through 2035, driven by agro-residue feedstock availability and rising demand for sustainable cellulose powder

• By Process

- Acid hydrolysis captured the leading position in the Microcrystalline Cellulose Market in 2025, valued at approximately USD 0.58 billion

- Steam explosion is set to register a 7.32% CAGR to 2035, as food stabilizers producers seek energy-efficient processing routes

• By End-User Industry

- Pharmaceuticals accounted for 46.10% of the Microcrystalline Cellulose Market in 2025, with tablet binding agents representing the largest single application category

- Cosmetics exhibit the fastest end-user growth at 7.52% CAGR, fueled by clean-beauty formulations requiring plant-derived rheology modifiers

• By Region

- Asia-Pacific led the Microcrystalline Cellulose Market with 40.12% revenue share in 2025

- North America held approximately USD 0.40 billion in 2025 market value, anchored by dietary supplement ingredients demand

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s proprietary estimation framework synthesizes primary interviews with cellulose powder producers, pharmaceutical excipients distributors, and food stabilizers blenders alongside secondary data from trade associations, regulatory filings, and company annual reports. Historical figures (2021–2024) reflect actual reported revenues; base-year 2025 combines preliminary earnings disclosures with supply-side production data. Forecast projections (2026–2035) apply a compound growth model validated against macroeconomic indicators and end-user capacity expansion pipelines.