Microspheres Market Summary

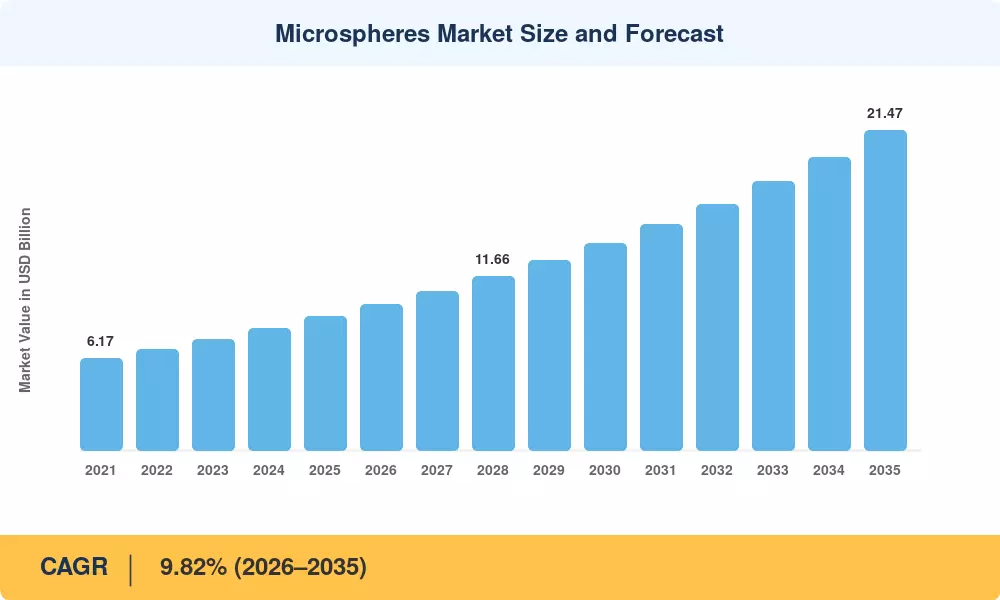

The Global Microspheres Market size was valued at USD 8.98 Billion in 2025, and the market is projected to grow from USD 10.12 Billion in 2026 to USD 21.47 Billion by 2035, registering a CAGR of 9.82% during the forecast period 2026–2035. Two catalysts anchor this trajectory: the FDA's expanding approvals for yttrium-90 glass microspheres in interventional oncology and a global push toward lightweight structural composites driven by electric-vehicle production mandates in the EU, China, and the United States [1]. Together, these forces convert what was once a niche specialty-materials category into a multi-vertical growth platform.

A technology transformation is reshaping the Microspheres Market from commodity filler beads toward engineered, application-specific controlled release microspheres and high-performance hollow glass bubbles. Legacy cenosphere supply from coal fly ash is giving way to synthetic biodegradable polymer beads and precision-graded ceramic variants. Global investment in injectable microsphere formulations alone surpassed USD 2.4 billion in combined R&D commitments between 2023 and 2025, reflecting pharma's confidence in drug-loaded microparticles as next-generation delivery vehicles [2].

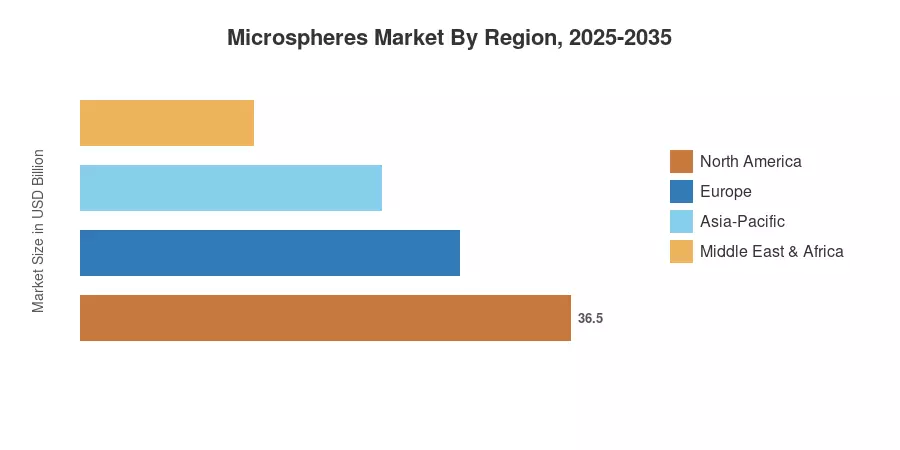

North America commands approximately 37% of the global Microspheres Market revenue, anchored by interventional radiology reimbursement pathways and a mature oil-and-gas services sector. Asia-Pacific is the fastest-growing region at an estimated 12.78% CAGR, fueled by China's glass-bubble capacity build-outs targeting EV battery enclosures and India's expanding paints-and-coatings sector. Europe holds the second-largest share at roughly 26%, though its phased microplastic ban is actively reshaping raw-material preferences toward glass and biodegradable polymers. The decade ahead will reward suppliers who can pair material science with application engineering across these divergent regional demand profiles.

Key Report Takeaways

• By Raw Material

- Glass raw material captured the dominant share of the Microspheres Market in 2026 and is forecast to grow at approximately 11.6% CAGR through 2035, driven by demand for hollow glass bubbles in syntactic foams and targeted drug delivery particles

- Polymer-based microspheres face headwinds from Europe's microplastic restrictions, pushing formulators toward biodegradable polymer beads and ceramic alternatives

- Fly ash cenospheres maintain a cost advantage in construction composites but are losing relative share to engineered glass variants

• By Type

- Hollow microspheres accounted for roughly 72% of Microspheres Market volume in 2026, benefiting from weight-reduction mandates across automotive and aerospace applications

- Solid microspheres hold a smaller but resilient niche in controlled release microspheres for pharmaceutical and cosmetic end uses

• By Application

- Medical technology led the Microspheres Market with approximately USD 4.38 Billion in 2026 revenue, powered by radioembolization procedures and injectable microsphere formulations

- Automotive and aerospace composites collectively represent the second-largest application pocket, with lightweight hollow variants displacing traditional fillers

• By Region

- North America held roughly 37% of the Microspheres Market in 2026, with the US accounting for the largest national share

- Asia-Pacific is projected to register the highest CAGR of 12.78%, led by China and India's manufacturing scale-up

Market Size and Forecast (2021–2035)

Market Research Future (MRFR)'s proprietary sizing framework combines bottom-up company-revenue aggregation with top-down demand modeling across six raw-material categories and eight application verticals. Historical data (2021–2024) draws on audited financials, trade databases, and customs-flow analysis; the forecast period (2026–2035) applies segment-level growth assumptions validated against macro indicators including GDP, industrial production indices, and healthcare spending trajectories.